1. Weekly News

Colombia

Colombian Tomato Prices Fell 36% WoW in W37 Due to Increased Supply

In W37, the quality of fresh tomato in the Colombian Department of Risaralda improved due to favorable climate conditions during the harvest. This led to a shift in the market, with increased volumes driving prices down. The wholesale market in Pereira reported a 36% week-on-week (WoW) price drop, reaching USD 0.44 per kilogram (kg) by the end of W37.

Egypt

Egyptian Tomato Prices Expected to Decline in 20 Days with Arrival of Beni Suef Production

Egypt's tomato prices are expected to decline in W40 as production from Beni Suef Governorate reaches the markets. The current high prices are due to several factors, including early-season crop damage from high temperatures and reduced cultivation areas due to decreased revenues and increased expenses. The trend of Egyptians stockpiling tomatoes during price increases has exacerbated market volatility, contrasting with global practices where consumers often wait for prices to stabilize before purchasing. In W37, tomato prices ranged between USD 0.41 and 0.72/kg in various regions, including remote and upscale areas. Despite these challenges, Egypt remains a significant player in global tomato production, ranking sixth worldwide with an annual output of 6.2 million metric tons (mmt), following China, India, Turkey, the United States (US), and Italy.

Morocco

Concerns Raised Over High Pesticide Levels in Moroccan Tomatoes Supplied to the EU

A major supplier of tomatoes to the European Union (EU), Morocco has been reported to use high levels of pesticides, including banned substances like Dichlorodiphenyltrichloroethane (DDT), in its agricultural practices. This poses significant health and environmental risks. DDT, an extraordinarily effective but persistent insecticide, continues to be a concern despite its ban in many countries, including Hungary, which first prohibited its use in 1967. The widespread use of such harmful pesticides in Moroccan tomato cultivation raises serious questions about the quality of the produce and potential health hazards for consumers. While outsourcing tomato production to North Africa may offer economic advantages, contaminating half of Moroccan tomato samples with pesticides underscores the urgent need for stricter oversight and safer agricultural practices.

Peru

Peru's Tomato Exports Fell 75% YoY in Aug-24

Peru's tomato exports amounted to 486 metric tons (mt) in Aug-24, reflecting a 75% year-on-year (YoY) decline from 1,963 mt in Aug-23. The tomatoes were shipped to seven countries, with Brazil being the most prominent destination, accounting for 64% of the exports, followed by Colombia with a 17% share. Moreover, 13 purchasing companies were involved in this month's transactions.

Ukraine

Ukraine Tomato Prices Increased 17% WoW as Local Supply Drops

As of September 13, Ukraine is witnessing a significant upward trend in tomato prices, driven by reduced local supply and stable domestic demand. Greenhouse tomato prices were 17% WoW higher, reaching their highest level in the past seven years. This increase is due to decreased availability from local farms and higher prices for soil-grown tomatoes. Producers are now quoting prices for greenhouse tomatoes between USD 1.21 to 1.45/kg, reflecting the highest market prices in recent years.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

* Varieties: All tomato pricing is for round tomatoes.

Yearly Change in Tomato Pricing Important Exporters (W37 2023 to W37 2024)

* Varieties: All tomato pricing is for round tomatoes

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

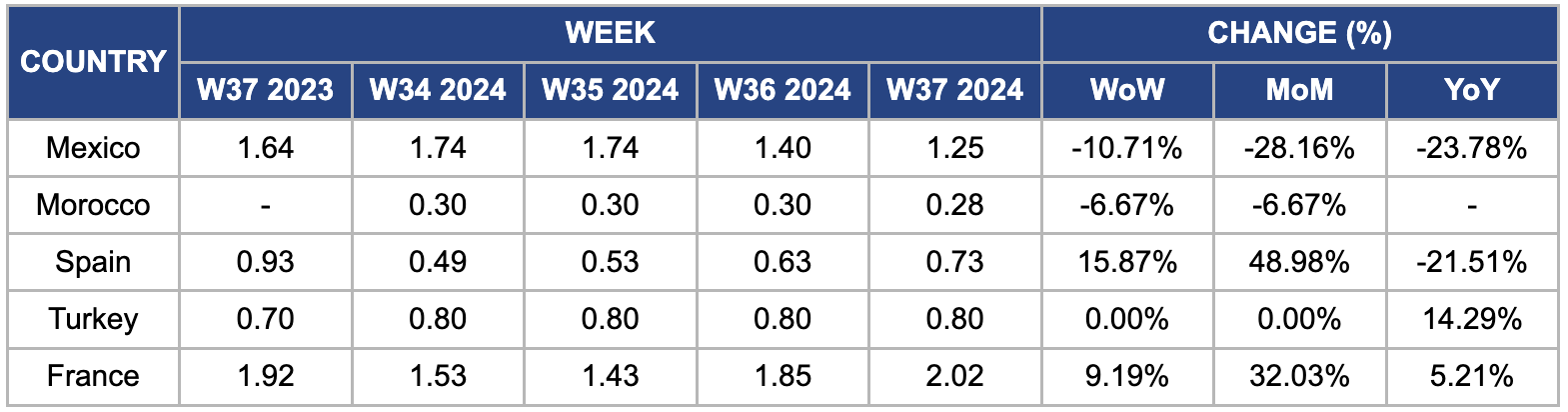

Mexico

In W37, wholesale tomato prices in Mexico saw a notable decrease of 10.71% WoW, falling to USD 1.25/kg. Prices also dropped 28.16% month-on-month (MoM) and 23.8% YoY. This decline is linked to an anticipated 2% increase in Mexico's tomato production in 2024, rising to 3.30 mmt from 3.22 mmt in 2023. The expected rise in production has contributed to price stabilization and the recent bearish trend. While some producers have invested in protected cultivation to mitigate risks, many regions rely on open-field farming, which is more vulnerable to climatic conditions and results in lower yields.

Morocco

In W37, Moroccan tomato prices dropped 6.67% WoW and 6.67% MoM to USD 0.28/kg. This decline is primarily due to overproduction late in the 2024 season, aggravated by high temperatures, leading to a significant fall in local and export prices. Moreover, Moroccan tomato exports to the EU decreased by 6.8% from Sept-23 to May-24, further impacting prices. Despite this downward trend, there are indications of a reduction in tomato cultivation acreage, with estimates suggesting a 10 to 15% YoY decrease from the previous season, a scenario that could result in elevated prices in the coming weeks.

Spain

In W37, Spain's wholesale tomato prices surged by 15.87% WoW, increasing from USD 0.63/kg to USD 0.73/kg. This sharp rise is due to seasonal fluctuations as the summer tomato production cycle winds down while early autumn varieties are unavailable. Additionally, adverse weather conditions, including intense heat waves and erratic rainfall, have disrupted yields, further constraining supply. These factors combined to push prices higher. Despite the weekly increase, prices remain 21.5% lower YoY, as last year's elevated export demand from Northern Europe and the Middle East and limited domestic supply had driven local prices up when exporters prioritized international markets over domestic needs.

Turkey

In W37, Turkey's tomato prices held steady WoW at USD 0.80/kg but saw a 14.29% YoY increase. This rise is due to worsening drought conditions tied to climate change, affecting agricultural productivity. Adding to the pressure, soaring diesel fuel and transport costs have increased prices. The situation has become untenable for many farmers, sparking frequent protests in key agricultural provinces like Bursa, Kahramanmaras, and Balikesir. In Gaziantep, frustrated farmers have taken drastic steps, dumping unsold tomatoes on roads to highlight their plight, as inflation and mounting costs leave them with shrinking profits. This unrest is a clear signal that Turkey's agricultural sector is under immense strain, with the ongoing drought and economic hardships threatening long-term sustainability if not addressed decisively.

France

In W37, tomato prices in France rose significantly by 9.2% WoW, 32% MoM, and 5.2% YoY, reaching USD 2.02/kg. This makes French tomatoes the most expensive among global suppliers, including Mexico, Turkey, Spain, and Morocco. Despite a generally favorable growing season, adverse weather events in Aug-24, such as heavy rains and heatwaves, negatively affected tomato quality and yields in some regions, reducing yields by 10 to 15% YoY. Additionally, disruptions in the supply chain, including transportation strikes and increased fuel costs, have further escalated distribution expenses. Transportation costs have risen by approximately 12% due to higher fuel prices and logistical delays, contributing to the overall increase in tomato prices.

3. Actionable Recommendations

Enhance Tomato Cultivation Practices in Morocco

Moroccan farmers should adopt more precise and sustainable farming techniques to improve yield quality and reduce the impact of climatic factors. Investing in weather-resistant tomato varieties and advanced irrigation systems can help manage environmental challenges. Additionally, better planning and management of cultivation areas can prevent overproduction and stabilize market prices. Strengthening export strategies and diversifying export destinations will also help mitigate the effects of local price declines.

Revitalize Peru's Tomato Export Strategy

Peruvian authorities and industry stakeholders should focus on enhancing the competitiveness of their tomato sector by improving production efficiency and exploring new export markets. Investing in quality control and certification processes can help meet international standards and boost buyer confidence. Developing targeted marketing strategies and strengthening trade relationships with critical destinations like Brazil and Colombia can help increase export volumes and stabilize market presence.

Enhance Tomato Production Resilience in Egypt

With Egyptian tomato prices expected to decline due to the arrival of Beni Suef production, it is essential to enhance production resilience to mitigate future price volatility. Egyptian farmers should invest in technologies and practices that reduce crop damage from adverse weather and improve overall yield stability. Developing better irrigation systems and adopting more resilient tomato varieties can help manage the effects of high temperatures and other environmental factors. Furthermore, strengthening market mechanisms to balance stockpiling practices and prevent extreme price swings will contribute to more stable pricing in the long term.

Sources: Tridge, Portaldelcampo, AgroForum, Amal News