Webinar Recap: The Sweet Spot: Trends in the Chocolate, Jelly, and Candy Retail Sector

Host: Ben Lategan - Global Market Analyst (South Africa)

Presenter: Mzingaye Ndubiwa - Global Market Analyst (South Africa)

Speakers: Thomas (Dae Sol) Kim - Growth Solution 2 - Assistant Manager - HQ

Wanjugu Gatheru - Business Development Representative - (Kenya)

Alper Akkurt - Global Supply Chain Manager - (Türkiye)

Agenda:

- Global Trends of the Confectionery Market

- Overview of Top Products and Manufacturers

- Panel Discussion

In its November webinar, Tridge experts covered the latest trends in the chocolate, jelly, and candy markets, pointing out emerging trends and sales strategies. Chocolate stands out among confectionery products, consuming over 50% of the market share, while candy and jelly products follow with 30% and 10%, respectively. Among the top manufacturers, Mars Wrigley leads the way with USD 45 billion and famous brands like M&M’s, Snickers, Twix, and Milky Way. According to Tridge panelists, key ingredients such as cocoa, sugar, milk, and nuts influence the prices of the final product, and any supply chain issues reflect the availability and price strategy of the confectionery market. On the production of raw ingredients, stakeholders should monitor production volumes and weather changes, especially in major producing regions. Sustainability remains critical in today’s raw ingredients sector, and one of the ways to overcome obstacles is by diversifying suppliers and production and using modern digital tools like the Tridge platform.

Global Trends of the Confectionery Market

The global confectionery market is valued at USD 229.48 billion in 2023. It is expected to reach USD 322.66 billion in 2032, growing at a compound annual growth rate (CAGR) of 3.8% over the forecast period. Chocolate is the largest segment, accounting for over 50% of the market share, valued at approximately USD 114.7 billion. Candy and jelly or gummy are the second and third largest segments, accounting for 30% and 10% of the market share, respectively. Accounting for 33%, Europe is the largest market globally.

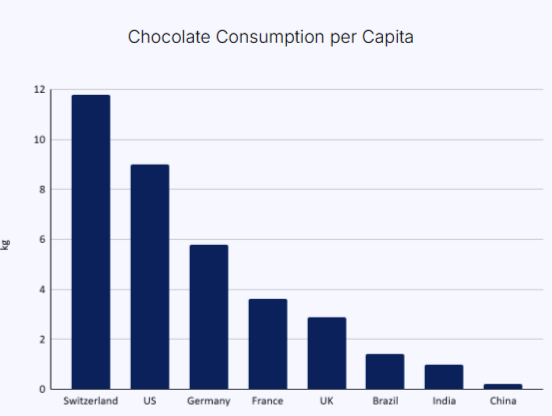

Figure 1. Chocolate Consumption Per Capita

Source: Tridge

The market is evolving as consumer preferences shift. One of the most significant changes is that consumers are buying more premium chocolate. Premium and artisanal chocolate sales increased 12% globally in 2022. This is primarily driven by consumers in Europe who are buying brands like Lindt and Godiva. Consumers are also looking for healthier chocolate. Dark chocolate now accounts for 28% of chocolate sales in the United States (US) compared to 18% a decade ago. Vegan chocolate sales also increased by 19% in 2022.

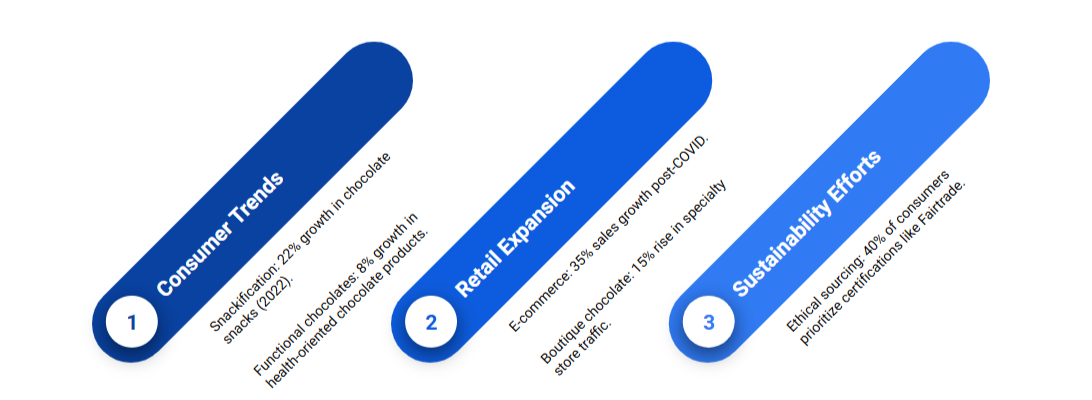

Figure 2. Major Market Drivers for Confectionary Products

Source: Tridge

Overview of Top Products and Manufacturers

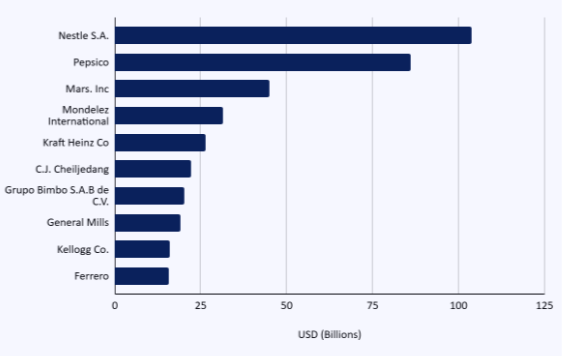

Mars Wrigley is the world’s largest candy company, with annual sales of USD 45 billion. It owns iconic brands such as M&M’s, Snickers, Twix, and Milky Way. The company is committed to sourcing only sustainable cocoa by 2025 and is actively developing innovative products, including sugar-free Skittles and plant-based Snickers.

Ferrero is the second most prominent manufacturer, with annual sales of USD 14 billion. According to Tridge's analyst research, it is expanding and is venturing into selling premium products. Known for brands like Ferrero Rocher, Nutella, and Kinder, Ferrero is renowned for using traditional recipes and high-quality ingredients. This reputation as a premium brand will solidify the company cater to the growing consumer demand for artisanal and high-end chocolates, enabling it to compete effectively with other major players in the confectionery market. To further strengthen its presence in North America and expand its portfolio, Ferrero acquired Ferrara Candy Co.

Nestlé has an annual revenue of USD 9 billion from the confectionery segment. It is adopting sustainable practices and launching new products to expand its business.

Figure 3. Top Global Confectionery Companies by Annual Revenue

Source: Tridge

Panel Discussion:

Wanjugu Gatheru, Thomas (Dae Sol) Kim, and Alper Akkurt shared their insights on the supply and pricing fluctuations of essential raw materials in the agri-food industry. Supply and price fluctuations of key ingredients such as cocoa, sugar, milk, and nuts impact global trade in the food industry. This increases costs, disrupts supply chains and trade, and impacts consumer demand and retail prices. For example, frost in Turkey, the world's largest hazelnut exporter, reduced production and increased prices by 60% in 2014. In Africa, cocoa farmers faced increased shipping costs due to higher fuel prices. In 2020, Ghana and Ivory Coast increased cocoa prices by USD 400 per ton with a new Living Income Differential (LID) policy to ensure that farmers earn more.

Tridge panelists pointed out several important issues regarding key factors agricultural stakeholders should monitor to ensure stability in the supply chain for essential confectionery ingredients. To ensure the stability of the agri-food supply chain, the Tridge team agreed that agricultural stakeholders must monitor several factors, like production volumes, weather risks, global demand, and trade regulations. Production volumes, especially in key regions, must be observed. This allows traders to anticipate availability and identify suitable sourcing locations. Weather is another crucial factor. Adverse weather conditions, such as frost or drought, can negatively impact production volumes.

Tridge's climate intelligence tools allow businesses to monitor weather patterns, reducing the risk of raw material shortages. Additionally, Tridge enables exporters to diversify sourcing options, ensuring stability even during logistical challenges or geopolitical disruptions. For instance, Turkish manufacturers seeking cocoa or sugar suppliers outside traditional markets can rely on Tridge's global network to maintain supply chain continuity and competitive advantage. Tridge insights can also inform decision-makers on consumer preferences through retail and monthly reports. This allows industry players to anticipate sourcing locations and adapt to the market.

Regarding the biggest challenges in sourcing raw materials sustainably and its expected outcomes, Tridge’s panelists shed some light on the matter. Sustainability and sourcing in the confectionary sector are facing challenges. These include deforestation, lack of traceability, high compliance costs, and increased regulation regarding procedures and paperwork. The factors increase costs and complexity in the short term, but it can lead to increased brand loyalty, access to premium markets, and compliance with regulations in the long term.

Companies can mitigate the risk of raw material price increases by diversifying sourcing, entering into long-term contracts, reformulating products, using technology to monitor markets, and collaborating with suppliers. Tridge can help by providing traceability, connecting buyers to responsible suppliers, and providing market intelligence to ensure a sustainable and resilient supply chain.

Click here to view the webinar recording, or click here to see the presentation slides.