W10 2026: Coffee

.jpg)

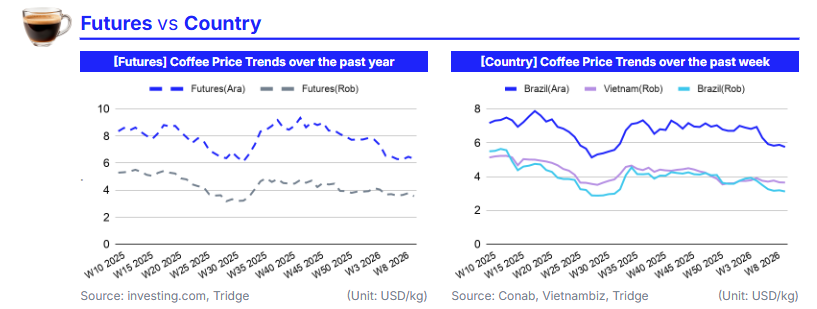

In W10 2026, global coffee prices declined across both Arabica and Robusta markets as expectations of a strong supply recovery, led by Brazil, continued to weigh on sentiment. Arabica futures fell 2.35% WoW, while Robusta dropped more sharply by 6.02% WoW, reflecting stronger downside pressure in the lower-grade segment. The projected Brazilian harvest of up to 71.1 million bags and a global surplus of 7–10 million bags are shifting the market from a weather-driven risk premium toward a supply-driven pricing environment. Rising inventories and strong Vietnamese export growth further reinforce the perception of ample global availability.

At origin level, Brazil’s declining prices and reduced exports indicate short-term supply tightness but do not offset expectations of forward surplus. Vietnam continues to add pressure through expanding Robusta exports, accelerating the normalization of supply-demand balances. This dynamic is particularly evident in Robusta, where faster production growth and substitution in blends are driving a steeper price correction, while Arabica remains relatively supported but constrained by improving crop conditions and easing structural tightness.

For a global coffee manufacturer sourcing Brazilian Arabica for roasted products and Vietnamese Robusta for blends, the core strategy should focus on short-term, opportunistic procurement and cost optimization. Buyers should prioritize flexible sourcing and staggered purchasing to capitalize on continued price weakness, while leveraging Robusta substitution to reduce input costs. As the market transitions into a surplus phase, disciplined, timing-driven procurement offers greater advantage than forward stock accumulation, with near-term price risks remaining skewed to the downside.

1. Weekly Price Overview

Coffee Prices Weaken as Brazil’s Expanding Supply Outlook and Rising Export Competition Reinforce a Bearish Market Environment

In W10 2026, global coffee prices moved lower across both Arabica and Robusta benchmarks, reflecting increasing expectations of a supply recovery led by Brazil. The international Arabica benchmark, represented by US Coffee C Futures, declined 2.35% week-on-week (WoW) to USD 6.31 per kilogram (kg), while Robusta prices fell more sharply by 6.02% WoW to USD 3.55/kg. This downward trend is primarily driven by projections of a significantly larger Brazilian crop, estimated to be between 66 and 70 million bags, with some forecasts reaching 71.1 million bags for the 2026/27 season. The prospect of a global surplus of 7 to 10 million bags is shifting market sentiment toward sustained oversupply, outweighing short-term volatility linked to weather risks and export fluctuations.

In Brazil, both Arabica and Robusta prices declined by 2.17% WoW to USD 5.75/kg and USD 3.12/kg, respectively, aligning with the global bearish trend. Although exports dropped 17.4% year-on-year (YoY) in Feb-26, temporarily tightening prompt availability, this has not offset the broader expectation of increased forward supply. In Vietnam, Robusta prices declined by 0.30% WoW to USD 3.65/kg, despite strong export growth (+56.4% YoY in volume), reinforcing the view that expanding export flows are adding further pressure to global prices.

2. Price Analysis

Improving Supply Expectations Drive Broad Coffee Price Correction Despite Short-Term Arabica Stability

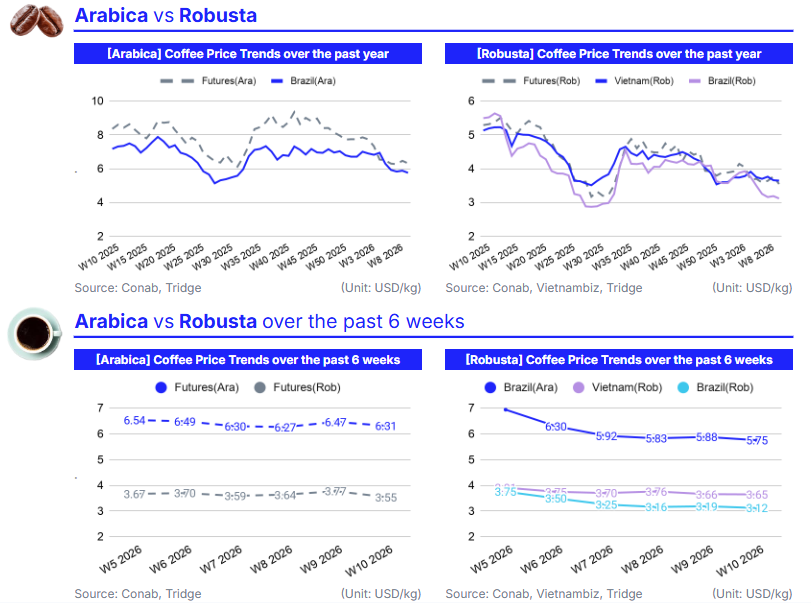

As of W10 2026, global coffee prices are adjusting downward, reflecting a clear shift in market fundamentals from supply tightness toward anticipated surplus. Arabica futures rose marginally by 0.25% month-on-month (MoM) to USD 6.30/kg, but this increase is largely technical and does not signal a reversal in trend. In contrast, Robusta futures declined by 1.28% MoM and 32.99% year-on-year (YoY), confirming a more pronounced bearish trajectory. The primary cause of this divergence lies in supply expectations; favorable weather conditions in Brazil are reinforcing projections of a large 2026/27 harvest, while rising certified inventories on the New York exchange are signaling improved short-term availability. Together, these factors have weakened the risk premium that previously supported prices, particularly in the Robusta segment, where supply expansion is more immediate.

This supply-driven correction is further reflected in origin markets. In Brazil, Arabica prices declined by 2.88% MoM and 19.78% YoY, while Robusta fell more sharply by 4.15% MoM and 43.26% YoY. The magnitude of the Robusta decline indicates a faster normalization of supply-demand balance, driven by both domestic production growth and substitution dynamics in global blending. Arabica, while also declining, remains comparatively supported due to its tighter structural balance and premium positioning. Importantly, despite recent declines, Arabica prices remain historically elevated, suggesting that the current adjustment reflects easing scarcity rather than oversupply. Producer behavior is reinforcing this dynamic: Brazilian exports fell 17% YoY in Feb-26 as farmers withheld volumes, slowing the pace of price declines but not altering the underlying bearish sentiment.

In the global context, Vietnam’s Robusta prices declined by 1.43% MoM and 28.92% YoY, driven by stable production outlooks and subdued demand. Although logistical disruptions linked to Middle East tensions have increased freight costs, these have not translated into meaningful supply constraints, indicating that physical availability remains sufficient. This highlights a key market dynamic: cost-side pressures, such as freight, are currently being outweighed by supply-side improvements, limiting their impact on price formation.

Coffee prices are expected to follow a bearish-to-neutral trajectory in the short term. Robusta is likely to remain under the greatest pressure, as synchronized production strength in Brazil and Vietnam continues to expand global availability and reduce reliance on Arabica substitution. Arabica prices may stabilize within a narrower range, supported by quality differentiation and residual weather risk, but upside potential is constrained unless there is a material deterioration in crop conditions. The market is transitioning into a supply-led phase, where price direction will be increasingly determined by harvest realization, inventory accumulation, and the timing of producer selling rather than scarcity-driven volatility.

3. Strategic Recommendations

Adopt a Tactical, Short-Coverage Procurement Strategy as Global Coffee Markets Shift to Surplus

Global coffee markets are transitioning into a supply-led phase, with expanding production in Brazil and Vietnam and a projected surplus of 7–10 million bags driving a sustained bearish bias. The sharper decline in Robusta prices, combined with rising inventories and improving export flows, indicates that the current correction is structural rather than temporary. While Arabica shows relative resilience, its upside is constrained by easing supply tightness and improving crop conditions. As a result, trade strategies should prioritize flexibility, cost optimization, and timing rather than forward accumulation.

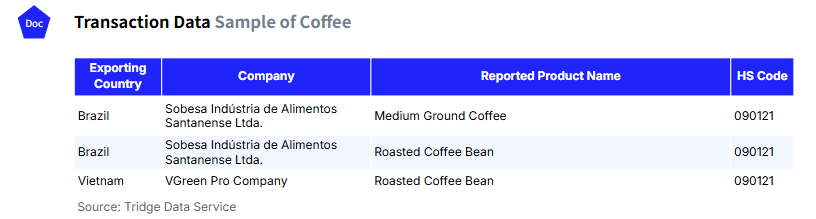

From a strategic perspective, buyers should adopt a short-duration and opportunistic procurement model. Arabica sourcing should focus on phased purchasing, particularly from Brazil, where suppliers such as Sobesa Indústria de Alimentos Santanense Ltda. continue to export medium ground and roasted coffee. Given that Arabica prices remain historically elevated despite recent declines, buyers should avoid heavy forward commitments and instead secure volumes incrementally during market dips. This approach preserves downside participation while maintaining protection against potential weather-related supply shocks.

For Robusta, a defensive and cost-driven strategy is recommended. The combination of strong Vietnamese export growth and synchronized supply expansion suggests continued price pressure. Buyers should prioritize short-term or spot contracts and maintain minimal inventory levels to capture further downside. Vietnam remains the most competitive origin, with exporters such as VGREEN PRO Company supplying roasted coffee beans into global markets. Increased substitution toward Robusta in blends should be actively leveraged to reduce input costs, particularly as the Arabica–Robusta spread remains wide.

According to Tridge Eye’s transaction data explorer, ongoing export activity from Brazil and Vietnam confirms improving supply liquidity across both origins. Sobesa Indústria de Alimentos Santanense Ltda. continues to supply both medium ground and roasted coffee from Brazil, while VGREEN PRO Company maintains steady Robusta shipments from Vietnam. These flows indicate that availability is not a constraining factor, strengthening the case for tactical, demand-aligned procurement rather than forward stock accumulation.

Execution should focus on dynamic sourcing aligned with market movements, combining selective Arabica purchasing during corrections with opportunistic Robusta buying under continued price pressure. Contract structures should emphasize flexibility in delivery and pricing mechanisms to adapt to ongoing volatility, while procurement teams should continuously monitor harvest developments and inventory trends to refine entry points. This approach ensures cost efficiency while preserving the ability to respond quickly to any shift in supply conditions or market sentiment.