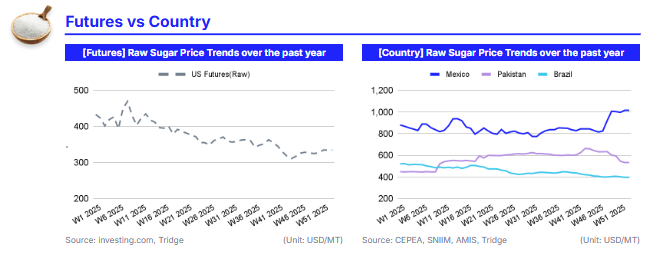

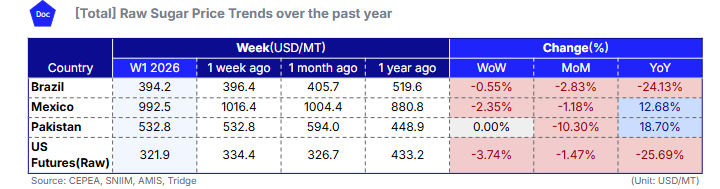

In W1 2026, global sugar markets softened further as surplus conditions and improving supply fundamentals continued to dominate price formation. In Brazil, domestic sugar prices declined 0.55% WoW to USD 394.2/mt, reflecting the recovery of the 2025/26 harvest and higher effective availability despite earlier weather and fire disruptions. Globally, surplus expectations remain firm, with the USDA projecting excess supply above 5 mmt, reinforcing a bearish-to-neutral outlook into early 2026. In Mexico, sugar prices fell 2.35% WoW to USD 992.5/mt as exports resumed and logistics normalized, easing domestic pressure despite structurally high absolute prices. In Pakistan, prices were flat WoW but softened on a monthly basis amid expectations of deregulation and reduced government intervention, weakening near-term price support. In the derivatives market, US raw sugar futures declined 3.74% WoW to USD 321.9/mt, trading within a narrow range as ample global supply capped upside momentum.

For a global food manufacturer sourcing Brazilian sugar, the core strategy is to prioritize near-term and staggered procurement from Brazil while prices remain compressed by surplus-driven fundamentals. Brazil should remain the primary sourcing anchor given its cost efficiency and supply resilience, while exposure to Mexico should be limited to tactical or spot needs due to policy- and cost-driven price inflation, and Pakistan should be treated as a non-core, policy-sensitive origin. This defensive and flexible sourcing approach balances cost control and protection against episodic volatility in an otherwise range-bound global sugar market.

1. Weekly Price Overview

Weak Brazilian Real, Rising Center-South Yields, and Policy Actions Drive Broad Sugar Price Declines

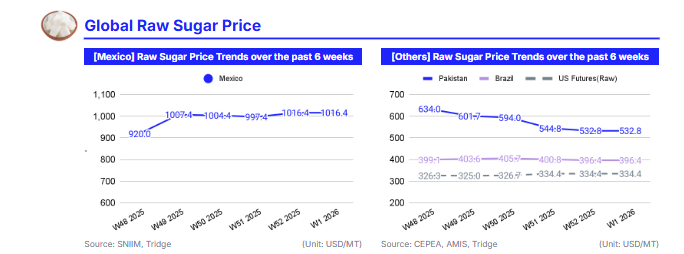

In W1 2026, global sugar markets softened further, reflecting sustained surplus conditions and improving supply fundamentals across key origins. In Brazil, domestic sugar prices declined 0.55% week-on-week (WoW) to USD 394.2 per metric ton (mt), pressured by a stronger-than-expected recovery in the 2025 harvest following weather and fire-related disruptions in 2024. While early-season productivity and Total Recoverable Sugars (ATR) were negatively affected by drought and partial field damage, improved weather and agronomic management supported a steady recovery through the year. According to the Brazilian Sugarcane Industry Association (UNICA), Center-South cane crushing reached 592.3 million metric tons (mmt) in the 2025/26 season to date (–1.92% YoY), while sugar production increased 1.13% year-on-year (YoY) to 39.9 mmt, reinforcing near-term availability. At the global level, the United States Department of Agriculture (USDA) estimates a surplus exceeding 5 mmt in the 2024/25 season.

Mexico’s sugar prices fell 2.35% WoW to USD 992.5/mt, reflecting easing domestic sentiment as exports resumed and logistics normalized. In late W52 2025, Mexico launched its first sugar export shipment of the 2026 season, with 15,000 mt of raw sugar shipped from Puerto Chiapas to the United States (US). This early export activity signaled adequate supply availability and helped relieve short-term domestic pressure, even as prices remain elevated in absolute terms due to structural costs and policy influences.

In Pakistan, sugar prices were flat WoW but declined 10.30% month-on-month (MoM), as expectations of deregulation and government disengagement from price controls weighed on market sentiment. Official statements indicating a targeted retail price decline toward USD 0.39 per kilogram (PKR 110/kg) and progress on deregulation reforms reinforced expectations of improved market balance, despite ongoing concerns over inflation and uneven retail pricing across regions. On the other hand, in the US, raw sugar futures declined 3.74% WoW to USD 321.9/mt, with prices trading in a narrow range around 14.7–14.9 c/lb during the week. Although futures briefly tested mid-week highs near 15.0 c/lb, ample global supply capped gains. Improving supply conditions in Brazil and persistent global surpluses continue to anchor sugar prices, limiting upside into early 2026, absent a material supply shock.

2. Price Analysis

Global Sugar Prices Consolidate at Lower Levels as Harvest Recovery and Rising Supply Cap Upside

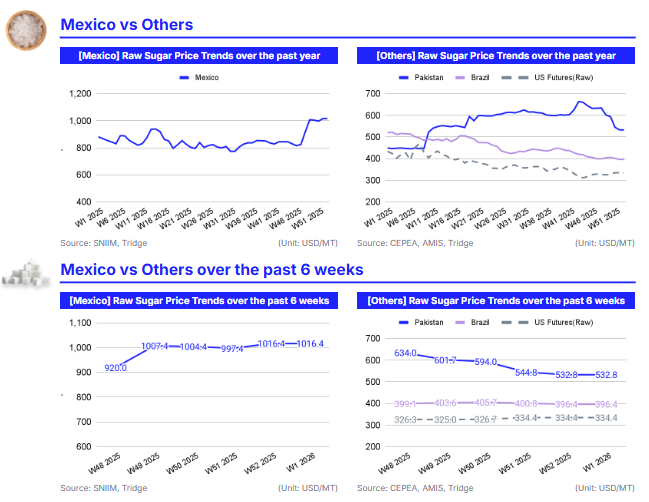

As of the latest assessment, sugar prices remain under pressure despite brief periods of stabilization, reflecting a market where supply resilience continues to outweigh earlier scarcity concerns. In Brazil, prices eased 0.69% WoW but remained marginally higher month-on-month (MoM) at USD 399.2/mt, indicating short-term consolidation rather than a trend reversal. The sharp decline observed through 2025 was primarily driven by the start of the 2025/26 harvest, which increased physical availability and steadily eroded the risk premium that had been embedded earlier in the year. Although the availability of higher-quality sugar remained tight and export volumes stayed broadly stable, falling international prices significantly reduced export revenues, weakening price support. The persistence of a domestic premium over export parity encouraged mills to prioritize local sales, reinforcing downward pressure on domestic benchmarks.

In Mexico, sugar prices rose 20.93% MoM to USD 824.8/mt despite recent WoW softness, reflecting a delayed adjustment from earlier tightness rather than a structural shift. A forecast production growth of around 7% in the 2025/26 marketing year (MY) points to improving supply conditions, which, combined with weaker margins, is likely to limit further price appreciation and gradually ease domestic prices as the season progresses. In Pakistan, sugar prices fell 6.53% MoM while remaining elevated YoY, highlighting the growing impact of policy uncertainty and softening domestic demand. Expectations of deregulation have weakened near-term price support by raising the prospect of higher production and exportable surpluses, shifting sentiment toward a looser market balance.

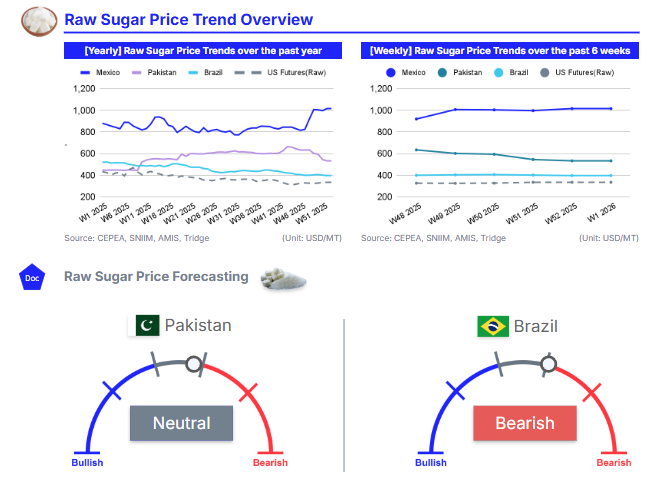

Looking ahead, global sugar prices are expected to remain range-bound with a bearish-to-neutral bias. Brazil’s steady harvest progression and weaker export realizations are likely to cap any sustained recovery. Meanwhile, rising production in Mexico and the potential for increased output and exports from Pakistan add to downside risks. Absent a material weather shock or an abrupt policy shift restricting supply, price movements over the coming months are more likely to reflect consolidation at lower levels rather than a durable upward trend.

3. Strategic Recommendations

Maintain Defensive Sourcing While Exploiting Origin-Specific Price Weakness

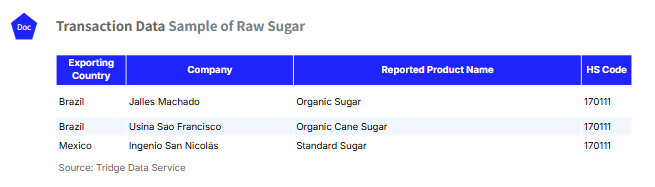

Given the prevailing surplus-driven balance and the bearish-to-neutral price outlook into early 2026, sugar procurement and trading strategies should remain defensive and flexible. Brazil’s steady harvest recovery, rising Center-South output, and weaker export realizations suggest limited upside risk, making Brazilian supply the most cost-efficient anchor for near-term coverage. Buyers should prioritize short-dated or staggered purchases from Brazil, leveraging competitively priced availability, including organic sugar from suppliers such as Jalles Machado and organic cane sugar from Usina São Francisco, as reflected in Tridge Eye’s transaction data. Any short-lived price rebounds should be treated as tactical opportunities to extend coverage incrementally rather than signals for aggressive forward locking.

In Mexico, elevated absolute prices remain vulnerable to normalization as production expands and exports resume. Traders with access to standard sugar from mills such as Ingenio San Nicolás should consider accelerating sales while current price levels persist. Buyers should limit forward exposure and rely on spot or nearby contracts. In Pakistan, declining prices and expectations of deregulation point to further downside risk; buyers are advised to defer commitments, while exporters should remain cautious until clearer policy direction emerges.

The recommended action plan is to remain lightly covered in low-cost Brazilian origins, monetize policy- or timing-driven price strength in higher-cost markets such as Mexico, and preserve optionality through short-term contracts and selective hedging. Absent a material weather shock or abrupt policy shift, this approach balances cost control with protection against episodic volatility in an otherwise range-bound global sugar market.