In W50, although some EU markets recorded marginal WoW gains like Germany, Belgium, and the Netherlands, butter prices remained lower on a monthly and annual basis. Similarly, US prices fell, supported by rising output and robust exports. The GDT auction reinforced bearish sentiment, with overall dairy prices and butter values declining further despite strong demand from North Asian buyers. Oceania also faced ongoing price softness due to sustained milk availability and heightened global competition. Looking ahead, while near-term pressure is expected to persist, particularly in the US, a potential rebalancing of milk toward cheese production in the EU could support a gradual recovery in butter prices from 2026. In the meantime, market participants are recommended to prioritize value-added processing, and targeted export strategies. They should also consider stronger inventory and price-risk management to navigate the prolonged period of low prices.

1. Weekly Price Overview

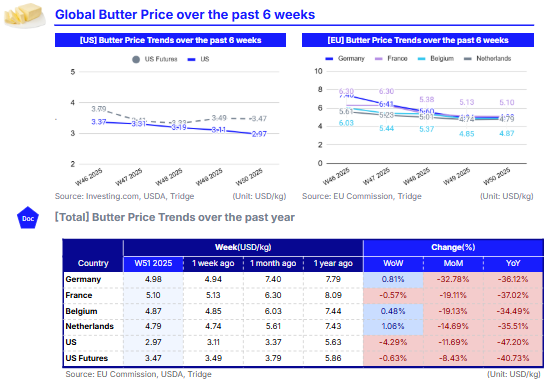

Global Butter Markets Weaken as Ample Supply and High Inventories Persist

In W50, butter prices in Germany averaged USD 4.98 per kilogram (kg), up 0.81% week-on-week (WoW), largely supported by currency movements. However, values were still down by 32.78% month-on-month (MoM) and 36.12% year-on-year (YoY). It is worth noting that butter prices in Germany fell below the USD 5.00/kg threshold in W49 for the first time in over two years. A similar trend was observed in Belgium, where butter prices averaged USD 4.87/kg, edging up 0.48% WoW but remaining lower by 19.13% MoM and 34.49% YoY. In the Netherlands, prices stood at USD 4.79/kg, reflecting a 1.06% WoW increase, but were down 14.69% MoM and 35.51% YoY. In contrast, French butter prices averaged USD 5.10/kg, declining by 0.57% WoW and registering drops of 19.11% MoM and 36.12% YoY.

Overall, EU butter prices remained under pressure as abundant milk supplies and high inventory levels continued to weigh on the market. Buyers largely limited purchases to immediate needs, showing little interest in extending coverage amid comfortable supply conditions.

In the United States (US), butter prices continued to weaken in W50, averaging USD 2.97/kg, down 4.29% WoW, 11.69% MoM, and 47.20% YoY. Butter futures followed a similar downward trajectory, declining by 0.63% WoW, 8.43% MoM, and 40.73% YoY to USD 3.47/kg. Persistently high production levels remained the primary factor weighing on prices. While retail discounting may provide limited short-term support, the completion of holiday demand and sustained strong cream output suggest that US butter prices are likely to face further downward pressure in the near term.

2. Price Analysis

Ample Milk Supply Pressures Butter Prices Across Key Producing Regions

At the Global Dairy Trade (GDT) auction held on December 16, overall dairy prices declined by 4.4% from the previous event to USD 3,341 per metric ton (mt). Specifically, butter prices weakened, falling by 2.5% to USD 5,012/mt. Demand was led by North Asian buyers, who accounted for nearly 70% of total butter purchases, followed by buyers from Europe and Southeast Asia/Oceania.

In Oceania, butter prices extended their downward trend over the week. Although the region has moved past the peak of the spring flush, sustained strength in milk production has ensured ample milk availability for processors. Domestic market conditions were mixed during the period, with processor prices softening slightly, while domestic futures prices remained steady or edged higher. On the export front, prices declined amid strong global milk production and intensified competition from other major butter-producing regions.

In the US, butter production reached nearly 186 million pounds (lbs) in Oct-25, marking a 10.1% increase YoY. US butter remains the cheapest globally, supporting robust export growth. Low fat prices have prompted some producers to reduce the use of costly feed supplements aimed at boosting milkfat levels. However, with the national dairy herd close to its largest size in three decades and ongoing genetic improvements, any meaningful reduction in butterfat production is expected to be gradual.

According to estimates from the United States Department of Agriculture (USDA), EU butter production is projected to rise marginally to 2.09 million metric tons (mmt), up 0.1%, supported by strong domestic demand. Despite this, reduced competitiveness in global markets has constrained exports, contributing to lower prices. Looking ahead, EU butter production in 2026 is forecast to decline by 1.4% YoY to 2.06 mmt, as tighter milk supplies are expected to favor cheese production over butter and nonfat dry milk (NFDM). This shift could provide support for a rebound in butter prices in 2026.

3. Strategic Recommendations

Navigate Low Butter Prices Through Value Optimization and Demand Targeting

In the current environment of persistent oversupply and depressed butter prices, processors in the EU and the US should actively rebalance milk utilization away from bulk butter toward higher-value and more demand-resilient dairy products. Redirecting cream and butterfat into specialty and branded cheeses, premium spreads, ice cream, and foodservice-oriented fat blends can help absorb excess supply while improving margins. For example, EU processors can prioritize Protected Designation of Origin (PDO) and functional cheeses where pricing is less exposed to global spot volatility. On the other hand, US processors can expand customized butterfat products for industrial bakeries and foodservice clients, reducing reliance on low-priced commodity butter.

On the demand side, exporters should shift from price-led competition to targeted market development in structurally deficit regions, particularly in North Asia, Southeast Asia, and the Middle East. Given that North Asian buyers dominate GDT butter purchases, exporters can strengthen partnerships with bakery and food manufacturers by emphasizing performance attributes such as flavor consistency, lamination quality, and supply reliability rather than price alone. Exporters should consider long-term supply agreements, co-branding with regional foodservice chains, and differentiated positioning such as sustainability-certified or grass-fed butter for premium segments, helping stabilize offtake even in weak price cycles.

Additionally, processors and traders should strengthen inventory and price-risk management to limit exposure during prolonged market weakness. High stock levels have amplified price pressure, making it critical to shorten storage cycles, reduce speculative inventory builds, and increase the use of forward contracts and risk-hedging tools. Locking in medium-term contracts with food manufacturers at formula-based pricing can stabilize revenues, while selective use of futures allows participation in any upside ahead of the expected supply tightening in 2026. Positioning strategically during the downturn, rather than chasing short-term volume, will place market participants in a stronger position when butter prices eventually recover.