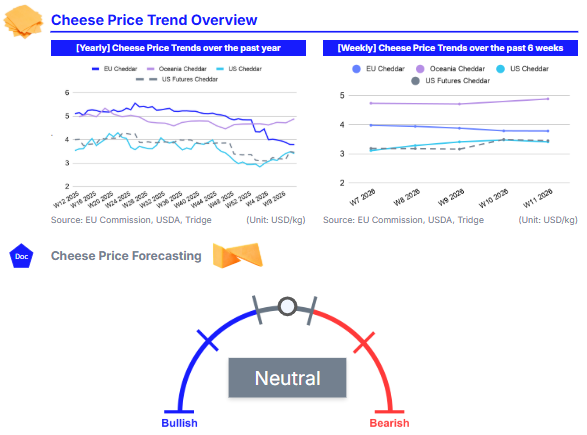

In W11, EU cheddar prices held steady WoW but declined MoM and YoY due to abundant milk supply and weak export competitiveness, despite stable local demand. In the US, cheddar prices fell on a weekly and yearly basis but rose monthly, supported by rising production, herd expansion, and stronger exports. Oceania led performance, with cheddar up on both a weekly and monthly basis, driven by robust Asian demand and seasonal milk tightening. Across regions, short-term price movements remain highly sensitive to inventory management, seasonal milk availability, and spot market dynamics. Strategically, EU processors could benefit from focusing on domestic and value-added channels, while US producers are advised to align output with export demand and high-value cheese varieties. Meanwhile, Oceania suppliers should leverage seasonal supply constraints to secure premium pricing in export markets.

1. Weekly Price Overview

Cheddar Prices Show Mixed Trends Globally Amid Supply Overhang and Export Demand Shifts

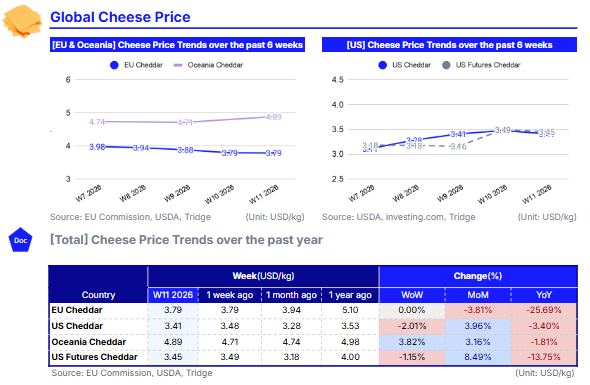

In W11 2026, cheddar prices in the European Union (EU) remained unchanged week-on-week (WoW) at USD 3.79 per kilogram (kg) but declined by 3.81% month-on-month (MoM) and 25.69% year-on-year (YoY), highlighting persistent bearish pressure. This downward trend is largely attributed to ample milk supply carried over from 2025 and weakened export competitiveness, which continue to weigh on price recovery.

In contrast, the United States (US) market showed mixed signals, with cheddar prices averaging USD 3.41/kg, down 2.01% (WoW) and 3.40% YoY, but rising 3.96% MoM. The weekly decline reflects softer spot market activity and subdued domestic demand, as inflationary pressures continue to constrain consumer spending. However, stronger export performance has provided partial support, contributing to the monthly increase. Similarly, US cheddar futures averaged USD 3.45/kg, declining by 1.15% WoW and 13.75% YoY, but posting a notable 8.49% MoM gain. The short-term weekly drop suggests a market correction rather than a reversal of the upward trend, driven by near-term factors such as weaker spot prices at the Chicago Mercantile Exchange (CME) in early Mar-26 and cautious trader sentiment.

Meanwhile, Oceania emerged as the strongest-performing region, with cheddar prices rising by 3.82% WoW and 3.26% MoM to USD 4.89/kg, although still slightly down by 1.81% YoY. The upward momentum is supported by robust export demand from Asia, particularly China and Southeast Asia, combined with seasonally tightening milk production, which has reinforced prices through active participation in Global Dairy Trade (GDT) auctions.

2. Price Analysis

Global Cheddar Markets Display Mixed Trends Due to Herd Expansion, Seasonal Production, and Export Demand

The GDT Event 400, held on March 17, 2026, the dairy index rose by 0.1% from the previous event, with average winning price at USD 4,330 per metric ton (mt). Cheese markets were resilient, with Cheddar averaging USD 4,925/mt, up 0.1%, and Mozzarella stood at USD 4,208/mt, up 0.5% compared to the previous event.

The price increases come amid pressures on global milk production, particularly in key exporting regions. Seasonal milk production in New Zealand is tapering off post-peak, limiting immediate exportable volumes, while processors in Europe and the US are strategically holding stocks to recover margins after a challenging 2024/25 period. In the US, United States Department of Agriculture (USDA) data indicates that dairy producers generated 18.255 billion pounds (lbs) of milk in Feb-26, up 2.9% from Feb-25, supported by herd expansion, which reached 9.615 million heads in Feb-26, 211,000 more than the previous year.

Similarly, Europe saw robust milk output in Feb-26, aided by disease recovery, favorable forage quality, and low input costs, contributing to growth in production volumes despite high inventory levels of skim milk powder (SMP) and butter. Feb-26 wholesale data from the Milk Market Observatory reported an average cheese price decline of 3.7% MoM, with Cheddar dropping 8.8%, Gouda 5.4%, Edam 1.8%, and Emmental 0.3%. The downward trend was partly due to ample regional milk supplies supporting production, combined with modest export competitiveness in the EU, although demand from retail and foodservice sectors remained stable. Despite the price dip, European processors maintained steady production schedules, contributing to ongoing availability for local consumption and limited but strategic exports.

Overall, the global cheese market in Mar-26 demonstrates a regional divergence, with the US market is supported by rising production, herd expansion, and export-driven demand, supporting higher Cheddar and Mozzarella prices, whereas Europe faces moderate pressure on cheese prices due to strong supply and competitive export conditions. Across both regions, short-term price movements remain highly sensitive to spot market activity, inventory management, and seasonal milk availability, signaling a cautiously bullish outlook for cheese commodities over the coming months.

3. Strategic Recommendations

Actionable Approaches for Stable Cheese Margins During Regional Price Divergence

Given the current global cheese market dynamics in the EU, where cheddar prices are under persistent bearish pressure due to abundant milk supplies and weakened export competitiveness, processors should consider diversifying sales channels to reduce reliance on slow-moving exports. For instance, targeting domestic retail and foodservice segments with value-added cheese products, such as pre-sliced or flavored cheddar, can help maintain margins and stimulate local demand. EU exporters can also explore dynamic pricing strategies to remain competitive in selective overseas markets where demand is stable or growing, such as North Africa or parts of Southeast Asia, while reducing bulk exposure to highly price-sensitive regions.

In the US, where cheddar prices show mixed trends, strategies should focus on leveraging export growth and spot market opportunities. With herd expansion and rising milk production, processors can increase forward contract volumes to secure stable margins while maintaining flexibility to respond to spot market fluctuations at the CME. Active monitoring of domestic consumption trends is crucial, as inflationary pressures are dampening retail spending; processors could introduce promotional campaigns or bundled cheese products to sustain volume sales. Additionally, the US market benefits from rising Mozzarella prices, suggesting processors could align production portfolios toward higher-demand varieties to capture favorable pricing while balancing Cheddar supply.

For Oceania, the strongest-performing region due to robust Asian export demand and seasonal milk tightening, players should focus on maximizing export leverage. Forward booking with strategic buyers in China and Southeast Asia, particularly during periods of limited seasonal supply, can lock in premium pricing and reduce exposure to spot-market volatility. Additionally, processors could invest in seasonal production smoothing, such as temporary storage or controlled cheese maturation, to better match export demand spikes and maintain price stability.