In W3 in the maize landscape, some of the most relevant trends included:

- The USDA revised global corn production for 2024/25 to 1.21 billion mt, with US production forecast to decrease to 377.63 mmt due to lower yields and exports declining to 62.23 mmt.

- Ukraine corn production is forecasted at 26.5 mmt, exports to the EU are slightly down, and maize prices surged 61.54% YoY due to drought.

- Due to dry conditions affecting yields and planting delays in key regions, Argentina's 2024/25 corn production estimate has been revised to 49 mmt.

- Brazil's corn production forecast for 2024/25 was revised slightly down to 122.39 mmt, with planting progress at 87.1% but drought affected some areas.

.

1. Weekly News

Global

USDA Lowered Global Corn Production Forecast to 1.21 Billion MT for 2024/25

The United States Department of Agriculture (USDA) revised the global corn production forecast for the 2024/25 season to 1.21 billion metric tons (mt). This is a reduction of 3.54 million metric tons (mmt) from the previous estimate, with exports and ending stocks also lowered to 191.41 mmt and 293.34 mmt, respectively. The Ukrainian corn harvest forecast remains steady at 26.5 mmt, with exports projected at 23 mmt and ending stocks at 0.64 mmt. Meanwhile, the United States (US) corn production forecast was significantly reduced by 7.01 mmt to 377.63 mmt. This is accompanied by lower export estimates of 62.23 mmt and a sharp decline in ending stocks by 5.03 mmt to 39.12 mmt. These adjustments reflect shifts in key markets for major corn exporters during the 2024/25 marketing year (MY).

Argentina

2024/25 Argentina Estimate Reduced Amid Dry Conditions

The 2024/25 Argentina corn production estimate has been lowered by 1 mmt to 49 mmt due to ongoing hot and dry conditions, with further reductions likely if rainfall does not improve. Most of the country remains dry, with temperatures reaching the mid-90s to low 100s (Fahrenheit) and expected to rise, intensifying crop stress. Early-planted corn in grain-filling stages has faced minimal impact. At the same time, Nov-24 planted corn is experiencing yield losses during pollination, and Dec-24 planted corn requires immediate moisture to avoid pollination issues. The southern core regions, including northern Buenos Aires and Southern Santa Fe, are most affected, while western Argentina retains better soil moisture. Planting progress has reached 91.6%, with Northern Argentina lagging at 45% planted.

Brazil

Brazil's 2024/25 Summer Corn Harvest Progressed Amid Drought Concerns

Brazil's National Supply Company (CONAB) reported that the 2024/25 summer corn planting reached 87.1% in W2, consistent with 2023/24, with key states except Piauí and Maranhão completing sowing. However, drought in Rio Grande do Sul and dry conditions in Paraná may impact productivity. Harvest progress stands at 2.3%, up from 1.1% the previous week but lagging behind last year’s pace for the same period.

Peru

Peru's 2024 Hard Yellow Corn Imports Surged 17.14% YoY, Dominated by Argentina

Peru imported 4.12 mmt of hard yellow corn in 2024, marking a 17.14% year-on-year (YoY) increase compared to the 3.52 mmt imported in 2023, as reported by the Supply and Price Information System (SISAP) under the Ministry of Agrarian Development and Irrigation (MIDAGRI). Monthly imports varied, peaking in Aug-24 at 521,036 mt. Argentina emerged as Peru’s primary supplier, accounting for 98.95% of the total imports with 4,080,643 mt, a significant 39.33% rise from 2.93 mmt in 2023. In contrast, imports from Brazil and other sources declined sharply, with Brazil contributing only 11,773 mt and other countries supplying 31,599 mt.

2. Weekly Pricing

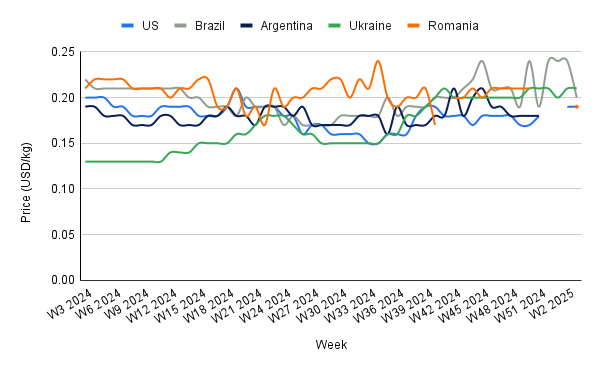

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W3 2024 to W3 2025)

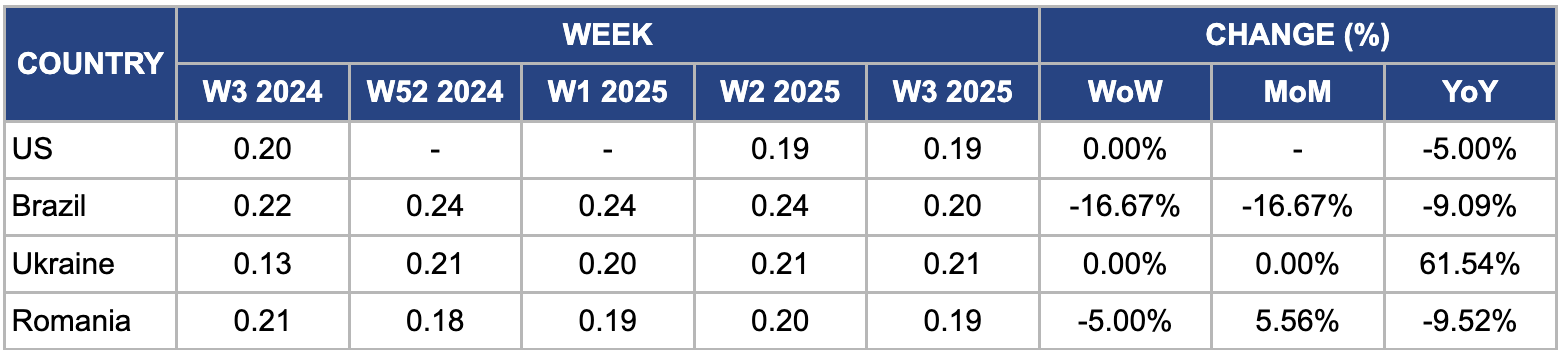

United States

In W3, wholesale maize prices in the US remained unchanged week-on-week (WoW) but declined 5% YoY, reaching USD 0.19 per kilogram (kg). Despite this, the USDA has revised its corn production forecasts for the 2024/25 season, projecting a decrease in yields to result in a corn harvest of 377.63 mmt, down by 7 mmt from the Dec-24 estimate. The lower production forecasts have also led to a projected drop in corn stocks in the US by 5.03 mmt by the end of the period.

Brazil

In W3, wholesale maize prices in Brazil dropped by 16.67% WoW and month-on-month (MoM), settling at USD 0.20/kg. According to USDA projections, Brazil's 2024/25 MY corn production is expected to reach 127 mmt, up from 119.74 mmt in the previous year. This increase is due to favorable weather and expanded planted acreage. Despite the production growth, domestic demand remains strong, supported by the livestock sector's requirements for feed and the food processing industry's needs. CONAB estimates Brazil's total corn crop for the season at 4,717 million bushels, reflecting a 3.6% YoY growth.

Ukraine

In W3, wholesale maize prices in Ukraine remained steady WoW but surged by 61.54% YoY, reaching USD 0.21/kg. This sharp price increase is primarily due to a significant reduction in maize production due to severe drought conditions. According to USDA projections, Ukraine's corn production is expected to decline to 25 mmt in 2024/25 MY, marking a 23% drop from the previous season and the lowest output since 2017. The drought has severely impacted crop yields, leading to tighter domestic maize supply, which has exerted upward pressure on prices.

Romania

In W3, Romanian maize prices decreased by 5% WoW to USD 0.19/kg, down from USD 0.20/kg. This decline is primarily due to favorable weather conditions that have improved maize yields, leading to increased supply. Moreover, the Romanian government has allocated approximately USD 25.65 million for irrigation systems, aiming to mitigate weather-related risks for spring crops. This investment is expected to enhance maize production efficiency and contribute to the increased supply, thereby exerting downward pressure on prices.

3. Actionable Recommendations

Develop Alternative Markets for Brazilian Corn Exports

While Brazil's corn production is growing, domestic demand remains strong, driven by the livestock and food processing sectors. To avoid over-saturation in domestic markets and to stabilize prices, Brazilian exporters should explore new and emerging markets in Asia and Africa, where corn demand is rising. Strengthening trade partnerships with countries like Indonesia, Vietnam, and Nigeria could provide alternative export outlets and reduce dependency on traditional markets, thereby supporting more stable prices for Brazilian corn. These strategies aim to enhance resilience in production, manage supply more effectively, and create alternative revenue streams for farmers, traders, and exporters amid shifting global corn dynamics.

Enhance Storage Infrastructure in Peru to Manage Corn Imports

Peru’s growing dependency on imported corn, primarily from Argentina, highlights the need for improved storage infrastructure to stabilize supply and prices. Expanding grain silos and storage facilities can help manage surplus imports during peak periods and avoid over-supply issues. Moreover, providing farmers and importers with training on proper storage techniques and ensuring timely distribution can reduce spoilage and improve market efficiency.

Encourage Crop Diversification for Corn Farmers

To combat the impact of dry conditions on corn production in Argentina, farmers can adopt drought-resistant corn varieties such as Pioneer P3525HR, BASF DEKALB DK 43-10, Monsanto DKC 64-89, Syngenta NK 40-05, AgReliant RL 20B32, and DLF Trifolium DroughtGard™, specifically bred to withstand water stress. These varieties feature strong root development, improved water-use efficiency, and early maturing traits that help conserve moisture and maintain yields even during periods of limited rainfall. By planting these drought-tolerant options, farmers can ensure better resilience to fluctuating weather patterns and reduce the risk of significant yield losses in dry regions.

Sources: Tridge, Agraria, NoticiasAgricolas, UkrAgroConsult