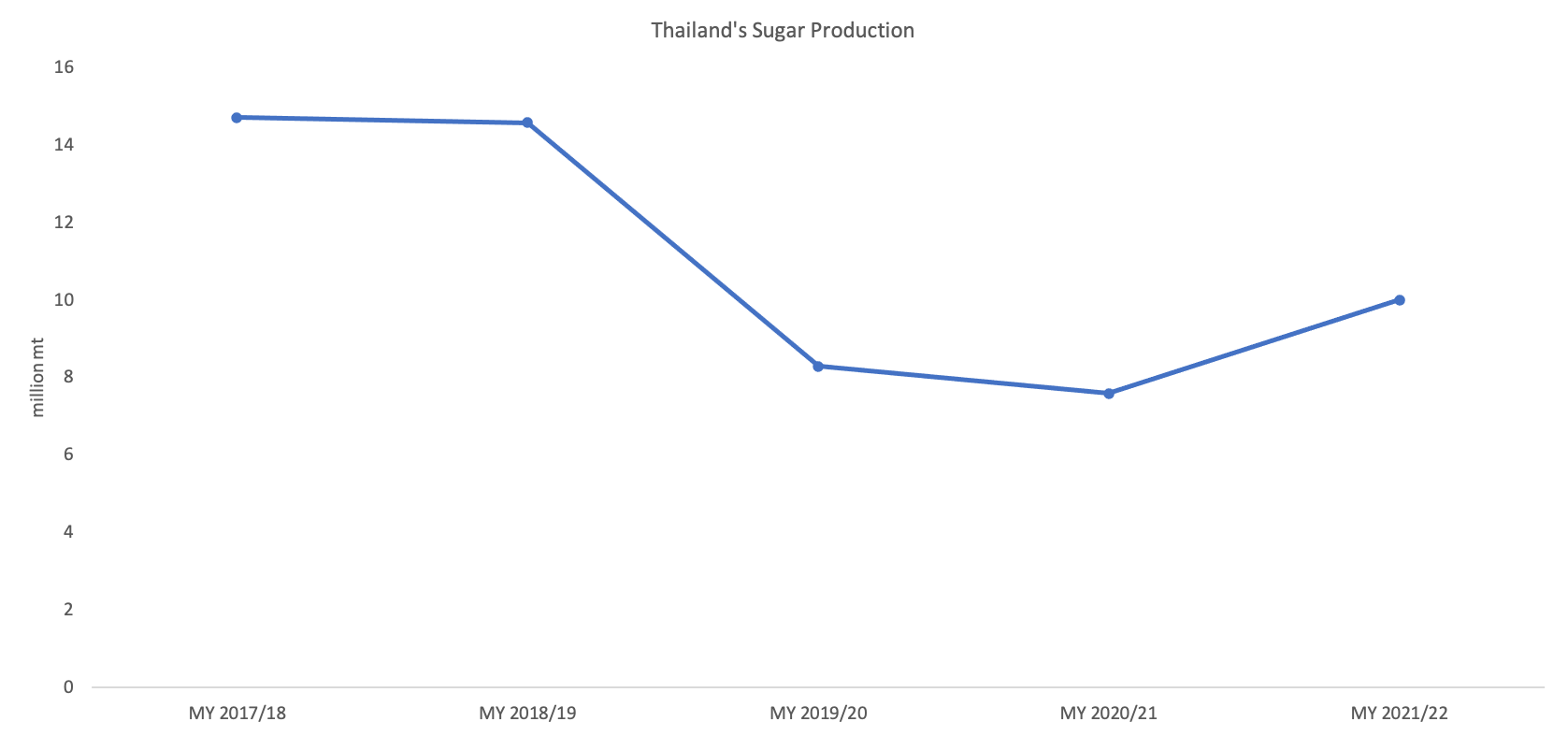

Thailand’s Sugar Production is Expected to Recover in MY 2021 - 22

Thailand is among the leading producers and exporters of sugar in the world. For the upcoming marketing year 2021-22 (October-September), it is expected that sugar cane production will increase compared to the previous seasons. The Thai sugar market is likely to return to usual production levels after two consecutive years of drought. Initially, it was anticipated that the trend of low production will continue even during MY 2021-22 since many farmers had shifted from sugar cane crops to other cash crops. Still, favorable weather conditions increased the yield of the existing crop. According to estimates fromS&P Global Platts Analytics, Thailand sugarcane production for MY 2021-22 is projected to be at 95 million mt and the sugar production at 10.5 million mt. Similarly, the Federation of Thai Industries (FTI) has estimated the cane production for MY 2021-22 to reach 85-90 million mt.

Source: USDA.

Improvement in sugarcane production was driven by favorable weather conditions during the cane growing period. According to the estimates of the Thai Meteorological Department, the average precipitation was 5-7% above average during the sugarcane tillering and elongation growth stages in major growing areas. Overall, the sugar cane-producing regions witnessed 15% higher rainfall in comparison to the previous year. The FTI is expecting that higher production levels will drive the sugar exports for the MY 2021-22 and help producers secure better prices in the global market. S&P Global Platts Analytics has projected the exports to reach 7.5 million mt, a YoY increase of over 100%.

Thailand’s recovery in sugar production is likely to increase its exports to one of the main markets - Indonesia. As per the Thai Sugar Milling Corporation Limited, Indonesia imports more than 2 million mt of raw sugar every year from Thailand but due to lower production, the country imported only 819,031 mt between January-October 2021, which is a YoY drop of approximately 61%. In 2020, it is expected that Thailand will regain its export competitiveness and capture the market again. Furthermore, the short distance between the countries signifies lower freight costs relative to importing sugar from other countries like Brazil and India.

Sugar processing and crushing have already started with a full boom in Thailand and are expected to end in the next few months. The country is currently facing a shortage of 100,000 workers who previously migrated from neighboring countries but are now unable to, given the ongoing pandemic. It is expected that the logistical challenges in securing freight to export its surplus supply to buyers in the region as well as competition from cargoes from India and Brazil will continue through this season. Despite some challenges, the outlook for MY 2021-22 remains positive with higher production and higher exports. Thailand’s sugar producers are looking forward to fetching better global prices.