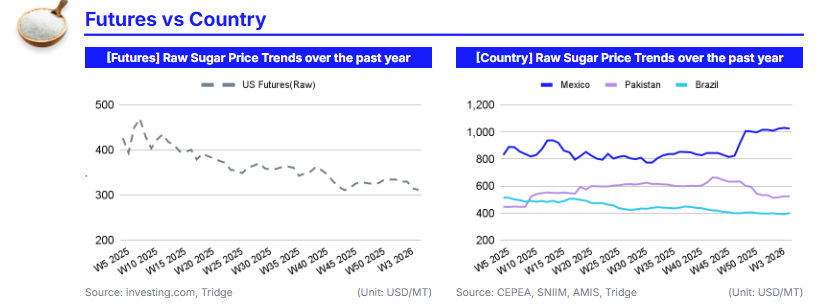

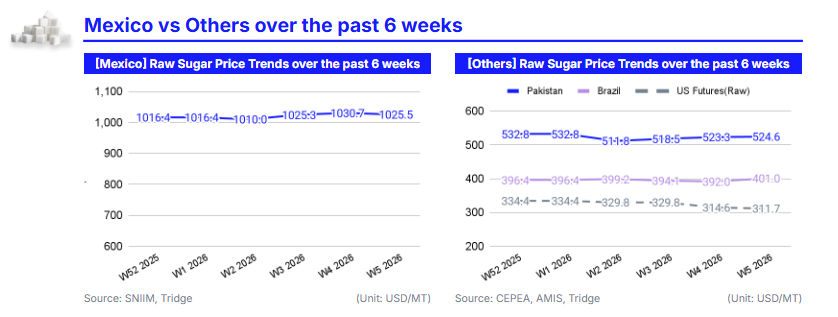

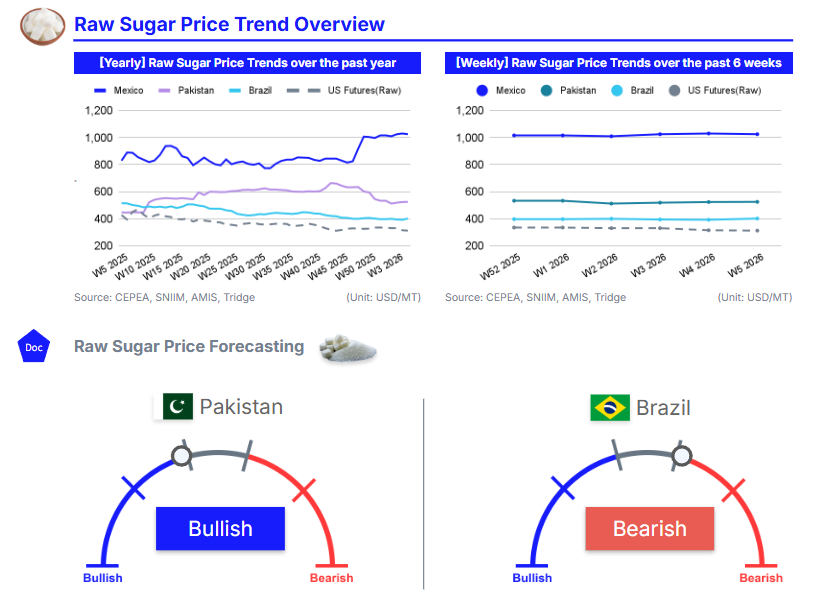

In W5 2026, global sugar markets reflected short-term divergence but remained structurally oversupplied. Brazil’s prices rose 2.29% WoW to USD 401/mt, supported by localized demand, yet strong 2025/26 Center-South output of 40.222 mmt and a higher sugar mix of 50.82% continue to reinforce ample export availability. In Mexico, prices declined 0.50% WoW to USD 1,025.5/mt despite a 156% import tariff, as elevated inventories and normalized export flows cushioned the market. Pakistan’s prices edged up 0.25% WoW to USD 524.6/mt amid procurement delays, though improving crushing activity suggests easing tightness. US raw sugar futures fell 0.91% WoW to USD 311.7/mt, reflecting persistent global surplus expectations anchored by Brazil’s supply strength.

For a global food manufacturer sourcing Brazilian raw and refined sugar, the core strategy is defensive, short-term procurement anchored in Brazil while maintaining flexibility across secondary origins. Brazil should remain the primary sourcing base through staggered and short-duration contracts to capitalize on surplus-driven price compression. Exposure to Mexico should be tactical due to elevated absolute prices and policy distortions, while Pakistan should be approached cautiously given localized supply uncertainty. This cost-focused and flexible sourcing model preserves margin protection while allowing responsiveness to episodic volatility in a range-bound global sugar market.

1. Weekly Price Overview

Brazil’s Output Strength Caps Global Sugar Upside Despite Localized Volatility Across Key Origins

In W5 2026, global sugar prices showed mixed movements across key origins, with short-term gains in Brazil offset by continued pressure from abundant global supply. Brazil’s sugar prices increased by 2.29% week-on-week (WoW) to USD 401 per metric ton (mt), reflecting technical stabilization and localized demand, but broader fundamentals remain bearish. According to the Brazilian Sugarcane Industry Association (UNICA), cumulative 2025/26 Center-South sugar output through Dec-25 reached 40.222 million metric tons (mmt), up 0.9% year-on-year (YoY), while the share of cane allocated to sugar rose to 50.82% from 48.16% in the previous season. This higher sugar mix, combined with steady production, reinforces ample export availability and continues to weigh on international benchmarks despite the recent weekly rebound.

In Mexico, sugar prices declined 0.50% WoW to USD 1,025.5/mt, even after the government implemented a 156% tariff on all sugar imports, including cane, beet, syrups, and refined liquid sugar. The measure, formalized through a presidential decree and published in the Official Gazette, aims to protect domestic producers following a surge in lower-priced imports in recent years. While the tariff is expected to tighten domestic supply conditions structurally, the immediate price response suggests that current inventories and normalized export flows are providing a short-term market cushion.

Pakistan’s sugar prices rose 0.25% WoW to USD 524.6/mt amid mounting tensions between farmers and mills. The Sindh Chamber of Agriculture reported that only around 25% of cane has been harvested due to delayed procurement by mills, with calls to raise the cane purchase price to USD 2.15 per 40 kilograms (PKR 600/40 kg). Slower crushing and procurement bottlenecks risk reducing sucrose content and disrupting planting cycles, introducing localized supply uncertainty that has provided mild price support.

In the United States (US), raw sugar futures fell 0.91% WoW to USD 311.7/mt, reflecting persistent global surplus expectations. Although severe cold weather in parts of the southern US has raised concerns about potential crop stress for future planting cycles, current market sentiment remains anchored by strong Brazilian output and comfortable global supply projections. While weather and policy developments have created localized volatility, the dominant driver over the past two weeks has been confirmation of resilient production and elevated sugar allocation in Brazil, limiting sustained upward price momentum.

2. Price Analysis

Global Sugar Market Remains Oversupplied as Brazil’s Export Strength and Rising Output in Mexico and Pakistan Limit Price Recovery

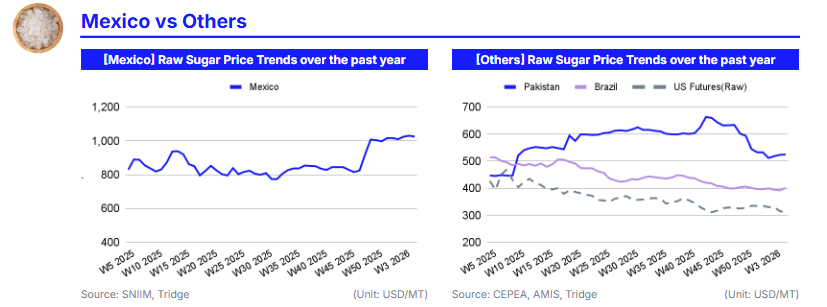

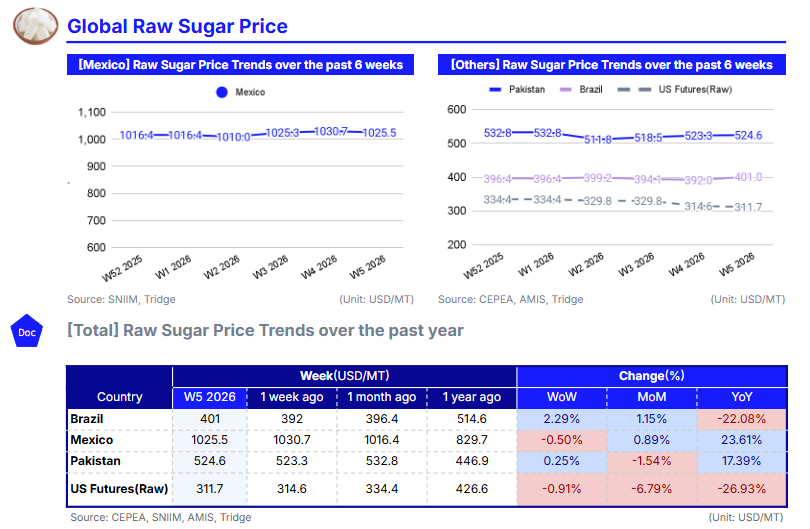

Recent sugar price movements confirm that the market remains structurally oversupplied, with short-term fluctuations driven by localized adjustments rather than tightening fundamentals. In Brazil, prices increased 1.15% month-on-month (MoM) to USD 401/mt but remain 22.08% lower year-on-year (YoY) from USD 514.6/mt. The modest monthly rebound reflects technical stabilization after an extended correction, yet the steep annual decline signals that improved production, high sugar allocation, and uninterrupted export flows continue to outweigh demand growth. Given that sugar represents 12% of Brazil’s USD 116.5 billion agricultural export basket, within a highly concentrated commodity structure dominated by soybeans and coffee, the country’s scale and logistical depth reinforce its ability to sustain large export volumes. This structural export capacity limits the likelihood of prolonged price rallies, as global buyers rely on Brazil as a volume anchor.

In Mexico, prices rose 0.89% MoM but remain under pressure structurally despite being 23.61% higher YoY. A projected 7% increase in 2025/26 production to 5.4 million tons, combined with a 56% reduction in US export quotas and rising high-fructose corn syrup imports (+4% YoY), has created domestic saturation. Inventories are projected at 1.07 mmt, around 10% above optimal levels, equivalent to roughly 2.5 months of consumption. The slight monthly increase is likely due to short-term distribution or policy distortions rather than a tightening of supply. The underlying balance suggests continued vulnerability to downside correction as excess stocks weigh on the internal market.

Pakistan’s prices declined 1.54% MoM but remain 17.39% higher YoY, indicating that expanded crushing activity is gradually easing prior to tightness. Output in Punjab has increased versus last season, supported by uninterrupted mill operations and improved farmer payments. The monthly decline reflects improving physical availability and active anti-hoarding enforcement, suggesting that last year’s elevated price environment is normalizing as supply stabilizes.

US raw sugar futures fell 6.79% MoM and 26.93% YoY to USD 334.4/mt. While winter storms temporarily strengthened spot Midwest beet sugar prices and lifted short-term demand, forward buying remains cautious, and global benchmark prices continue to respond primarily to Brazil’s export strength and comfortable global stocks. Weather-related demand spikes have not translated into sustained futures support, reinforcing the broader bearish trend.

Sugar prices are expected to remain range-bound with a downward bias. Brazil’s scale-driven export model and concentrated commodity structure provide strong supply continuity, Mexico faces persistent domestic oversupply risks, and Pakistan’s improving production tempers upside momentum. Absent a significant weather disruption in major producing regions or abrupt policy intervention restricting exports, sustained price recovery appears unlikely in the near term.

3. Strategic Recommendations

Global Sugar Trade Strategies Favor Brazilian Sourcing and Short-Term Contracts as Structural Surplus Caps Price Upside

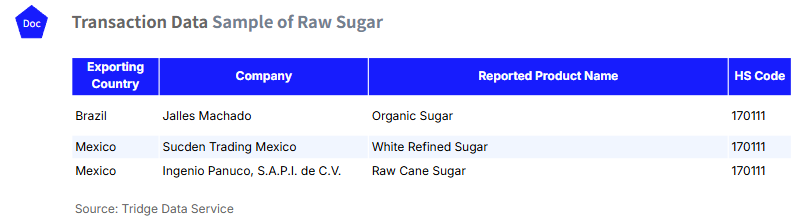

Given the structurally oversupplied global balance and the bearish-to-neutral outlook, sugar trade strategies should remain cost-focused, short-term oriented, and opportunistic. Brazil continues to anchor global supply, with prices at USD 401/mt and sustained output supported by a higher sugar mix. Buyers should prioritize Brazilian origin as the primary sourcing base, securing staggered short-term contracts rather than locking in long-dated volumes. Competitive offerings such as organic sugar from Jalles Machado, as reflected in Tridge’s Eye transaction data explorer, can be leveraged to secure cost-efficient coverage while maintaining flexibility to benefit from potential further downside.

In Mexico, where domestic prices remain elevated at USD 1,025.5/mt despite recent softness and rising inventories, sellers should accelerate offtake while price levels persist. According to Tridge’s Eye transaction data explorer, active flows of white refined sugar through Sucden Trading Mexico and raw cane sugar from Ingenio Panuco, S.A.P.I. de C.V. indicate ongoing commercial activity that can be monetized under current price conditions. Export-oriented traders should prioritize near-term sales execution and avoid excessive stock accumulation. Buyers, in contrast, should limit forward exposure and rely on spot procurement, anticipating gradual normalization as production expands and inventories remain above optimal levels.

In Pakistan, where mild weekly gains contrast with improving crushing activity, exporters should remain cautious in committing forward volumes until procurement bottlenecks and policy signals become clearer. Buyers may defer large commitments and monitor harvesting progress for more favorable entry points if supply accelerates.

The recommended action plan is to anchor procurement in competitively priced Brazilian supply through short-duration contracts, monetize relatively elevated prices in Mexico via accelerated sales supported by transaction visibility from Tridge’s Eye, and maintain optionality in Pakistan pending clearer supply signals. Selective short-term hedging in US futures can be used to manage episodic volatility, but overall positioning should remain defensive, preserving liquidity and flexibility in a market where structural surplus continues to cap sustained price upside.