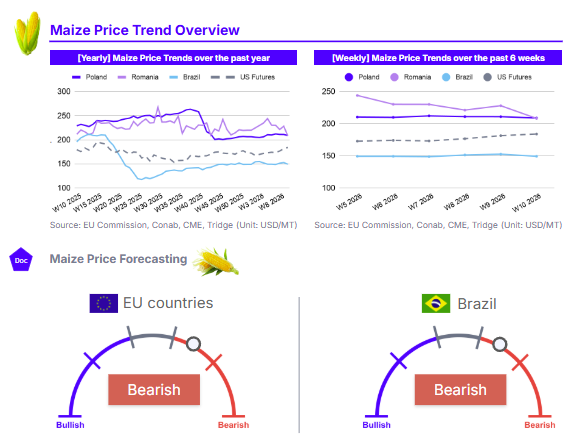

W10 2026: Maize

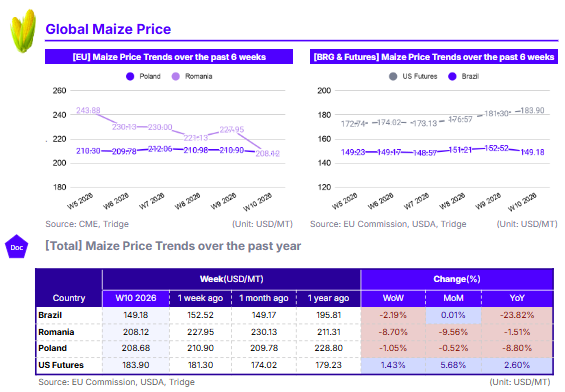

In W10 2026, global maize prices exhibited divergent trends, with US Futures (USD 183.90/mt) rising 1.43% WoW and 5.68% MoM, driven by record-high export commitments and strong demand from Mexico. Conversely, Brazil (USD 149.18/mt) fell 2.19% WoW, pressured by geopolitical conflict affecting exports to Iran, despite a 1 mmt increase in 2025/26 production forecasts. In the EU, Romania (USD 208.12/mt) saw a sharp 8.70% WoW drop due to improved 2026 yield expectations and rising global ending stocks. Poland (USD 208.68/mt) remained stable, with a 1.05% WoW decline, supported by its large 2025 harvest of 10.3 mmt. Overall, high global supplies weigh on long-term values, but record US exports provide upward short-term pressure. Buyers are advised to prioritize Poland for cost-effective EU supply and the US for large-volume global needs.

1. Weekly Price Overview

Strong US Exports Clash with Expanding Global Stocks

In the United States (US), the price of maize rose 1.43% week-on-week (WoW) to USD 183.90 per metric ton (mt) in W10. This increase is primarily driven by record-breaking export demand, with commitments reaching 2,558 million bushels for the week ending 26 Feb-26, the highest on record for this period. Strong procurement from Mexico and robust domestic use for ethanol continue to provide upward price support despite a large 2025 domestic and global harvest. Conversely, Brazil experienced a 2.19% WoW decline to USD 149.18/mt. This downward pressure is largely linked to geopolitical tensions due the US-Iran conflict affecting exports to Iran, a major destination for Brazilian maize. While the March 2026 WASDE report raised Brazil's anticipated 2025/26 production by 1 million metric tons (mmt) to 132 mmt, increased domestic ethanol demand and growing exports to China are acting as a partial buffer against steeper losses.

European markets also showed a downward trend, most notably in Romania, where prices plummeted 8.70% WoW to USD 208.12/mt. This sharp correction is attributed to the optimistic 2026 European Union (EU) outlook, with Romanian production expected to increase to 7.79 mmt due to recovering yields. Furthermore, the March WASDE report’s increase of global corn ending stocks to 292.8 mmt has weighed heavily on regional sentiment. Poland demonstrated more resilience, with its price edging down 1.05% WoW to USD 208.68/mt. While high global supplies and a large 2025 Polish harvest of 10.3 mmt exert downward pressure, the market is partially stabilized by forecasts of a smaller 2026 crop (9.62 mmt) due to reduced acreage and yield.

2. Price Analysis

Heavy Global Inventories Pressure Long-Term Values Despite Surging US Export Demand

In the US, maize prices increased 5.68% over the past month, bringing the total price increase for the year to 2.60% at USD 183.90/mt. This bullish trend is largely the result of exceptional export demand, which has persisted despite large domestic and global production levels in 2025. Mexico, a major importer of US maize, continues to drive volume, helping US prices decouple from the broader global downward trend. While the 2025 harvest was record-breaking, the consistent pace of foreign sales has provided significant month-on-month (MoM) support.

Brazil’s price stands at USD 149.18/mt, remaining nearly flat MoM with a 0.01% increase, but showing a substantial 23.82% decline year-on-year (YoY). The heavy YoY deflation is primarily driven by the production recovery during the 2024/25 cycle, which reached 136 million metric tons (mmt). The March 2026 WASDE report further reinforced this long-term pressure by raising anticipated 2025/26 production to 132 mmt. While increasing domestic ethanol production and exports to China provide a floor for prices, the large available supply keeps long-term values well below previous year levels.

In Romania, maize prices fell 9.56% over the past month, contributing to a 1.51% YoY decrease to USD 208.12/mt. This downward trajectory is fueled by the optimistic 2026 outlook for the EU, with Romania’s own production expected to grow to 7.79 mmt due to higher yields. Similarly, Poland’s price decreased 8.80% YoY to USD 208.68/mt, with a marginal 0.52% MoM decline. While Poland saw slight price firming in Euro terms due to a projected smaller 2026 harvest of 9.62 mmt, the overall global surplus and high ending stocks continue to weigh on Polish prices in USD terms.

3. Strategic Recommendations

Prioritize Poland for Cost-Effective EU Maize Procurement

European buyers and industrial processors should continue to prioritize Poland as the primary sourcing origin within the EU. While prices in Romania have experienced a significant sharp correction, falling 8.70% WoW and 9.56% MoM to USD 208.12/mt, Poland remains highly competitive at USD 208.68/mt. Although Polish prices are slightly higher in Euro terms, the market is pressured by the large 10.3 million metric tons (mmt) harvest from 2025, which remains 23.19% above the five-year average. Sourcing from Poland offers a strategic hedge against the volatility seen in Romania, where prices are reacting more aggressively to the optimistic 2026 EU production outlook and rising global ending stocks. Importers should utilize the current price floor in Poland to secure requirements before potential further firming in Euro terms, driven by projections of a smaller 9.62 mmt Polish crop in 2026.

Capitalize on Plentiful US Supply Amidst Record Export Demand

Global importers requiring high liquidity and large volumes should focus procurement on the US, despite current price firming. While US prices are up 5.68% MoM, they remain a reliable source for large-scale buyers due to the record 2025 harvest and the efficiency of US supply chains. The current strength in US prices, supported by heavy procurement from Mexico, suggests that waiting for a price dip may be risky as exports continue at a record pace. Furthermore, with Brazil facing potential export disruptions to Iran due to geopolitical conflict, the US offers a more stable alternative for the Americas. Large-scale buyers should leverage the high liquidity of the US market to fulfill long-term inventory needs, securing supply before the anticipated smaller 2026 harvest potentially triggers a market correction.