The US Broiler Industry: Increasing Production, Exports, and Consumption Amid HPAI Outbreak

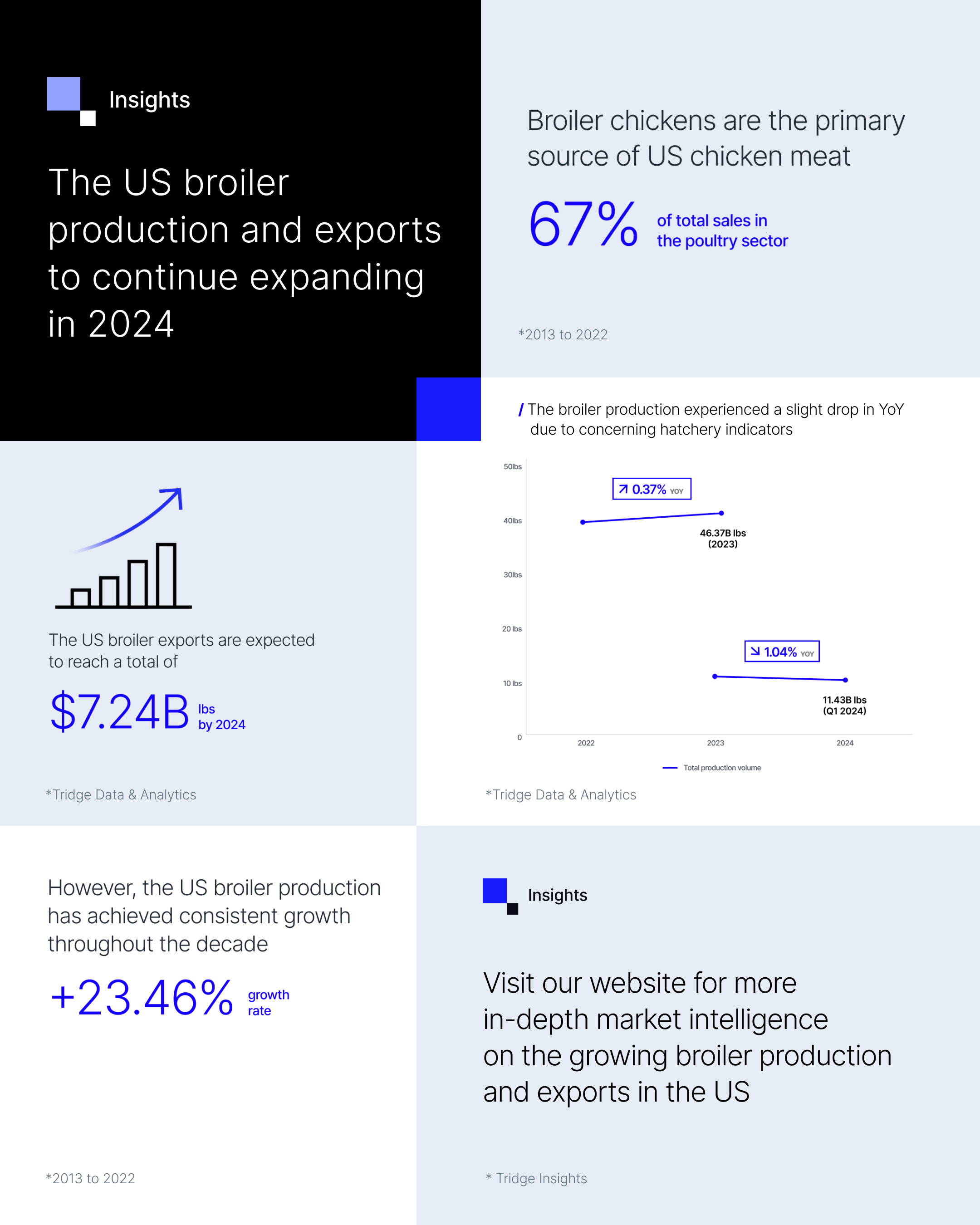

The United States (US) plays a substantial role in the global chicken market, standing as one of the leading countries in broiler production and exports. Competitive production frameworks and widespread consumer preference underpin this dominance. According to the United States Department of Agriculture (USDA), broiler chickens, the primary source of US chicken meat, constituted an average of 67% of total sales in the poultry sector from 2013 to 2022.

Consistent Increase in US Broiler Production

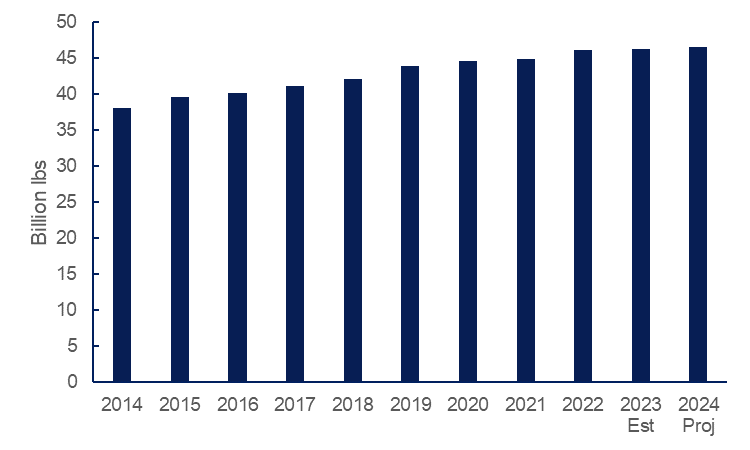

From 2013 to 2022, US poultry production, particularly broiler output, significantly expanded, reaching 46.21 billion pounds (lbs) in 2022, a significant 23.46% increase over the decade. This growth can be attributed to producers aiming to meet the rising demand from domestic and global consumers. The USDA estimates US broiler production at 46.37 billion lbs in 2023, a modest 0.37% rise compared to 2022.

However, US broiler production is expected to reach 11.43 billion lbs in Q1-2024, a slight 1.04% drop compared to Q1-2023. This pessimistic outlook is attributed to bleak hatchery indicators. The USDA’s National Agricultural Statistics Service (NASS) Chickens and Eggs report indicated that there were 681.5 million broiler-type eggs in incubators at the start of Nov-23, a drop of 3.7% compared to the same period in 2022 but close to the five-year average. Notably, broiler-type eggs in incubators on the first of each month in 2023 have dropped consistently since Jun-23. During the week ending December 23, 2023, US hatcheries set 239.86 million broiler-type eggs in incubators, a slight 0.29% decrease from the previous week and a modest 0.07% drop over the same period in 2022. Despite these challenges, projections suggest a marginal 0.56% year-on-year (YoY) increase in broiler production for 2024, reaching approximately 46.63 billion lbs.

Figure1: US Broiler Production

Understanding the Factors Driving the Expansion of US Broiler Production

According to the National Chicken Council, the US broiler production sector has consistently maintained an average YoY growth rate of 2% since 2000. This sustained growth is primarily attributed to the adoption of a vertical integration model within the sector. Vertical integration involves consolidating independent suppliers across various production stages into a single firm. In this system, a poultry company takes ownership and control of crucial components such as the hatchery, feed production, processing plant, transportation, and marketing. However, the live grow-out operations are contracted to external entities. This means that the chickens, feed, and transportation are all managed by the poultry companies, while the facilities where the birds are raised are owned and operated by independent contract farmers.

The contract established between the poultry entity and the grower outlines that the company will supply the birds, feed, and management guidance, while the grower is responsible for providing facilities, utilities, and labor for the bird-rearing process. This contractual arrangement proves advantageous for growers as it cushions them from the risks associated with fluctuations in input commodity prices and market uncertainties. Despite that, growers face challenges like increasing utility and facility costs, especially since they often operate in highly leveraged single-use facilities.

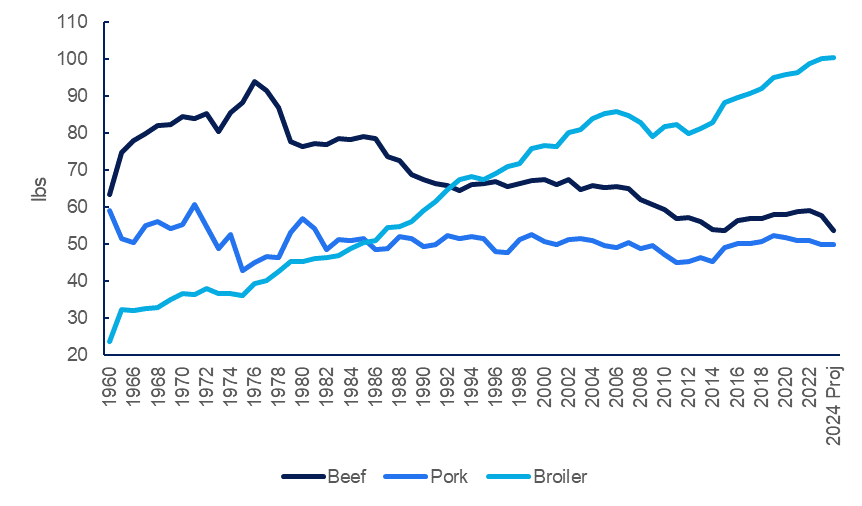

Another factor contributing to sustained broiler production growth in the US is consistently increasing consumption. According to USDA estimates, broiler per capita consumption in the US is projected to reach 100.1 lbs in 2023, a 1.21% YoY increase and a substantial 324.15% rise compared to the 23.6 lbs recorded in 1960. Projections further anticipate a 0.5% increase in 2024 compared to the 2023 forecast, reaching 100.6 lbs. Notably, broiler per capita consumption has consistently exceeded that of beef since 1993 and pork since 1986. This consistent growth is primarily attributed to the pricing advantage of broiler meat compared to beef and pork, making it a more attractive option for consumers. Additionally, changing consumer preferences towards healthier alternatives has played a role, with chicken being perceived as a wholesome choice.

Figure 2: US Per Capita Meat Consumption Trend

US Broiler Exports Witnessing an Overall Upward Trend

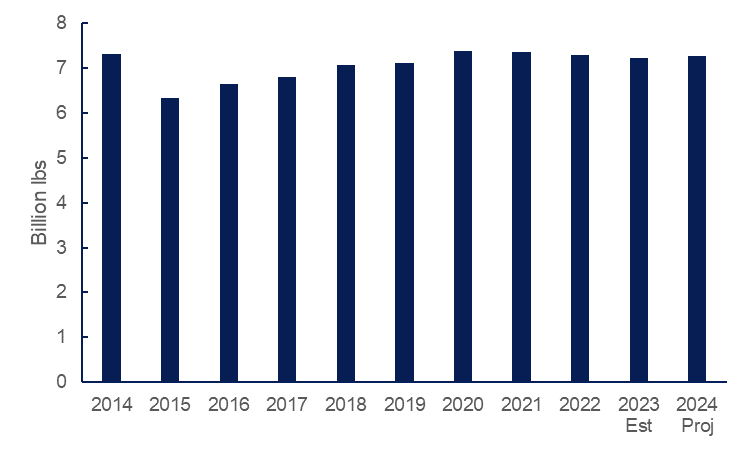

The sustained increase in broiler production in the US has created lucrative export opportunities for farmers. USDA data reveals that approximately 17% of domestic broiler production was exported from 2013 to 2022. Projections suggest that US broiler exports will amount to 7.21 billion lbs in 2023, a modest 1.1% drop compared to 2022. Despite the expected dip in 2023, US broiler exports have shown an overall upward trend since 1960. A slight rebound is anticipated in 2024, with US broiler exports estimated at 7.24 billion lbs, a marginal 0.42% YoY increase.

Figure 3: US Broiler Exports

The consistent growth in US broiler exports over the past decades can be attributed to increasing global chicken consumption due to its pricing competitiveness compared to beef and pork. Notably, since 2022, most people have turned to cheaper meat alternatives like chicken amid the high inflation and living costs. Moreover, changing consumer preferences towards healthier alternatives, with chicken being perceived as a healthy choice, has played a significant role. The majority of US broiler exports consist of leg quarters, with Mexico being the most significant foreign market.

Avian Influenza Posing Challenges to the US Poultry Industry

Despite the persistent growth in US broiler production, the sector has encountered significant uncertainty stemming from emerging diseases like highly pathogenic avian influenza (HPAI) and other challenges. In the last decade, the US experienced two devastating HPAI events: one in 2014/2015, affecting around 50.4 million birds and incurring losses of nearly USD 1 billion in control costs. The most recent outbreak, observed in 2022 and 2023, impacted over 58 million birds, with 77% in the commercial egg industry, 17% in turkey production, 5% in broiler production, and the remainder in the backyard or other poultry flocks. While cases in wild birds have decreased, there is still a threat from new chicks hatched in summer nesting grounds.

Culling, a biosecurity measure employed during HPAI outbreaks, leads to a reduction in bird population, affecting production. While less severe than the 2022 outbreak, 8.1 million birds were culled in 2023, with notable losses in Iowa and Minnesota. The spread of HPAI is expected to influence poultry trade, as importing countries may impose bans on shipments to prevent the virus's spread. For instance, Singapore recently suspended importing raw poultry and poultry products from regions affected by HPAI outbreaks, including parts of Japan, the US, Canada, France, Belgium, and Germany. Despite stringent biosecurity measures, the virus continues to pose challenges for poultry farmers, with reported cases in various US states.