Trade Regulation & Geopolitics: How 2025 Trade Policy Shifts Reconfigured Global Agricultural Markets

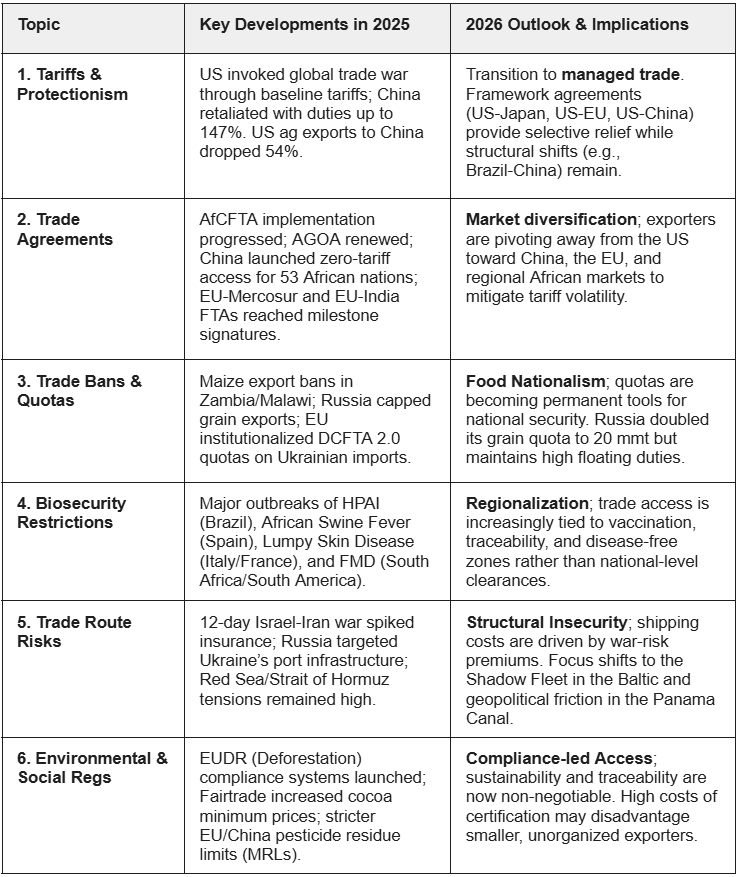

Table 1. Summary Table of Trade Regulations and Geopolitics

Introduction

In 2025, the global agri-food sector faced unprecedented disruption as a wave of protectionism, trade disputes, and regulatory shifts reshaped markets. Aggressive United States (US) tariffs, retaliatory measures by major partners, and emerging trade agreements, from Africa Continental Free Trade Area (AfCFTA) and Africa Growth and Opportunity Act (AGOA) to European Union (EU)–Mercosur and EU–India Free Trade Agreements (FTAs)—triggered volatility across supply chains, prices, and market access. Simultaneously, export bans, quota restrictions, and biosecurity crises compounded trade uncertainty, while sustainability and environmental regulations increasingly influenced market entry and compliance costs. As 2026 unfolds, the landscape is transitioning from the reactive crisis management of 2025 to strategic, managed trade, where market diversification, non-tariff compliance, and ethical standards are becoming critical determinants of competitiveness and growth in global agricultural commerce.

1. Tariffs

In 2025, the global agri-food sector was disrupted by an aggressive return to protectionism, primarily driven by the trade policies of the US. These measures implemented by the US, often utilizing the International Emergency Economic Powers Act (IEEPA), triggered a rapid cycle of retaliation from major trading partners. While the first half of 2025 was marked by extreme volatility and the near-collapse of established supply chains, 2026 has transitioned into a period of managed trade. This shift is defined by new framework agreements that offer selective relief for agricultural goods while maintaining high baseline barriers for industrial and strategic products.

1.1 Timeline of US Tariff Implementation (2025)

- January 20, 2025: The US invokes IEEPA to declare a national emergency concerning trade deficits and border security, laying the legal groundwork for broad tariff authority.

- February 1, 2025: An executive order establishes a 10% baseline tariff on imports from China and threatens 25% universal tariffs on Canada and Mexico.

- March 4, 2025: The 25% tariffs on most Canadian and Mexican imports take effect. Simultaneously, the supplemental duty on China is increased to 20%.

- April 2, 2025: The US announces global reciprocal tariffs ranging from 10% to 41%, targeting nations based on bilateral trade imbalances.

- April 9, 2025: Following a breakdown in negotiations, US supplemental tariffs on Chinese goods are increased to 125%, effectively halting trade in major bulk commodities.

- September 4, 2025: The administration shifts toward de-escalation by signing a framework agreement with Japan, signaling a new strategy of using tariffs as leverage for bilateral concessions.

- November 13, 2025: A significant modification to the reciprocal tariff list takes effect, exempting over 230 agricultural categories, including coffee, tea, cocoa, and tropical fruits, to combat domestic food inflation.

1.2 Retaliatory Measures and Economic Impact

Global trading partners, including China, Canada and Mexico, responded with surgical strikes on US agricultural exports to maximize political pressure. China implemented some of the most severe measures, increasing tariffs by 10% to 15% on over 100 products in the spring of 2025, and later matching the US escalation with a total weighted average tariff of roughly 147.6%. This had a devastating impact on the US agricultural industry. For context, in 2024, China imported USD 24.4 billion in US agricultural products, nearly 14% of total U.S. agricultural exports, making it the US’s largest agricultural trade partner outside North America. However, from Jan-25 to Aug-25, US agricultural exports to China fell by 54% compared to the same period in 2024, amounting to a USD 7.4 billion year-over-year (YoY) loss. US soybean exports fell by USD 2.7 billion compared to the same period in 2024, a 53% decline that alone accounted for over one-third of the total drop in trade value. This forced Chinese buyers to pivot to South American suppliers, primarily Brazil and Argentina, which could structurally alter future soybean trade flows.

Canada and Mexico also levied significant duties to protect their domestic markets and exert political leverage. Canada imposed a 25% surtax on approximately USD 21.5 billion (CAD 30 billion) of US imports effective March 4, 2025. This list specifically targeted high-visibility agricultural and consumer goods, including chocolate, confectionery, and coffee, alongside industrial products like steel and aluminum. Mexico, a critical USD 30.2 billion market for US agriculture, responded with similar duties on apples, dairy, and pork, sectors where the U.S. holds a dominant market share.

1.3. Remedial Frameworks and Agreements

To prevent a total severance of trade ties, a series of bilateral agreements were reached in late 2025. A landmark deal with the EU in Jul-25 saw the US cap tariffs at 15% for most EU exports. In return, the EU provided preferential market access for US tree nuts, dairy, and pork, while committing to purchase USD 750 billion in US energy by 2028. Similarly, the US–United Kingdom (UK) Economic Prosperity Deal removed a 20% tariff on US beef. In Southeast Asia, agreements with Thailand and Malaysia committed those nations to eliminate tariffs on practically all US agricultural goods, providing a vital alternative for exporters shut out of the Chinese market.

The US also reached several remedial agreements with Mexico and Canada for agricultural goods. However, several significant protectionist measures are still in place leaving a situation of managed trade entering 2026. Furthermore, Following a bilateral meeting in Busan, South Korea, on October 30, 2025, between President Donald Trump and President Xi Jinping, the US and China announced an agreement intended to ease escalating economic and geopolitical tensions between the two countries. Most notably for the US agricultural section China would suspend all retaliatory tariffs imposed on the US since Mar-25, including duties on soybeans, pork, dairy products, and grains.

1.4 EU Tariffs on Russia and Belarus

While the US trade war focused on reciprocity, the EU moved to further isolate Russia and Belarus. Effective July 1, 2025, via Regulation (EU) 2025/1227, the EU imposed a 50% ad valorem duty on the remaining agricultural products from Russia and Belarus that were not yet subject to extra customs duties. This impacted products such as sugar, flour, and animal feed. Most significantly, a new tariff regime for fertilizers was introduced to reduce dependence on Russian and Belarusian minerals. The duty began at 6.5% plus a levy of USD 43.40 to 48.80 (EUR 40 to 45) per metric ton (mt) for the 2025–2026 period. These levies are scheduled to rise annually, reaching a prohibitive USD 466.50 (EUR 430)/mt by 2028. These duties and levies were implemented to encourage the diversification of the EU agri-food and fertilizer industries away from Russian and Belarusian supply.

1.5 Outlook for 2026

Entering 2026, the global agri-food trade has settled into a fragmented but stable new normal. While the 2025 frameworks have mitigated the worst of the trade war, global food prices are projected to remain roughly higher due to the increased costs of inputs like fertilizer and logistics. The redirection of trade is likely structural. Brazil has solidified its position as a dominant supplier to China, while the US is increasingly looking to the Middle East and North Africa (MENA) region and Southeast Asia for growth. The focus for 2026 is shifting from raw tariff rates to non-tariff barriers, as countries use sustainability and health regulations as new tools for market protection.

2. Trade Agreements

In 2025, global trade was reshaped by key agreements and preferential market access schemes, including AfCFTA implementation, uncertainty around AGOA renewal, China’s zero-tariff access, and progress on EU–Mercosur and EU–India FTAs. While these measures created transitional volatility and uneven gains, 2026 is set for managed expansion, offering targeted market opportunities for agricultural exports amid a turbulent geopolitical landscape.

2.1. AfCFTA Implementation and Trade Implications

In 2025, AfCFTA advanced from institutional setup toward operational implementation. This shift was underscored by the Feb-25 memorandum of understanding (MoU) between the AfCFTA Secretariat and the United Nations (UN) Economic Commission for Africa (ECA), aimed at strengthening execution in key areas including market access, trade facilitation, and the development of regional industrial and agricultural value chains. In early 2026, member states and stakeholders convened in Ethiopia, where the Agri-Food Trade Action Plan was endorsed to accelerate agricultural trade integration, upgrade agri-food value chains, and improve private-sector participation under the AfCFTA framework. These developments reflect gradual but tangible progress in adoption. Intra-African trade was estimated at USD 220.2 billion in 2025, representing a 12.4% YoY increase according to Afreximbank. Nevertheless, intra-regional trade still accounts for only 15% to 18% of Africa’s total trade, significantly below levels observed in Europe and Asia, highlighting persistent constraints such as non-tariff barriers, regulatory fragmentation, infrastructure gaps, and uneven institutional capacity.

Looking ahead, AfCFTA is expected to deliver substantial structural gains as UN expects an increase in intra-African trade by up to 45% by 2045, adding approximately USD 275.7 billion in cross-border trade value, with food and agro-related products among the largest beneficiaries. By progressively eliminating tariffs on 90% of intra-African goods and reducing non-tariff barriers, AfCFTA is positioned to diversify agricultural export baskets, strengthen regional value chains, and expand value-added agri-food production. If fully implemented, these changes could gradually reshape global agricultural trade patterns by increasing Africa’s share of processed agri-food exports and reducing structural dependence on extra-regional imports.

2.2. AGOA Renewal and Strategic Implications for African Trade

AGOA has been a cornerstone for US and sub-Saharan Africa trade since 2000, granting duty and quota-free access to over 1,800 products, including nearly 90% of agricultural goods. In 2025, AGOA’s- scheduled expiry in September created significant uncertainty, threatening industries that support approximately 300,000 direct and 1.3 million indirect jobs in Africa, and 100,000 jobs in the US. In Jan-26, the US Congress renewed AGOA for a three-year period, effective through December 31, 2028, restoring preferential market access and providing short-term stability for African exporters. While the renewal mitigates immediate disruption, African economies face a strategic imperative to diversify export markets to ensure long-term resilience. Policymakers should leverage alternative frameworks, including the EU’s Economic Partnership Agreements for low-income and least-developed countries, China’s duty-free, quota-free market access, and AfCFTA. These measures would strengthen regional value chains, reduce over-reliance on the US market, and enhance Africa’s competitiveness in global agricultural and industrial exports.

2.3. China’s Zero-Tariff Access and Africa’s Trade Rebalancing Challenge

On June 12, 2025, China introduced a zero-tariff policy granting duty-free access to exports from 53 African countries, excluding Eswatini, to deepen trade ties and diversify its food import sources. The move creates new opportunities for African exporters of coffee, tea, cocoa, and fruits, with countries such as Ethiopia, Kenya, Côte d’Ivoire, and South Africa well positioned to benefit. The timing is notable, as African exporters simultaneously faced rising tariffs and policy uncertainty in the US market, increasing the likelihood of trade reorientation toward China. In early 2026, implementation moved forward as several countries began operationalising the zero-tariff framework. For instance, Kenya secured a preliminary bilateral arrangement granting zero-duty access on approximately 98.2% of its exports to China, reinforcing expectations of expanded agricultural shipments.

However, aggregate trade outcomes highlight persistent structural imbalances. According to China’s General Administration of Customs, Africa’s trade deficit with China widened by 64.5% YoY in 2025 to USD 102.01 billion, driven by a 25.8% YoY surge in Chinese exports to Africa to USD 225.03 billion, compared with a modest 5.4% YoY increase in African exports to China to USD 123.02 billion. These dynamics underscore that tariff elimination alone is insufficient to rebalance trade. Africa’s limited production capacity, weak industrial base, fragmented logistics, constrained processing infrastructure, and challenges in meeting quality and phytosanitary standards continue to restrict the export of higher-value products. To fully leverage zero-tariff access, African governments should complement trade preferences with targeted investment in value addition, logistics, standards compliance, and trade intelligence. Without such measures, the policy risks reinforcing Africa’s role as a supplier of raw materials rather than catalyzing a shift toward value-added exports. At the same time, exporters should avoid over-reliance on the Chinese market by diversifying toward the EU, the Middle East, and Southeast Asia, while aligning production with global requirements on sustainability, traceability, and certification.

2.4. EU–Mercosur Partnership and Long-Term Trade Integration Prospects

The EU–Mercosur trade agreement advanced in Sep-25, when the European Commission (EC) moved forward proposals for the signature and conclusion of the Partnership Agreement and an interim trade agreement. Progress continued in Dec-25, as the European Parliament and the Council agreed on safeguard rules, allowing the EC to temporarily suspend tariff preferences on sensitive agricultural imports from Mercosur if EU producers are harmed. On January 17, 2026, the EU–Mercosur Partnership Agreement (EMPA) and the interim Trade Agreement (iTA) were signed, paving the way for the EU’s largest-ever free trade agreement amid rising global tariff uncertainty. The agreement now awaits consent from the European Parliament and ratification by Argentina, Brazil, Paraguay, and Uruguay.

The EU-Mercosur trade deal will eliminate or progressively reduce tariffs on over 90% of goods and services, boosting EU exports of cars, wine, and cheese, while expanding access for Mercosur exports including beef, poultry, sugar, rice, honey, and soybeans. Moody’s estimates the deal could raise Mercosur’s gross domestic product (GDP) by around 0.25% and the EU’s GDP by 0.05% by 2040. Despite these gains, the agreement faces opposition from farmers and environmental groups, particularly in France, Poland, Ireland, Austria, and Hungary, over concerns about low-cost imports and deforestation risks.

2.5. EU–India FTA and Strategic Implications for Bilateral Trade

In 2025, after nearly two decades of negotiations, the EU and India accelerated discussions on a comprehensive FTA, with market access talks nearing completion by mid-year. Progress culminated on January 27, 2026, when both sides concluded a landmark FTA, one of the most ambitious trade pacts in their histories. The agreement will eliminate or reduce tariffs on approximately 96.6 % of bilateral goods trade by value, with EU tariffs cut on over 90 % of tariff lines and Indian tariffs reduced on 86 % of tariff lines, covering 96.6 % of Indian exports and 99.3 % of EU exports when phased reductions are included. The pact is expected to double EU goods exports to India by 2032, generating around USD4.73 billion (EUR 4 billion) in annual duty savings and providing access to a market of 1.45 billion consumers. For India, the agreement opens duty-free or preferential access to EU markets for textiles, leather, footwear, gems, jewellery, tea, coffee, and spices, while significantly reducing tariffs on industrial goods such as cars, machinery, and chemicals. Sensitive agricultural products, including soya, beef, sugar, rice, and dairy, were largely excluded to protect domestic producers. The agreement is expected to stimulate trade flows, deepen value chain integration, and enhance global trade diversification.

2.6. Outlook for 2026

Looking into 2026, the global agricultural trade landscape is being reshaped by the combined effect of new FTAs and preferential trade frameworks, amid the lingering impact of US tariff hikes in 2025. There is a clear shift away from reliance on the US market, as African exporters, facing higher US tariffs, pivot toward China, the EU, and regional markets under AfCFTA, AGOA, and China’s zero-tariff access. Meanwhile, the EU–Mercosur and EU–India FTAs are opening over 90% of trade to tariff reductions. However, structural constraints remain, especially as Africa’s industrial and logistical limitations, along with limited value addition, risk reinforcing its role as a raw material supplier. Overall, the realignment of trade flows appears lasting, signaling that market diversification, regional integration, and investment in value chains will define competitiveness in 2026 and beyond, as the focus shifts from raw tariffs to non-tariff barriers, standards compliance, and sustainable trade practices.

3. Trade Bans, Suspensions, Restrictions (Quotas)

In 2025, the global agri-food sector was dominated by the US tariff trade war but was also characterized by restrictive outright bans and volume-based quotas. As of early 2026, some of these measures have transitioned from temporary emergency responses to a more structural feature of national food security strategies. The following sections outline the specific restrictions currently shaping trade in three key regions.

3.1. Africa: Grain Security and Intra-Continental Friction

Across Africa, 2025 was a year of maize nationalism, as nations grappled with the dual pressures of climate volatility and high input costs. Major producers, including Malawi and Zambia, implemented or maintained export bans on maize in 2025. The Zambian government officially lifted the ban on August 15, 2025, allowing for the export of around 350,000 mt of maize, primarily to Malawi. These bans were triggered by regional supply shocks and the need to protect national strategic reserves. Nigeria also maintains its suspension on the export of several staple grains to curb triple-digit food inflation that plagued the region throughout the previous year.

The outlook for 2026 is slightly more optimistic for South Africa, which expects to export approximately 1.03 mmt of white maize and 840,000 mt of yellow maize to regional neighbors like Zimbabwe and Botswana. However, the continent remains a patchwork of restrictions. While South Africa serves as Southern Africa’s breadbasket, other nations are increasingly using seasonal bans—such as Kenya’s suspension of certain horticultural exports—to ensure that high-quality produce is processed domestically rather than exported as raw materials.

3.2. Russia: Record Harvests vs. Managed Quotas

Russia has fundamentally altered its grain export strategy for 2026 to manage its third-largest grain harvest on record of 142 mmt. In late Dec-25, the Russian government announced that the grain export quota for the period of February 15 to June 30, 2026, would be doubled to 20 mmt, up from the 10.6 mmt allowed in 2025. This expanded quota now covers wheat, meslin, barley, and corn, whereas previous restrictions were largely limited to wheat.

Despite this volume increase, the floating export duty remains a significant barrier. Shipments outside of the allocated quota are subject to a prohibitive duty of 50% of the customs value, but not less than USD 108.50 (EUR 100)/mt. Furthermore, while the government is pushing for higher volumes, the Russian Grain Union has noted that the current strength of the ruble makes exports unprofitable for smaller producers. As a result, analysts expect that a significant portion of the 2026 quota may go unused unless there is a significant currency devaluation or a further reduction in the floating duty.

3.3. The European Union: From Emergency to DCFTA 2.0

In 2026, the EU has moved away from the emergency suspensions that characterized its trade with Ukraine and Russia in 2024 and 2025. The new DCFTA 2.0 (Deep and Comprehensive Free Trade Area) framework, which became fully operational in Jan-26, has institutionalized a series of permanent quotas on sensitive agricultural products. This includes strict volume limits on Ukrainian wheat, maize, and poultry to protect farmers in Poland, Hungary, and Slovakia from market saturation.

Simultaneously, the EU has updated its Autonomous Tariff Quotas through Council Regulation 2025/2614, effective January 1, 2026. This system allows for the duty-free import of specific agri-food inputs that the EU cannot produce in sufficient quantities, such as specialized mushrooms (Auricularia polytricha) and specific vegetable oils. These quotas are highly technical and are often exhausted within the first few weeks of the year. For 2026, the EU is using these quotas as a surgical tool—opening access for raw materials needed by its food processing industry while maintaining high barriers against finished products from the US and Russia.

4. Biosecurity Restrictions

In 2025, outbreaks of avian influenza, African swine fever (ASF), Lumpy Skin Disease (LSD), and foot-and-mouth disease (FMD) disrupted global livestock trade, prompting import bans, export suspensions, and stricter biosecurity measures across key markets. Entering 2026, these disruptions are expected to influence trade patterns, with countries reinforcing surveillance, vaccination, and regionalisation protocols to safeguard supply chains, manage price volatility, and maintain competitiveness in a landscape where disease management has become a central determinant of market access.

4.1 Global Avian Influenza Outbreaks and Trade Disruptions in 2025

In 2025,outbreaks of highly pathogenic avian influenza (HPAI), prompted widespread biosecurity restrictions and trade impacts across multiple regions, significantly disrupting poultry markets globally. In Mar-25, Brazil, the world’s largest chicken exporter, confirmed its first HPAI outbreak on a commercial farm in Rio Grande do Sul, triggering trade bans from major markets including China, the EU, South Korea, Canada, Chile, and South Africa, as well as regional restrictions in the UK, the United Arab Emirates (UAE), Japan, and others. Despite that, some countries later lifted restrictions when outbreaks were resolved, like the UK lifted HPAI‑related import bans in Jul-25. In Argentina, temporary suspensions on exports of fresh poultry and meat products due to an HPAI outbreak in Aug-25 were also lifted by Nov-25 once control criteria were met. Across Europe in 2025, over 699 HPAI outbreaks were recorded in poultry farms across 23 countries, underscoring persistent disease pressure and prompting emergency zoning and import control decisions to manage trade risk. In early 2026, bird flu events continued, with outbreaks in regions such as West Flanders, Belgium, where millions of birds were culled to contain spread, reinforcing ongoing trade and biosecurity challenges.

4.2. African Swine Fever and Global Pork Trade Disruptions

A notable ASF event occurred in late 2025 when it was detected in wild boars in Catalonia, Spain. This triggered trade bans and suspensions from key markets such as China, the UK, Taiwan, Mexico, Japan, and South Korea on pork products originating from the outbreak area, disrupting trade flows for an industry valued at about USD 10.37 billion (EUR 8.8 billion) annually. As the EU’s largest pork producer, Spain faced the blocking of nearly one‑third of its export certificates, particularly impacting shipments to China. To mitigate disruption, regionalisation measures were applied, allowing pork from unaffected areas to continue trading under strict biosecurity protocols. These restrictions caused global pork supply imbalances and price volatility, as importers turned to alternative sources outside affected zones, underscoring the wider economic and trade implications of livestock disease outbreaks on agri-food supply chains and export competitiveness.

4.3. Lumpy Skin Disease and Global Cattle Trade Disruptions

A major LSD event occurred in mid-2025 in Italy and France, followed by cases in Spain in Oct-25. This triggered trade bans and suspensions from key markets on live cattle, embryos, semen, dairy, and bovine by-products, affecting exports from the outbreak areas and disrupting trade flows for an industry valued at approximately USD 45 billion annually across Europe. As major cattle producers, Italy, France, and Spain faced restrictions that blocked significant portions of their exports, particularly to Asian markets including China, South Korea, and Taiwan. To mitigate trade disruption, regionalisation measures were applied, allowing products from unaffected zones to continue trading under strict biosecurity and surveillance protocols. In South Korea, authorities reinforced biosecurity measures, including tighter import controls on live cattle and genetic materials, and strengthened vaccination and vector control programmes to prevent domestic outbreaks. These restrictions led to shifts in global beef and cattle product flows and increased regulatory complexity at borders. They also heightened the focus on surveillance and vaccination programmes, highlighting the broader economic impacts of livestock disease on agri-food supply chains and export competitiveness in 2025/26.

4.4. Foot Mouth Disease Outbreaks and Global Trade Impacts

In early 2025, FMD outbreaks in South America, particularly in Peru and Ecuador, prompted key importers, including the EU, South Korea, Japan, and China, to restrict imports of susceptible animals and products in line with the World Organisation for Animal Health (WOAH) standards. Most of these restrictions remained in place through late 2025, with phased lifting tied to verified disease control and surveillance. South Africa became a major focal point after an FMD outbreak on a commercial farm in the Free State in Jul-25, with around 270 confirmed outbreaks reported across multiple provinces by mid-year. The situation escalated in early 2026, particularly in Gauteng, where 195 laboratory-confirmed outbreaks affected approximately 261,000 animals as of January 23, 2026. In East Africa, especially Kenya, mid-2025 FMD cases led to temporary export bans and tighter border checks. By early 2026, some Asian importers kept strict veterinary certification rules. These measures slowed livestock trade even without formal bans.

4.5. Outlook for 2026

Looking into 2026, global livestock and poultry trade continues to face significant biosecurity pressures from Avian Influenza, ASF, LSD, and FMD, leading to import restrictions, culling campaigns, and regional disease zoning. These measures are expected to sustain supply imbalances, disrupt trade flows, and increase regulatory complexity, particularly for poultry, pork, and beef exports to major markets. Countries are advised to strengthen surveillance, vaccination, and traceability systems, implement disease-free compartments, and diversify export destinations to reduce vulnerability. Authorities should also remain vigilant for emerging threats such as Bovine Spongiform Encephalopathy (BSE), which could trigger additional trade suspensions, while aligning with WOAH standards to protect agri-food supply chains and maintain global market access.

5. Trade Route Risks

In 2025, the logistical arteries of global agri-food trade were stressed by a combination of rapid military escalations and the lingering effects of the maritime security crisis in the Red Sea. As we enter 2026, the risk profile has shifted from acute kinetic disruptions toward a more persistent structural insecurity, where the threat of chokepoint closures and regulatory clamped-downs has become a permanent factor in shipping insurance and supply chain planning.

5.1. The Israel-Iran 12-Day War (June 2025)

The most significant logistical disruption of 2025 was the 12-day direct conflict between Israel and Iran, which sent shockwaves through the Middle East’s transit zones. While physical damage to agricultural infrastructure was localized, the maritime impact was global. During the peak of the conflict, the Strait of Hormuz experienced extreme GPS and AIS (Automatic Identification System) signal jamming, making safe navigation nearly impossible without military escorts.

The conflict triggered an immediate surge in war-risk insurance premiums, adding USD 10.00 per barrel to fuel costs, which directly translated into higher freight rates for bulk agricultural carriers. Furthermore, the temporary closure of Israel's Haifa port forced a redirection of perishable cargo, creating a 14-day backlog in the Eastern Mediterranean. While a ceasefire was reached on June 24, 2025, the war proved that even a brief disruption in this corridor can cause a spike in global fuel prices, which remains a primary driver of agri-food prices in 2026.

5.2. The Strait of Hormuz and Iranian Unrest (2026)

As of early 2026, the Strait of Hormuz is the world’s most volatile maritime chokepoint. Internal civil unrest in Iran has led to an increasingly assertive posture by the Iranian regime through the use of the Iranian Revolutionary Guard Corps (IRGC), which has conducted seizure attempts of foreign vessels. With the US moving toward a confrontational military posture and threatening intervention to protect freedom of navigation, the threat of a total closure of the Strait is a primary concern. The Strait is a vital passage for agri-food trade between the Americas, Europe, and the Persian Gulf. A closure would block nearly 35% of global crude oil trade and 20% of global LNG trade. Oil prices are a primary driver of food inflation while LNG is critical for the production of nitrogen-based fertilizers. Since the start of the year the OPEC basket price has risen nearly USD 9.00 per barrel while urea fertilizer prices are up nearly USD 80/mt. This suggests that a closure of the strait would be catastrophic for global trade but even tensions in the region can have significant impacts on commodity prices which can drive input costs and ultimately consumer prices for agri-food up.

5.3. The Black Sea: A War of Attrition on Infrastructure

Throughout 2025 and into early 2026, the Black Sea has transitioned from a battle over shipping lanes to a war of attrition against port infrastructure. While Ukraine’s independent maritime Humanitarian Corridor successfully moved grain throughout 2025, the geopolitical cost has escalated. Russia has intensified drone and missile strikes on the Odessa and Chornomorsk port complexes, as well as the Danube River ports of Izmail and Reni. These strikes have degraded Ukraine's harvest, logistics, and port capacity. As a result, according to State Customs Service of Ukraine data, average grain exports from Ukraine were 30% lower during the Jul-25 to Dec-25 period compared to the same period last year. Going into 2026, the risk is no longer the absence of grain export contracts, but the physical degradation of the harvest and logistics infrastructure required to move Ukraine’s grain harvest.

5.4. Outlook for 2026: Emerging Risks

The 2026 outlook is defined by a shift toward regulatory and hybrid threats in key maritime zones:

- The Baltic Sea Shadow Fleet Clampdown: In late Jan-26, a group of 14 European countries, including Germany, Poland, and the UK, issued an open warning to the Russian shadow fleet. By treating vessels with multiple flags or invalid insurance as stateless vessels, European states have expanded their authority to intervene, inspect, and detain tankers. While intended to curb Russian oil revenue, this crackdown increases the risk of tit-for-tat maritime blockades and accidental collisions in the Baltic, which is a major transit route for European agricultural inputs and Russian fertilizers.

- The Panama Canal Geopolitical Struggle: While water levels have stabilized in 2025 and into 2026, the canal has become a focus of US-China tension. New US policies are challenging Chinese influence over canal management. Any administrative friction here would immediately impact US grain exports to Asia and South American fruit exports to the US East Coast.

- The Taiwan Strait and South China Sea: A potential annexation of Taiwan by China remains the ultimate trade risk. The Taiwan Strait handles over USD 2.45 trillion in annual shipping, around one fifth of global maritime trade. A blockade would cripple regional supply chains, while cutting off China’s massive exports of phosphates and urea, potentially causing a global fertilizer crisis. The value of Chinese trade alone through the Taiwan Strait is around USD 1.4 trillion annually.

6. Environmental and Social Regulations

In 2025, the global agri-food sector faced an increasingly complex regulatory landscape, driven by sustainability, ethical certification requirements, stricter pesticide and environmental standards. In 2026, these measures are expected to shift from emerging compliance challenges to permanent trade considerations, shaping market access, investment in traceability systems, and competitive dynamics across major agricultural commodities.

6.1. Fair Trade Certification Trends and Global Market Access

In 2025, Fair Trade frameworks continued to evolve in response to market pressures, costs, and sustainability demands, shaping global trade in ethical agricultural products. Fairtrade Africa marked 20 years in 2025, launching a three-year strategy (2026–2028) to strengthen smallholder support through projects and community infrastructure. In cocoa, Fairtrade International announced increases in cocoa prices and premiums to support smallholder farmers. The Minimum Price will rise to USD 3,500/mt in Ghana and EUR 3,200/mt in Côte d’Ivoire, effective October 1, 2026. Alongside this, the Fairtrade Premium will increase to USD 275/mt and EUR 250/mt in Côte d’Ivoire, payable from October 1, 2026 in Ghana and Côte d’Ivoire, and from June 11, 2026 in other countries. Similarly, the Organic Differential will rise to USD 450/mt in Ghana and EUR 410/mt in Côte d’Ivoire, following the same schedule, ensuring that cocoa producers benefit from both guaranteed prices and additional premiums for sustainable production. Meanwhile, some countries raised concerns over certification costs. For instance, the Kenyan government suspended Rainforest Alliance certification for tea in Jun-25 due to high smallholder costs. Despite that, Fair Trade actors are aligning traceability and compliance systems with frameworks such as the EU deforestation and due-diligence regulations to maintain market access while supporting sustainable, ethical supply chains.

6.2. Global Pesticide Regulations: Trade Implications and Compliance

Regulatory action on pesticides and herbicides intensified globally in 2025, reshaping agricultural trade through stricter residue limits, bans on hazardous chemicals, and enhanced compliance requirements. In the EU, regulators updated maximum residue levels (MRLs) for multiple pesticides, including chlorpropham, fuberidazole, and others, under Regulation (EU) 2025/1163, effective from June 16, 2025, requiring exporters to meet tighter standards or risk shipment rejection. Additionally, a coordinated multi‑year control programme (EU Regulation 2025/854) came into force on January 1, 2026, to ensure compliance with pesticide residue limits and assess consumer exposure through 2028, raising enforcement expectations for global suppliers. In Kenya, the government banned 77 highly hazardous pesticides and restricted 202 others in mid-2025 after a scientific review cited unacceptable health and environmental risks, with another 151 products under review through Dec-25, effectively limiting their use and import until compliance is verified. China also strengthened pesticide labeling requirements in Aug-25, mandating full traceability on product formulations and registration details, taking effect January 1, 2026. These regulatory changes are influencing trade patterns by increasing non‑tariff barriers , especially in high‑value markets like the EU and China, with exporters facing greater costs for residue testing, certification, and compliance.

6.3. EU Environmental Requirements and Market Impact

In 2025, the EU expanded and adjusted its environmental regulatory framework, especially the European Union Deforestation Regulation (EUDR), with significant implications for global agricultural and commodity trade. Originally adopted in 2023 and set to require proof that products like cattle, cocoa, coffee, palm oil, rubber, soy, and wood placed on the EU market are deforestation‑free, the EUDR’s application was delayed to December 30, 2026 for large and medium operators and June 30, 2027 for micro and small enterprises after Parliament and Council agreed simplification measures to ease compliance burdens. To prepare for compliance, the EU launched an Information System in late 2024 that continued to be rolled out in 2025, enabling operators to submit due‑diligence statements proving that products meet environmental criteria. Stakeholders globally, including major commodity exporters in Latin America, Africa, and Asia, have raised concerns that meeting traceability and documentation requirements will increase non‑tariff barriers and compliance costs, potentially constraining exports to the EU and shifting trade toward certified sustainable suppliers. The enhanced EU requirements are reshaping trade patterns by driving investment in traceability and compliance systems. At the same time, they are causing market adjustments and raising concerns about competitive disadvantages for exporters unable to meet stringent environmental standards, highlighting the increasing role of environmental regulation in shaping agricultural trade.

6.4. Outlook for 2026

Looking into 2026, the global agricultural trade landscape is expected to continue shifting toward sustainability, traceability, and ethical compliance, driven by Fair Trade certification trends, stricter pesticide regulations, and EUDR requirements. Fair Trade price increase regulations are likely to strengthen smallholder resilience but may increase production costs for exporters, emphasizing the need for efficient supply chain management. Simultaneously, tighter pesticide residue limits and bans in the EU, China, and Kenya, coupled with expanded environmental regulations such as the EUDR, will continue to raise non-tariff barriers, forcing exporters to invest in traceability, testing, and documentation systems. Countries aiming to maintain market access in high-value markets should prioritize compliance infrastructure, integrate sustainability practices, and diversify export destinations to mitigate competitive disadvantages, while leveraging these trends to capture premiums for certified and ethically produced commodities.

Conclusion

The developments witnessed in 2025 and those unfolding in 2026 signal a decisive structural shift in global agri-food trade away from liberalized, price-driven flows toward a fragmented system governed by managed trade, strategic alliances, and compliance-led market access. Tariffs, quotas, biosecurity measures, environmental regulations, and geopolitical risks are no longer episodic shocks but embedded features of the trading landscape. While new FTAs and preferential schemes are opening selective opportunities, these gains are increasingly conditional on traceability, sustainability, disease control, and logistical resilience. For exporters and policymakers, competitiveness in 2026 and beyond will hinge less on tariff arbitrage and more on diversification, value addition, compliance capacity, and supply-chain adaptability. Those able to align production with evolving regulatory standards, invest in resilient trade routes, and pivot toward regional and emerging markets will be best positioned to navigate and benefit from the new era of structurally constrained global agricultural trade.