Low Canada’s lentil crop drives domestic and export prices

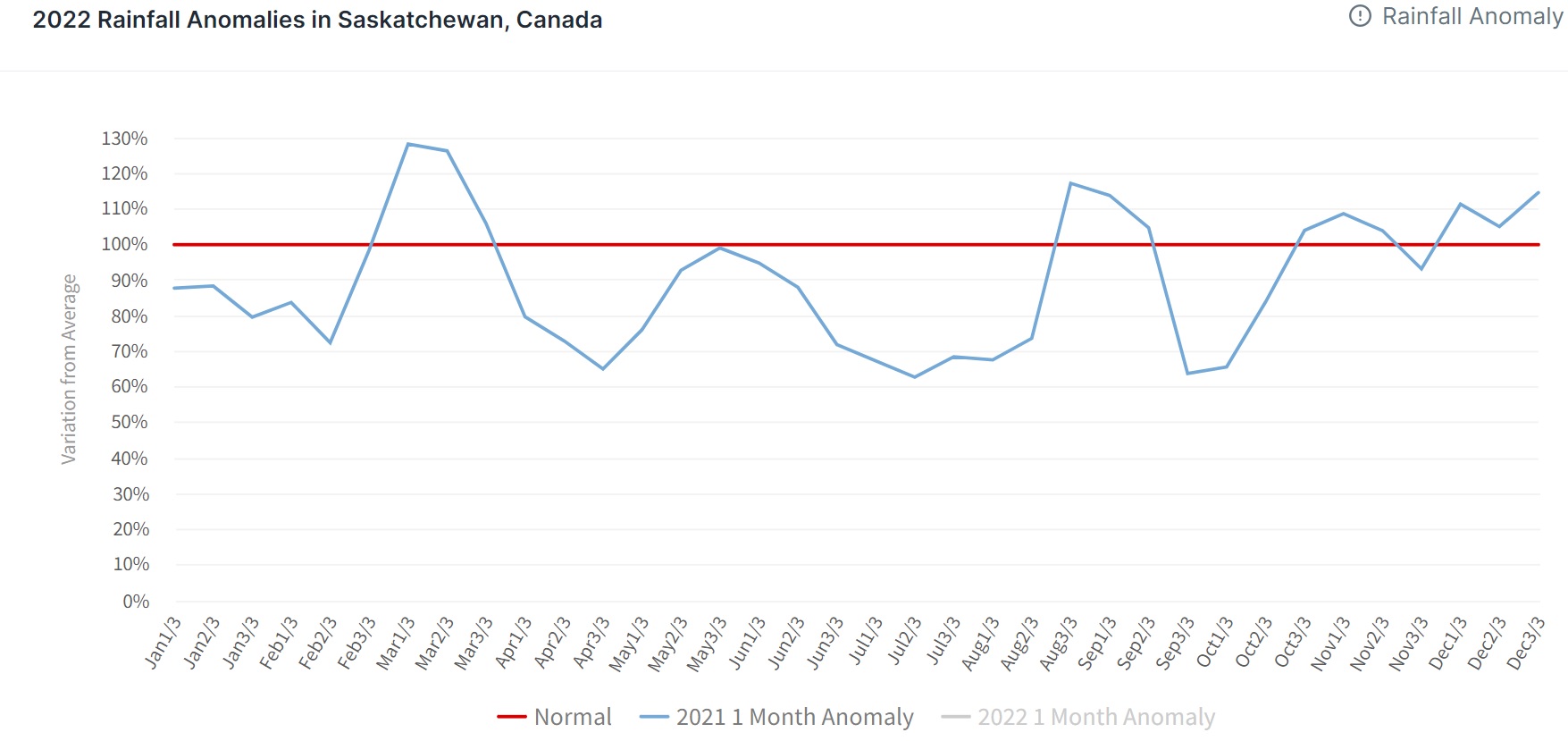

The new 2021/22 season did not begin with the most optimistic note for Canadian lentils. Unfavorable weather conditions during last year’s spring and summer in Saskatchewan, the central producing province of pulses, had capped lentil output. Extreme dryness in the mentioned region during sowing in early May and during maturing in June-July limited the lentils yields. According to the chart below, Saskatchewan’s precipitation levels from end-June through August 2021 were 30-40% below average. Canada’s Agricultural Department started to downgrade its crop estimates as the heat progressed.

Source: Tridge

Canada’s lentil output in MY2021/22 totaled 1.61 million mt, down by 1.26 million mt or 37% compared to 2020. Red lentil output fell to 1.2 million mt, almost 1 million mt less YoY. Green lentil harvest reached only 0.25 million mt, 35% less YoY. However, high carry-over stocks mitigated production losses by 2%, bringing Canada’s 2021/22 supplies to 2.06 million mt.

Tight supplies triggered price growth

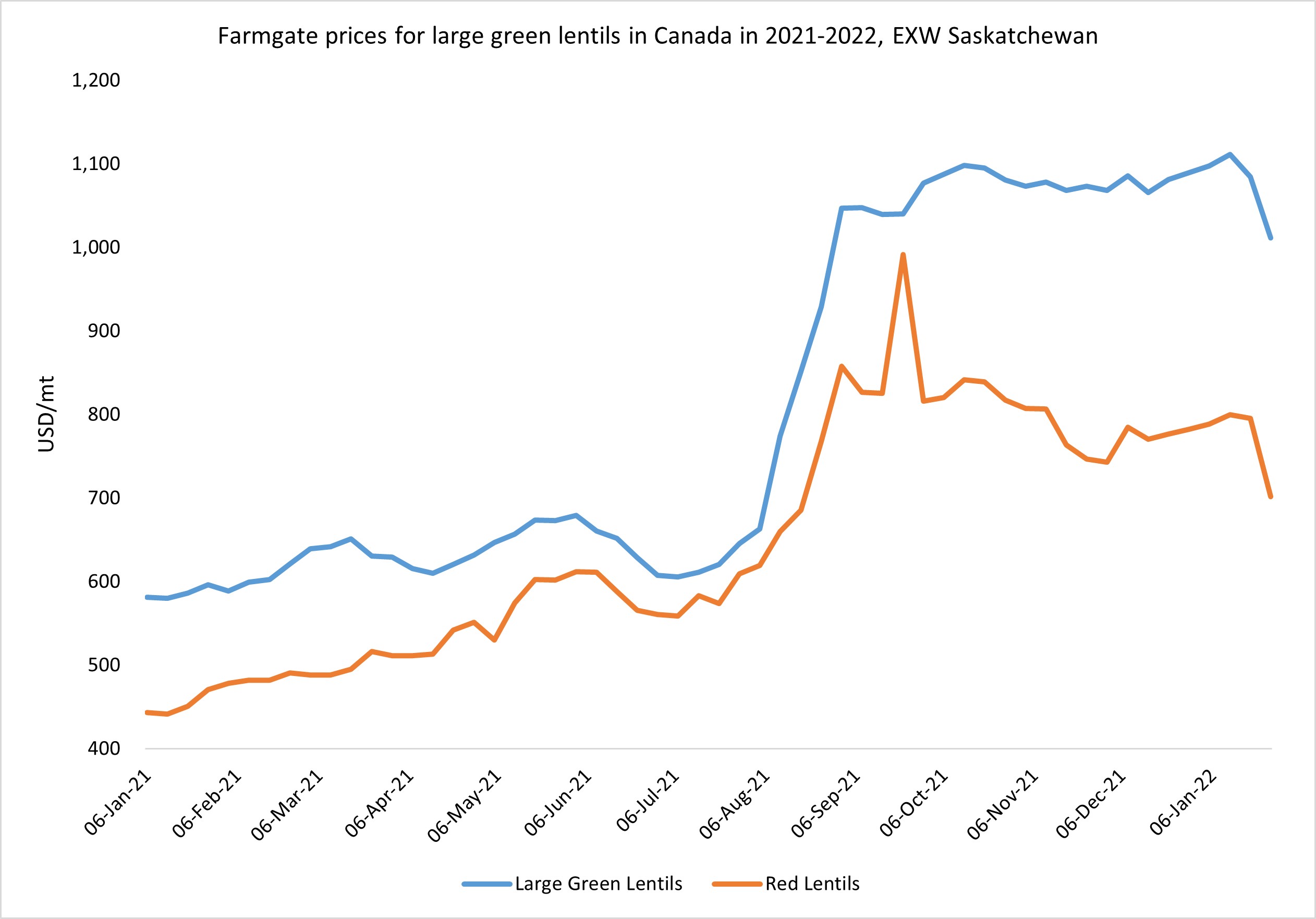

Tight lentil supply caused Canadian domestic and export prices to soar from August 2021 through mid-January 2022. The most significant jump was seen at the beginning of the new MY2021/22. Green lentil values surged by 63% from August to September 2021 to USD 1,050/mt, while red lentil value increased by 39% to USD 858/mt. Amid limited commodity amounts, traders and exporters were rushing to secure sufficient volumes to meet foreign trade contract obligations. At the same time, the green lentil premium over red lentil widened from USD 150 to USD 300/mt, given a disastrously small output of the former.

Source:AGR Market Trends - Government of Saskatchewan

After peaks at the beginning of October 2021, prices for both pulse varieties decreased somewhat in November 2021 amid weaker export demand. Major buyers of Canadian lentils were refraining from buying at the overpriced commodity, hoping that a lack of purchasing interest would help stop the upward trend.

Another phase of the price decrease happened in the second half of January 2022. In addition to slow export demand, the market received bearish news from the recent crop estimates for the MY2022/23. Agriculture Canada's first forecast for the new season’s crop was 2.5 million mt, up 0.9 million mt from the current season. The rise was attributed to higher yields and crop area estimates.

While it is still quite far to the new season and various changes might occur on the way, the current bullish factor connected with tight supplies has not lost its power to raise prices. Additional support should come from the resumption of import demand from Asian buyers ahead of Ramadan.