.jpg)

As of W8 2026, the global wheat market is characterized by a bearish long-term structure driven by record 2025 production. While YoY prices have declined across all tracked origins, most notably in Poland (-10.31%) and France (-8.43%), short-term metrics show stabilization and localized gains. Russian and Ukrainian FOB prices rose MoM by 2.18% and 1.73%, respectively, due to Black Sea logistical disruptions and tightening domestic supplies. US Futures saw a significant 5.56% MoM surge to USD 211.8/mt, underpinned by a decrease in anticipated global supply in 2026. Despite projected lower EU and global production for 2026/27, high inventories currently limit price ceilings. Strategic sourcing should prioritize the US for Americas-based volume and Poland for cost-competitive European procurement, avoiding the logistical volatility inherent in Black Sea trade.

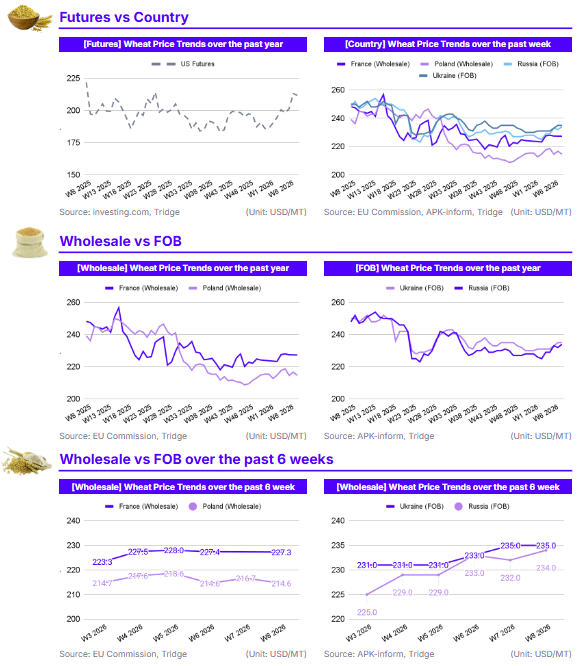

1. Weekly Price Overview

European Markets Stabilize While Black Sea Supply Constraints Drive Modest Price Gains

In Russia, the Free on Board (FOB) price rose 0.86% week-on-week (WoW) to USD 234.0 per metric ton (mt) in W8, supported primarily by adverse weather conditions in Black Sea ports that have hindered logistics. Ukraine’s FOB price remained stable at USD 235.0/mt, maintaining a price equilibrium with Russian origins despite limited domestic supply and heightened seasonal export demand.

In contrast, Western markets experienced slight downward adjustments. Poland’s wholesale price declined 0.97% WoW to USD 214.6/mt, as the market continues to navigate the pressure of high global inventories. France’s wholesale price remained stable at USD 227.3/mt while facing stiff competition from cheaper Black Sea origins, current values are supported by projections of lower domestic yields for the 2026 crop, which is estimated at 33.78 million metric tons (mmt). United States (US) Futures eased 0.67% WoW to USD 211.8/mt. This minor dip represents a correction following a rally the previous week to the highest price in almost 12 months. This recent rise is largely due to lower expected global wheat production in 2026.

2. Price Analysis

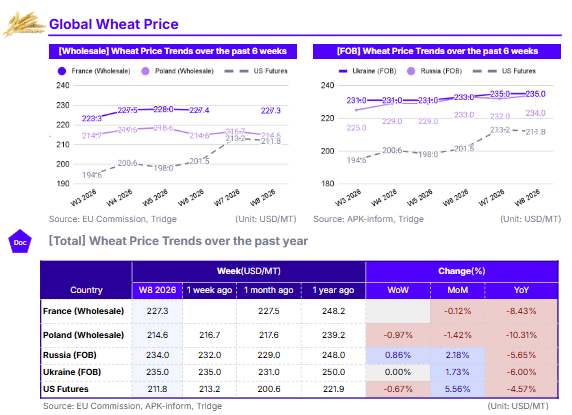

Global Wheat Prices Retain Bearish Long-Term Structure Amid Record 2025 Production

The long-term price analysis for wheat in W8 2026 reveals a market still heavily influenced by the record global harvest of 2025. In Poland, the wholesale price dropped 10.31% year-on-year (YoY) to USD 214.6/mt, while also declining 1.42% month-on-month (MoM). This downward trajectory is driven by a high global supply environment and large domestic carryover, even as Polish production for 2026 is forecast to decline to 13 mmt. Similarly, France's wholesale price stands at USD 227.3/mt, representing an 8.43% YoY decrease. While the French market is stable MoM, it faces significant structural pressure from cheaper Black Sea exports, specifically from Russia and Ukraine, which continue to challenge France’s traditional market share.

In the Black Sea region, Russia’s FOB price of USD 234.0/mt reflects a 5.65% YoY decline, despite a 2.18% MoM increase. The recent MoM strength is a result of logistical disruptions at Black Sea ports, but the YoY decline highlights the impact of Russia's massive 2025 production levels coupled with high global supplies. Ukraine’s FOB price followed a similar pattern, down 6.00% YoY to USD 235.0/mt but up 1.73% MoM due to tightening domestic supply and increased seasonal demand. United States (US) Futures show the most significant short-term recovery, surging 5.56% MoM to USD 211.8/mt, despite remaining 4.57% lower YoY. This MoM rally is supported by the February World Agricultural Supply and Demand Estimates (WASDE) report, which is projecting lower global ending stocks of 277.5 mmt.

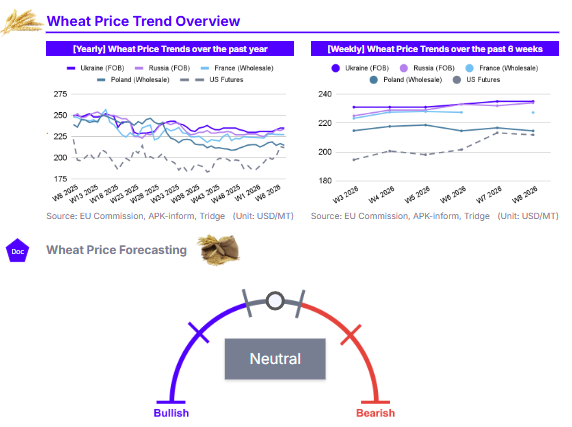

3. Strategic Recommendations

Capitalize on US Stability and Large Stocks for Bulk Procurement

For large-scale importers and millers in the Americas looking to secure significant volume at a competitive price, the US currently offers the most robust supply profile. According to the February 2026 WASDE report, US wheat ending stocks are projected to reach 931 million bushels, a 9% increase over the previous year and the largest inventory since 2019/20. This high domestic availability provides a reliable buffer against global volatility. While US Futures have seen a 5.56% MoM increase to USD 211.8/mt, they remain 4.57% lower than the previous year. Furthermore, the season-average farm price has stabilized at USD 4.90 per bushel. Buyers can leverage this record-high carryout to negotiate long-term supply contracts, mitigating risks associated with the projected tightening of global supplies. Sourcing from the US avoids the logistical uncertainties currently plaguing other regions such as Russia and Ukraine, ensuring consistent delivery schedules for large-scale industrial processing.

Prioritize Poland for Cost-Competitive European Sourcing Amid Logistical Risks in the Black Sea

European wheat buyers should prioritize Poland as their primary origin to optimize procurement costs while avoiding the heightened logistical risks of the Black Sea. As of W8 2026, Poland’s wholesale price of USD 214.6/mt represents the most significant YoY discount among major European producers, down 10.31%. This makes Polish wheat more affordable than French wheat, which carries a premium at USD 227.3/mt. While Black Sea origins like Russia (USD 234.0/mt) and Ukraine (USD 235.0/mt) offer relatively similar price points, they are currently subject to extreme logistical volatility. In contrast, Poland provides a more stable inland and Baltic logistical network. Although Polish production is forecast to decrease slightly to 13 mmt in 2026, the current high global supply continues to suppress local prices, offering a strategic entry point for buyers to lock in volumes before potential upward pressure hits the European market in the medium term.