Australian Beef Industry on the Path of Growth in 2022

Background for Australia beef sector growth

Apart from a continued growth of the beef market, the Australian beef sector is also hopeful that the effectuation of the UK-Australia Free Trade Agreement later in 2022 will further open an import high-value export market. The rebuilding of the national herd numbers has developed differently in South and Northern Australia as the weather has a large impact on the feasibility of expanding herds. In the south, 2022 will mark the third consecutive year with ample precipitation that has increased the productivity of feedlots. At the same time, the northern Australia have experienced average to below average precipitation the past two years which currently have caused key calf-producing regions such as the Barkly and the Gulf of Carpentaria to find themselves in a state of drought. Still yet, Meat and Livestock Australia(MLA)is hopeful that with favourable rainy seasons in 2022 and 2023, the national herd numbers could climb to 28.3 million heads by 2024, which would be the highest since 2014.

Production volumes increase well timed for the world market

As the herd size rebounds and the calves of 2020 and 2021 reach processor weights in the second half of 2022, the number of slaughters is expected to increase by 6.7 million heads equivalent to 11%. However, the weather may affect this, as dry periods may lead to cattle being sent for slaughter earlier than if rain is abundant. The processing plants have been severely affected over the past two years, as Covid-19 cases and restrictions have reduced processor capacity. As of January 2022, slaughter numbers are down 29% but as Australia is currently re-opening there is hope that the processor capacity will no longer be affected by Covid-19. As the carcass weights are expected to remain stable, the increase in slaughter numbers, the Australian beef production is expected to increase 12% YoY to 2,08 million mt in 2022, which is still short of the record year 2019, where 2,44 million mt were produced.

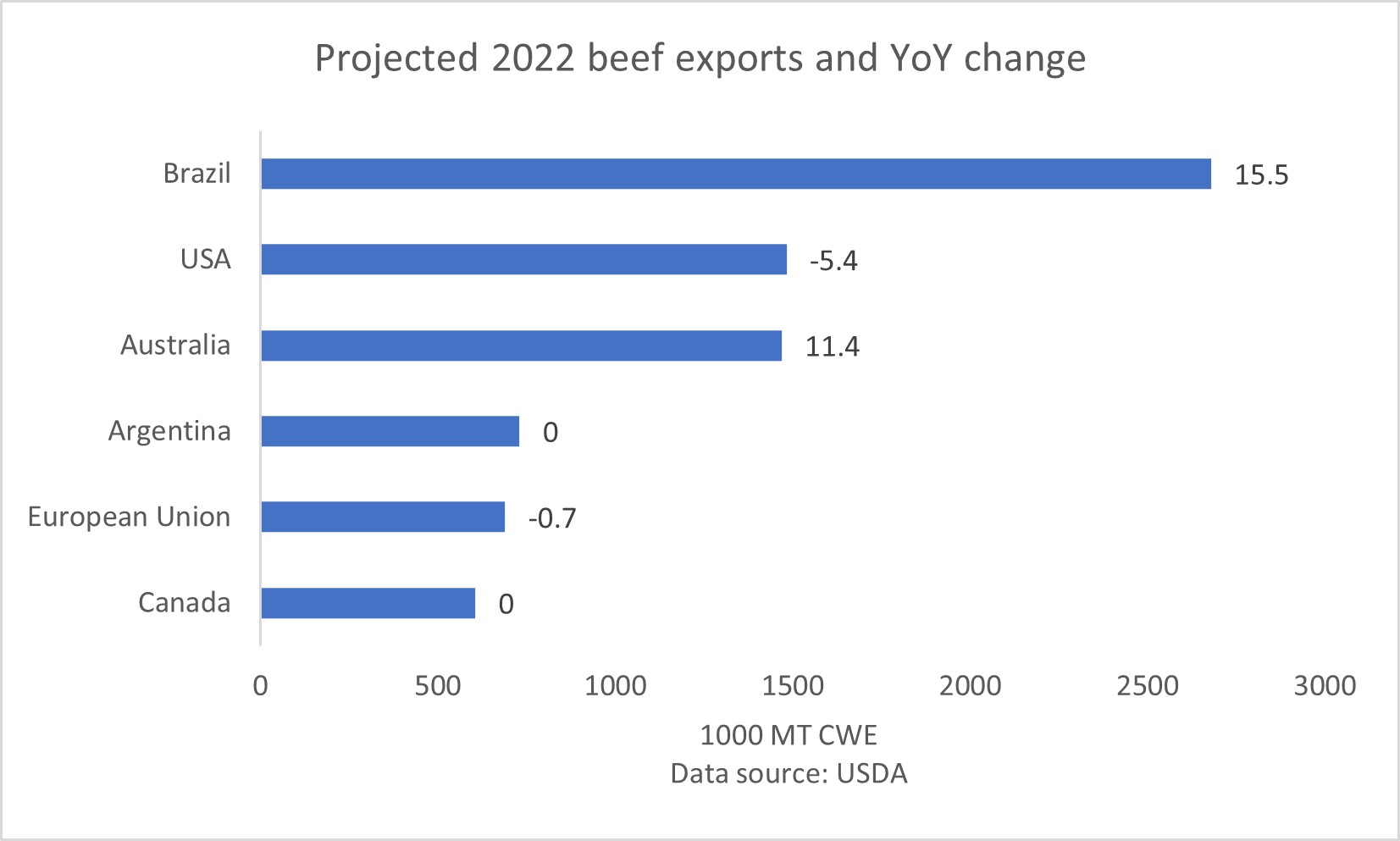

The increased exportable quantities available in Australia are perfectly timed to meet the global growing demand, which is projected by USDA to grow more than three times higher than the production in 2022 (Read more on the Tridge Analysis: Global Beef Demand Set to Exceed Supply in 2022 here). According to Trading Economics, the price of beef is nearly double that of Pre-covid-19 levels 4,1 USD/kg and this is likely continue rising as the world’s largest producer Brazil struggle to find suitable new grazing lots, consumers in high-income countries shift focus from quantity to quality and the general demand for beef increase along with higher living standards in developing countries. Indeed, beef prices have grown at a faster pace than other animal proteins in recent years having nearly doubled relative to a 2002-2004 index, whereas pork and poultry prices have grown at 51% and 19% respectively.

Outlook on Australia’s 2022 export

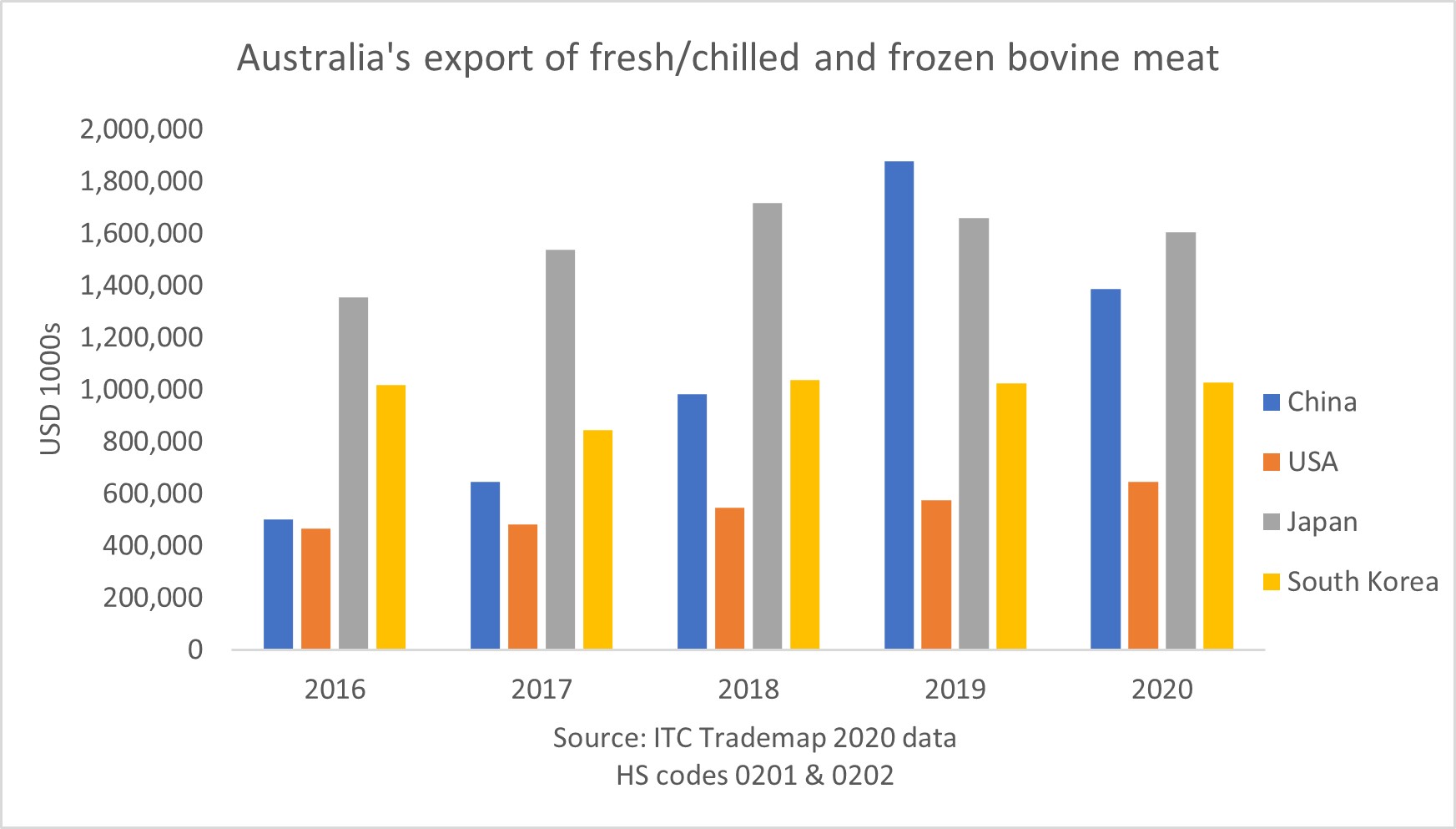

In 2022, the external factors most likely to affect the Australian beef exports are the global shipping prices and currency fluctuations. Due to its location, Australia lacks border trade and is reliant on international logistics services. However, with the main export locations being China, Japan and South Korea and the main export competitors being USA and Brazil, increased shipping prices by itself may not necessarily constitute a negative factor for Australia. However, for the exporters of fresh and chilled beef, that constitute 43% of the value of exports to Japan, 56% to USA and 67% to South Korea, delays in shipping are a major concern.

Working in global markets, the currency exchange rates of the Australian dollar strongly affects the competitiveness of Australian beef prices. MLA are expecting an appreciation of the AUD which would negatively affect margins and the competitiveness of Australian products globally. However, in the event that interest rates increase more in major export competing nations compared to the Australian interest rate, the AUD may in fact experience depreciation.