.jpg)

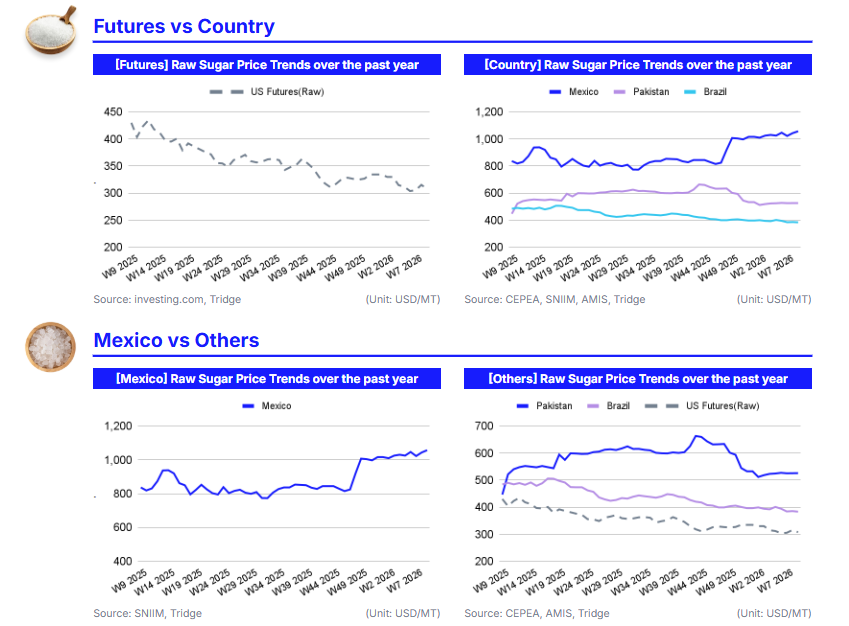

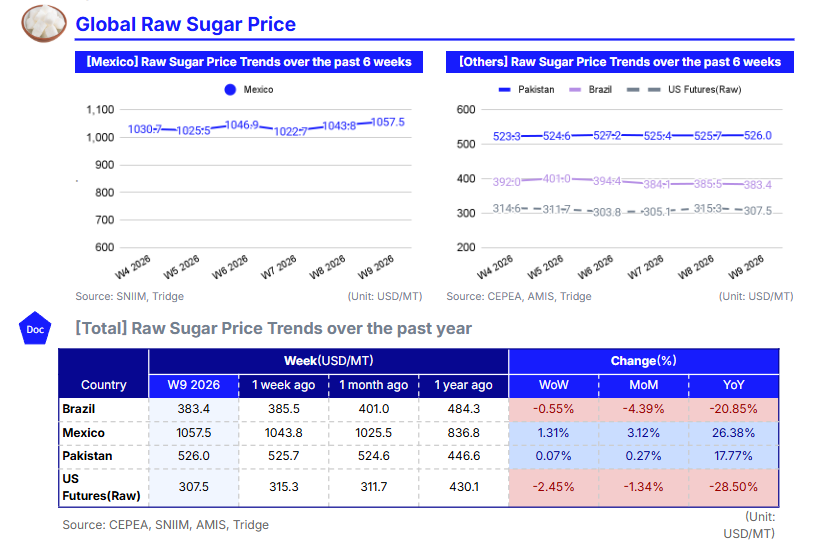

As of W9 2026, global sugar prices remain under pressure as ample supply and strong export flows continue to dominate market fundamentals. Brazil’s prices declined 0.55% WoW and 4.39% MoM to USD 383.4/mt, remaining 20.85% lower YoY as high shipment volumes and competitive pricing reinforce the country’s role as the primary global supply anchor. US raw sugar futures also weakened, reflecting oversupply and slower demand growth, while Mexico’s prices rose modestly due to protective trade policies and producer support programs. Pakistan’s prices increased slightly as imports surged, indicating localized supply tightening rather than a shift in global fundamentals.

For sourcing Brazilian raw sugar, the core strategy is to prioritize Brazil as the primary procurement origin while implementing staggered purchasing to capture potential additional price declines. Brazil’s consistent export availability, confirmed by active shipments and transaction flows from suppliers such as Jalles Machado, provides the most cost-efficient sourcing base under the current surplus environment. Mexico should remain a secondary origin for refined sugar when policy support sustains higher prices, while Pakistan should be treated as a short-term trading market rather than a stable sourcing base due to its growing import dependence and regulatory uncertainty.

1. Weekly Price Overview

Global Sugar Prices Diverge as Brazil Weakens, Mexico Strengthens on Policy Support, and Trade Shifts Drive Market Volatility

In W9 2026, global sugar prices showed mixed movements across key producing countries, reflecting localized policy developments and demand adjustments within an otherwise well-supplied global market. Brazil’s sugar prices declined by 0.55% week-on-week (WoW) to USD 383.4 per metric ton (mt). Domestically, the Center for Advanced Studies on Applied Economics (CEPEA/ESALQ) indicator for white crystal sugar also fell 1.42% to USD 19.14/50 kilogram bag (BRL 100.45/50 kg bag), with the physical market in São Paulo accumulating a 4.23% decline in Feb-26. The drop reflects weakening domestic demand and pricing adjustments by mills in response to softer international conditions, reinforcing Brazil’s role as a competitive low-cost origin in the global market.

In Mexico, sugar prices increased by 1.31% WoW to USD 1,057.5/mt as government initiatives aimed at strengthening the sugarcane sector improved market sentiment. Programs led by the Ministry of Agriculture and Rural Development (SADER) are expanding access to financing at preferential interest rates of 8.5% and integrating producers into welfare support mechanisms to improve liquidity and productivity. At the same time, authorities are tightening trade regulations through high ad valorem tariffs on imported sugar to curb smuggling and protect domestic producers, factors that continue to support elevated domestic price levels.

Pakistan’s sugar prices rose slightly by 0.07% WoW to USD 526.0/mt amid a sharp increase in imports. Between Jul-25 and Jan-26, sugar imports surged to more than USD 17.46 million compared with just USD 211,800 during the same period last year, highlighting growing reliance on foreign supply. Furthermore, investigations into alleged irregularities involving government sugar stocks have introduced additional uncertainty into the domestic market.

In the United States (US), raw sugar futures declined by 2.45% WoW despite a late-week rebound that lifted the Mar-26 contract to 14.30 cents per pound (lbs). The recovery followed a decision by the US Supreme Court to revoke trade tariffs introduced during the previous administration, a move expected to improve the competitiveness of Brazilian sugar in the US market and potentially reshape global trade flows. Global sugar prices remain influenced by ample supply availability, with policy adjustments and trade developments generating short-term volatility across regional markets.

2. Price Analysis

Global Sugar Prices Remain Weak as Brazilian Export Supply and Global Surplus Continue to Weigh on the Market

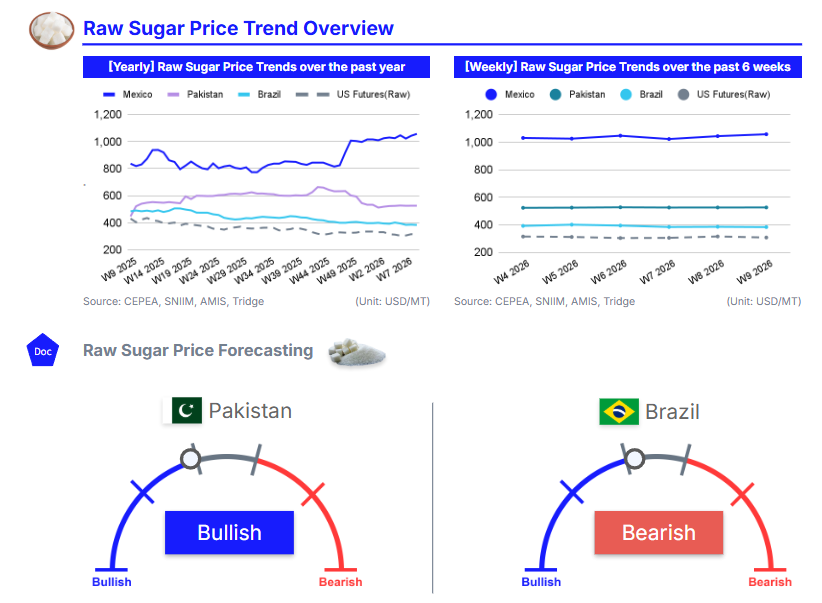

In W9 2026, global sugar markets continued to reflect oversupplied conditions, with most benchmarks declining or showing only limited monthly recovery. In Brazil, sugar prices fell 4.39% month-on-month (MoM) and 20.85% year-on-year (YoY) to USD 383.4/mt. The decline is primarily driven by strong export availability and sustained shipment flows. Port data show 1.576 million tons scheduled for export, led by the Port of Santos, confirming Brazil’s continued ability to supply large volumes to international markets. Export statistics reinforce this dynamic: although Feb-26 shipments increased 44% YoY, the average export price dropped 22.6% to USD 370.1/mt. This combination of expanding export volumes and falling unit prices indicates that global buyers remain well supplied, forcing exporters to compete primarily through pricing.

In Mexico, sugar prices increased 3.12% MoM but remain significantly lower YoY, reflecting structural inefficiencies in the agricultural sector rather than tightening supply conditions. Heavy reliance on imported fertilizers and persistent productivity constraints limit domestic production growth and increase cost volatility. The modest monthly price increase appears to reflect short-term market adjustments rather than a structural shift toward tighter supply.

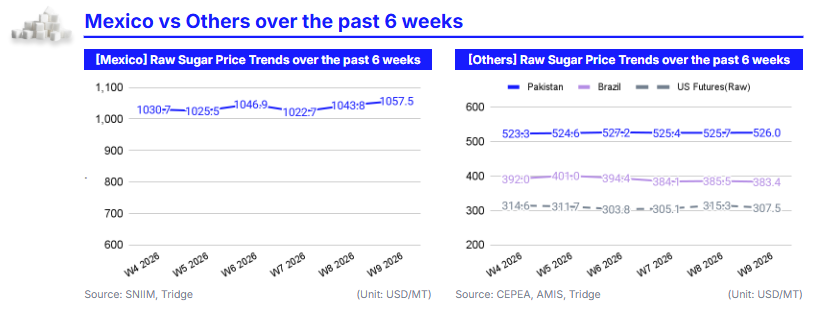

Pakistan’s sugar prices rose slightly by 0.27% MoM and remain 17.77% higher YoY at USD 526/mt. The increase is largely linked to tightening domestic availability, as evidenced by a 7,906% surge in sugar imports between Jul-25 and Jan-26. The sharp rise in imports suggests that local supply constraints are forcing the market to rely more heavily on international sources, temporarily supporting domestic prices despite the broader global surplus.

In the US, raw sugar futures declined 1.34% MoM and remain 28.50% lower YoY, reflecting persistent downward pressure from global oversupply and weakening demand. Lower international prices are encouraging imports, while structural demand shifts, including reduced sugar consumption linked to GLP-1 weight-loss medications, are limiting consumption growth.

Global sugar prices are likely to remain under downward pressure or move within a narrow range. Brazil’s strong export capacity and high shipment volumes continue to anchor global supply, while demand growth remains relatively modest. Although localized tightening in markets such as Pakistan may generate temporary price support, the broader balance suggests a neutral-to-bearish outlook unless significant weather disruptions reduce production in major exporting countries.

3. Strategic Recommendations

Prioritize Brazilian Supply While Maintaining Flexible Procurement to Capture Further Downside

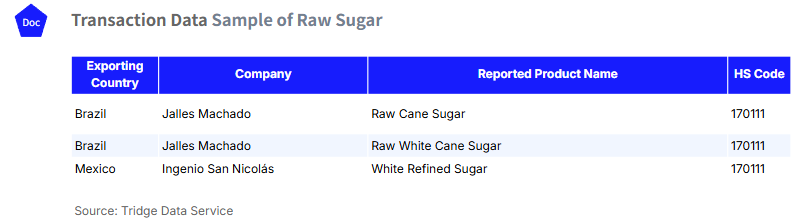

Given the current oversupplied market structure and the neutral-to-bearish price outlook, sugar importers and traders should prioritize sourcing from Brazil while maintaining flexible procurement strategies. Brazil’s prices have declined both WoW and MoM and remain significantly lower YoY, reflecting strong export availability and sustained shipment flows. With more than 1.5 mmt scheduled for export and volumes rising despite falling unit prices, Brazil continues to act as the primary global supply anchor. According to Tridge Eye’s transaction data, Brazilian suppliers such as Jalles Machado are actively exporting Raw Cane Sugar and Raw White Cane Sugar, confirming consistent availability for international buyers. Importers should therefore secure short- to medium-term physical coverage from Brazil while prices remain compressed.

From a trade execution perspective, buyers are advised to adopt a staggered purchasing strategy rather than locking in large forward volumes. This approach allows importers to capture potential additional downside as global inventories remain comfortable and export competition intensifies. Opportunistic procurement should be considered during short-term price rebounds, while maintaining partial exposure to benefit from continued downward pressure in international benchmarks.

Mexico should be treated as a secondary and tactical origin. Although domestic prices increased recently, the rise appears primarily policy-driven and supported by trade restrictions rather than tightening supply fundamentals. According to Tridge Eye’s transaction data, refined sugar from suppliers such as Ingenio San Nicolás remains available in the market, suggesting that traders holding inventory should consider accelerating sales into the current elevated price window before prices normalize.

In Pakistan, the sharp surge in sugar imports indicates tightening domestic availability but does not signal a structural shift in global supply conditions. Traders should therefore approach this market cautiously, focusing on short-term trading opportunities rather than building large long positions.

The recommended action plan is to secure incremental coverage from Brazilian suppliers over the next two to three months, monetize relative price strength in Mexico where possible, and maintain flexible procurement strategies to benefit from potential further price declines in the global sugar market.