.jpg)

1. Weekly News

Afghanistan

Afghanistan's Wheat Production Increased 10% YoY in 2024

As the National Authority for Statistics and Information of the Islamic Emirate reported, Afghanistan's wheat production reached 4.83 mmt by Oct-24, reflecting a 10% year-on-year (YoY) increase. This rise occurs amidst a severe humanitarian crisis affecting over 23 million Afghans, who continue facing poverty and food insecurity. The crop area was estimated using remote sensing technology and satellite imagery, with total wheat cultivation spanning 12.2 million hectares (ha), or about 70% of Afghanistan's agricultural land. The area of irrigated land increased by 2.8% over the past year, while rainfed farming expanded by 8.2%. Timely seasonal rains and a shift from opium poppy to wheat cultivation largely drove this growth. The central irrigated lands for wheat are in southern provinces like Helmand, Kandahar, Farah, and Kunduz. At the same time, rainfed farming is more common in northwestern regions such as Takhar, Herat, Badghis, and Faryab. Despite this notable increase in production, Afghanistan still faces a wheat deficit, with an estimated need of about 6.82 mmt, leading to a shortfall of approximately 2 mmt.

Australia

Dry Weather and Frost Cut into Australia's Wheat Yield

Persistent dry weather in Southern Australia, compounded by severe frost damage in mid-Sep-24, impacted wheat yields, though the country may still achieve an above-average harvest. Lower wheat production from Australia, a significant exporter, would strain a global market that's already challenged by dryness in critical regions like Argentina, the United States (US), and the Black Sea. Australian government forecasts from early September projected a robust 31.8 mmt wheat harvest, surpassing last season's 26 mmt and the five-year average of 29.8 mmt. However, Commonwealth Bank analysts noted worsening conditions in South Australia and Victoria, where some farmers are shifting to hay production instead of harvesting wheat. Current production estimates are 2.8 mmt for South Australia and 3.6 mmt for Victoria, down from their five-year averages of 4.7 mmt and 4.6 mmt, respectively.

Russia

Russian Wheat Exports Set to Break Oct-24 Record

Russia projects wheat exports in Oct-24 to reach 5.4 mmt, surpassing the record of 5.1 mmt in Oct-23. This increase is due to rising export prices and strong global demand for Russian wheat. From Jul-24 to Oct-24, total wheat exports were estimated at 20.3 mmt, slightly above last season’s record of 20.2 mmt. This growth has occurred despite Russia's halt in wheat exports to Kazakhstan since Aug-24 due to an import ban, with only 178 thousand metric tons (mt) exported to Kazakhstan from Jul-24 until the ban, compared to nearly 450 thousand mt during the same period last season.

Russian Wheat Exports to China Surged in 2024

According to China's State Customs Administration (GACC), China imported USD 8.697 million worth of Russian wheat on Sep-24, a 1.4-fold increase from USD 6.05 million on Sep-23. This growth placed Russia as the third-largest wheat supplier to China for the month, following Canada at USD 30.8 million and the US at USD 23.8 million. From Jan-24 to Sep-24, Russian wheat exports to China surged to USD 74.8 million, a substantial rise from USD 14.95 million in the same period of 2023. This positions Russia sixth in total wheat exports to China, behind Australia, Canada, France, the US, and Kazakhstan.

Saudi Arabia

Wheat Imports to Saudi Arabia Projected to Increase in 2024/25

According to the United States Department of Agriculture (USDA), wheat imports to Saudi Arabia for the 2024/25 season are projected to increase to 4.25 mmt, a 2% rise from 4.16 mmt in the 2023/24 season. In the 2023/24 season, Russia emerged as the dominant wheat supplier to Saudi Arabia, holding a market share of 49%, followed by European Union (EU) countries at 41% and Brazil at 10%. Wheat production in Saudi Arabia for the current season is expected to reach 1.5 mmt, up from 1.2 mmt in 2023/24 and 625 thousand mt in 2022/23. The General Directorate of Food Security (GFSA) has committed to purchasing up to 1.5 mmt of locally produced wheat in 2024/25 to support its anticipated consumption of 4.69 mmt.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W43 2023 to W43 2024)

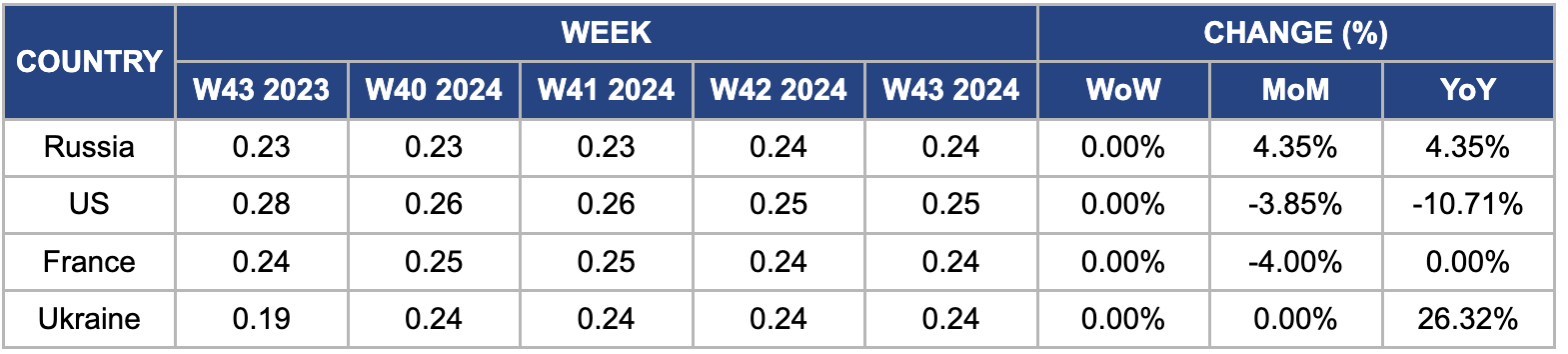

Russia

Russian wheat prices remained unchanged week-on-week (WoW) but increased by 4.35% month-on-month (MoM) and YoY, reaching USD 0.24 per kilogram (kg) in W43. This price increase is due to severe drought conditions affecting several regions, particularly Oryol, which has declared a state of emergency. Extreme weather events and earlier frosts have negatively impacted the 2024/25 wheat production forecast, creating challenges for farmers regarding wheat sales and reducing market liquidity. Moreover, concerns regarding winter planting for the 2025/26 crop have risen, prompting the Russian Grain Union (RGU) to advocate for export restrictions. The union urges the agriculture ministry to better reevaluate the export quota methodology to align it with global demand and seasonal potential.

United States

In W43, US wheat prices fell by 3.85% MoM and 10.71% YoY, reaching USD 0.25/kg, primarily due to increased supply. According to the USDA, the projected US wheat production for 2024 is 1.971 billion bushels, representing a significant 9% YoY increase and marking the highest level since 2016. The average yield is expected to rise to 51.2 bushels per acre, up from 48.7 bushels per acre in the previous year. Winter wheat production is anticipated to increase by 9% YoY to 1.349 billion bushels, while spring wheat production, excluding durum, is forecasted at 542 million bushels, reflecting an 8% increase from 2023. Despite these favorable production forecasts, weak demand, intense competition from Black Sea suppliers, and disappointing US export sales are impacting the market.

France

In W43, French wheat prices fell by 4% MoM to USD 0.24/kg, despite the International Grains Council's (IGC) revised global wheat production forecast for the 2024/25 season. This decline is due to poor harvest conditions in France, where heavy rainfall damaged crops. According to FranceAgriMer data, French farmers are nearing the completion of their soft wheat harvest. France is expected to record their smallest harvest since the 1980s due to adverse weather conditions, which have also negatively impacted the maize crop. This downturn is particularly concerning in exports to key markets such as Morocco, Algeria, and Tunisia, which have historically been significant destinations for French wheat.

Ukraine

In W43, Ukrainian wheat prices remained stable WoW but saw a significant increase of 26.32% YoY, reaching USD 0.24/kg . This price rise is mainly due to concerns over drought conditions threatening winter wheat planting for the 2025 harvest. The ongoing war and adverse weather have reduced the area sown with winter wheat, estimated at approximately 4.2 million ha in 2024, down from 4.4 million ha the previous year. The anticipated smaller harvest and lower carryover stocks have further constrained the exportable surplus, exerting additional upward pressure on prices.

3. Actionable Recommendations

Implement Market Intelligence and Risk Management

Saudi Arabia should develop a comprehensive market intelligence system to monitor global wheat production trends, pricing fluctuations, and emerging supply chain risks. This system would enable policymakers and industry stakeholders to make informed decisions based on real-time data, helping them anticipate market changes and adjust procurement strategies accordingly. Moreover, implementing robust risk management strategies, such as forward contracts, options, or hedging instruments, will help mitigate the impact of price volatility on wheat imports, ensuring more predictable costs for producers and consumers. Given that Saudi Arabia heavily relies on wheat imports to meet its growing consumption needs, having a proactive approach to market analysis and risk management will be crucial in securing its food supply and supporting its goal of achieving greater food security in the region. By staying ahead of market trends and potential disruptions, Saudi Arabia can better navigate the complexities of the global wheat market and ensure a stable supply for its population.

Invest in Irrigation Infrastructure

Australia should prioritize investments in irrigation infrastructure and water management systems to address the challenges of persistent dry weather and recent frost damage affecting wheat yields. Since the country is a significant player in the global wheat market, enhancing irrigation capabilities is crucial to improve yield stability and reduce vulnerability to adverse weather conditions. Expanding irrigation coverage in key wheat-growing regions, such as South Australia and Victoria, will help ensure more consistent production levels, even during periods of drought. Moreover, implementing advanced water management technologies, such as precision irrigation and rainwater harvesting systems, can optimize water usage and enhance crop resilience. By increasing the reliability of wheat production, Australia can better maintain its export capacity and support global food supply needs amid growing demand and climatic uncertainties.

Diversify Supply Sources

Afghanistan should diversify its wheat import sources beyond traditional suppliers like Pakistan and Iran. Engaging with new suppliers from regions such as Ukraine, Romania, Egypt, and Ethiopia can significantly enhance price stability and reduce dependency on a limited number of sources. This strategic approach can mitigate risks associated with geopolitical tensions, trade barriers, or supply chain disruptions that often impact wheat availability. Furthermore, forming long-term trade agreements or partnerships with these new suppliers can foster better negotiations on pricing and delivery terms, leading to improved food security in Afghanistan. Establishing relationships with multiple suppliers will provide more competitive pricing and allow the country to respond more flexibly to global market fluctuations, ultimately benefiting the millions of Afghans facing food insecurity.

Sources: Agro Investor, Agri, Hellenic Shipping News, Interfax, Rosng, Agroconf