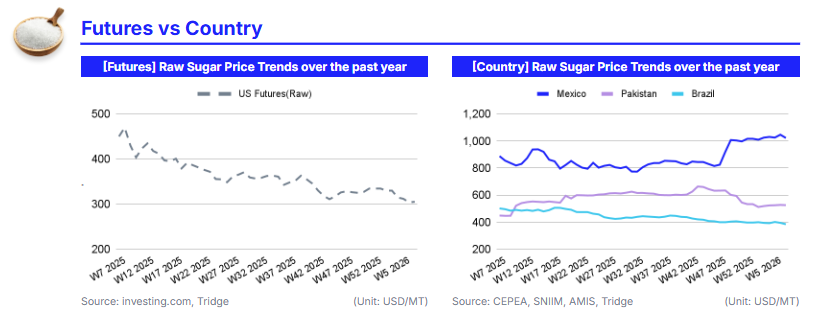

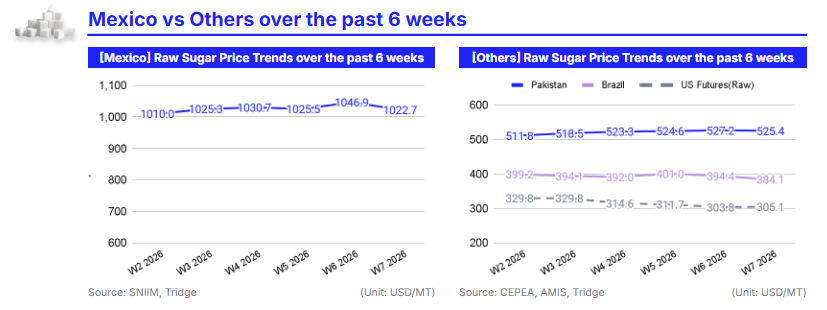

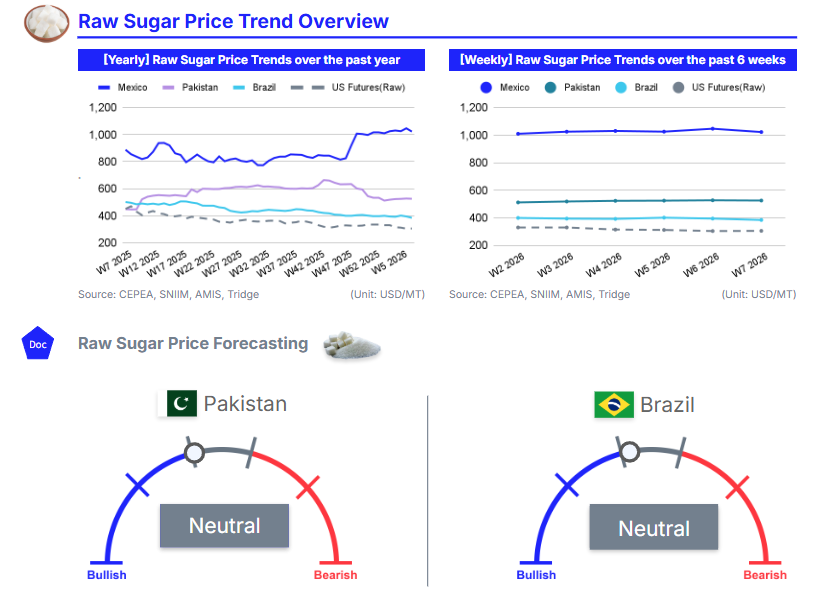

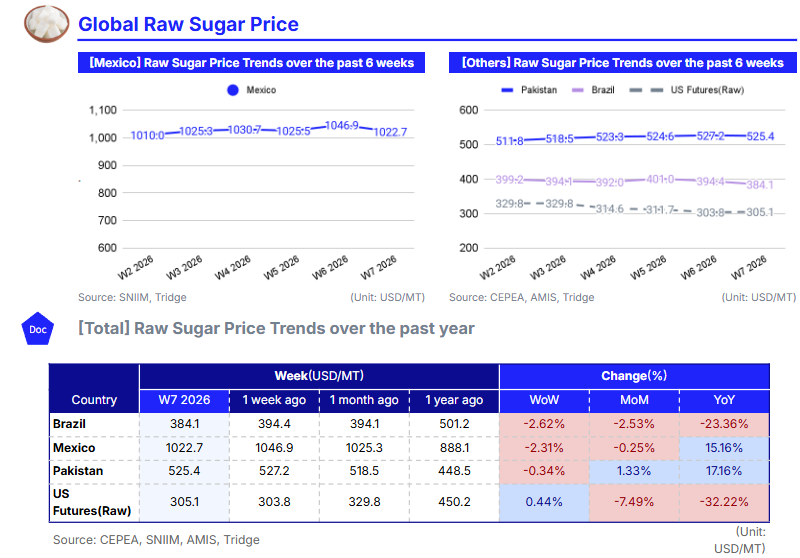

In W7 2026, global sugar prices remain under pressure amid surplus-driven fundamentals, with Brazil continuing to anchor the low end of the global cost curve. Brazilian prices declined 2.62% WoW to USD 384.1/mt and remain sharply lower on a YoY basis, reflecting ample prompt availability despite forward-looking signals of tighter supply linked to a higher ethanol mix in 2026/27. Mexico’s prices softened modestly by 2.31% WoW but remain elevated YoY due to policy distortions rather than supply tightness, while Pakistan’s slight easing reflects improving domestic balances following strong crushing performance. US raw sugar futures remain near multi-year lows, reinforcing expectations of comfortable global availability.

For global food manufacturers sourcing Brazilian sugar, the core strategy is to maintain defensive, cost-focused procurement anchored in Brazil through staggered short-term contracts. With surplus conditions dominating and ethanol-driven tightening unlikely to affect near-term exports, buyers should prioritize flexible coverage from Brazil, treat Mexico as a tactical origin only, and avoid chasing prices in Pakistan. Overall, the market outlook supports a bearish-to-neutral stance, favoring disciplined near-term sourcing over long forward commitments until clearer evidence of global supply tightening emerges.

1. Weekly Price Overview

Weekly Sugar Prices Extend Losses as Global Surplus Pressure Outweighs Emerging Supply Adjustments

In W7 2026, global sugar markets remained under pressure, with prices across key origins reflecting surplus-driven fundamentals despite emerging region-specific adjustments. In Brazil, sugar prices declined 2.62% week-on-week (WoW) to USD 384.1 per metric ton (mt), tracking international benchmarks that touched five-year lows amid a persistent global surplus. Over the past two weeks, price weakness has been driven by ample near-term availability and subdued futures, despite medium-term signals indicating a potential shift in production dynamics. Consultancy Safras & Mercado forecasts Brazil’s 2026/27 sugar output to fall 3.91% year-on-year (YoY) to 41.8 million metric tons (mmt), with exports expected to decline 11% YoY to around 30 mmt. However, this prospective tightening has not yet translated into price support, as mills are increasingly incentivized to divert cane to ethanol production. Ethanol prices in Brazil are currently estimated to be 30–40% higher than sugar, supported by a 20.7% YoY drop in Center-South ethanol stocks and multi-year high biofuel prices. As a result, around 53% of cane is expected to be allocated to ethanol in 2026/27, reversing the sugar-heavy mix of the current season, though inventories are expected to rebuild later in the year.

In Mexico, sugar prices fell 2.31% WoW to USD 1,022.7/mt, continuing a gradual softening trend. Recent price movements reflect policy uncertainty rather than immediate supply shocks. Sugarcane growers are pressing for changes in the upcoming United States-Mexico-Canada Agreement (USMCA) review, citing the long-standing suspension agreement that has progressively reduced Mexico’s tariff-free export quota to the United States (US). With expected exports to the US potentially falling to around 188,000 tons this year, and concerns that the quota could eventually be eliminated, Mexican sugar is increasingly exposed to low-priced global supplies. Despite high import tariffs imposed by Mexico on non-trade-agreement partners, low world prices continue to cap domestic upside, reinforcing the recent decline.

Pakistan’s sugar prices eased slightly, down 0.34% WoW to USD 525.4/mt, as improving domestic supply conditions offset earlier tightness. Over the past fortnight, sentiment has softened following a strong crushing performance in Punjab, where mills have processed 30.83 mmt of cane and produced 2.93 mmt of sugar, with recovery rates improving to 9.69%. Carry-forward stocks have fallen sharply YoY, but adequate current availability and the start of the spring planting season, supported by favorable weather and improved varieties, have reduced near-term supply concerns. High payment clearance rates to growers and stable ex-mill prices further suggest a more balanced domestic market.

In the US, raw sugar futures rose marginally by 0.44% WoW to USD 305.1/mt but remain near their lowest levels since Oct-20. Over the past two weeks, futures have been constrained by expectations of a large global surplus in 2025/26, underpinned by good growing conditions for cane and beet crops and rising output in major producers such as India and Thailand. With global consumption projected to remain broadly stable, the market continues to price in comfortable availability.

Sugar price movements in W7 2026 reflect a market dominated by surplus conditions and weak global benchmarks. While Brazil’s anticipated shift toward ethanol and lower forward sugar production could tighten supply later in the cycle, current prices remain anchored by ample stocks and strong output across multiple origins. Absent a material weather shock or abrupt policy-driven supply restriction, sugar markets are likely to stay under downward pressure in the near term, with only gradual stabilization possible as production mix adjustments take effect.

2. Price Analysis

Sugar Prices Remain Under Pressure as Surplus Conditions Dominate Despite Emerging Ethanol Support

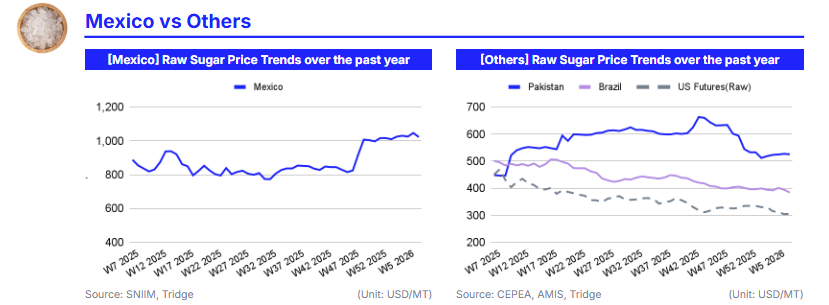

As of W7 2026, sugar prices continue to reflect a surplus-driven market, with declines across most key origins. In Brazil, prices fell 2.53% month-on-month (MoM) to USD 394.1/mt and remain sharply lower (23.29% YoY), confirming that ample global availability and weak international benchmarks continue to outweigh prospective supply tightening. The recent price weakness is largely the result of strong 2025/26 supply, high carry-in stocks, and limited near-term export urgency. Although Brazilian mills are signaling a greater allocation of cane to ethanol at the start of the 2026/27 crushing season, driven by ethanol prices that are materially higher than sugar, this shift has not yet reduced prompt sugar availability. As a result, the ethanol arbitrage is acting as a forward-looking support factor rather than an immediate price driver.

In Mexico, sugar prices edged down 0.25% MoM to USD 1,025.3/mt but remain elevated on a YoY basis (+15.16%). The mild monthly softening reflects easing domestic pressure rather than a change in structural balance. Government support programs for sugarcane growers are likely to improve liquidity and productivity over time, but in the near term, they do not materially tighten supply. Therefore, prices remain vulnerable to normalization if domestic output improves and access to global sugar remains available at lower prices.

Pakistan stands out with prices rising 1.33% MoM and 17.16% YoY to USD 448.5/mt, driven by tighter local balances. Falling carry-forward stocks, strong crushing performance, and improved recovery rates have supported prices despite rising output. However, the start of the spring planting season and favorable weather conditions point to improved supply prospects later in the cycle, which should limit further upside.

In the US, raw sugar futures declined 7.49% MoM and over 32% YoY, reinforcing the global bearish signal. Futures markets continue to price in a large global surplus for 2025/26, supported by good crop conditions and stable consumption growth, which has capped any sustained recovery attempts.

Sugar prices are expected to remain under pressure in the near term, with a bearish-to-neutral bias. Brazil’s anticipated shift toward ethanol could provide episodic support in early 2026/27 by tightening export availability, but this is likely to be gradual and insufficient to drive a sharp rebound while global stocks remain comfortable. Mexico is likely to see sideways-to-softer pricing as productivity measures take effect, while Pakistan may stabilize as new supply enters the market. Overall, absent a significant weather disruption or abrupt policy-driven supply restriction, sugar prices are more likely to consolidate at low levels than to stage a durable recovery over the coming months.

3. Strategic Recommendations

Defensive Procurement Favored as Surplus Conditions Persist and Brazil Remains the Cost Anchor

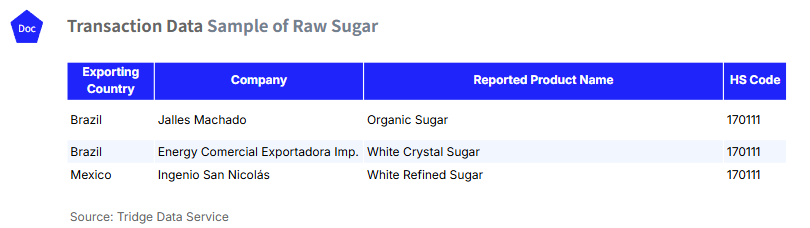

Given the surplus-driven market structure and the bearish-to-neutral price bias evident in W7 2026, sugar buyers and traders should adopt a defensive, cost-focused strategy anchored in low-cost origins and flexible execution. With Brazilian prices still trending lower on both a WoW and YoY basis, and global benchmarks near multi-year lows, international importers should prioritize Brazil as the primary sourcing origin for the next two to three months. Despite growing expectations that a higher ethanol mix could tighten sugar availability later in the 2026/27 cycle, current prompt supply remains ample, and price support has not yet materialized. According to Tridge’s Eye transaction data explorer, Brazilian export flows remain active across product types, including Organic Sugar, White Crystal Sugar from Energy Comercial Exportadora Imp, and other standard grades, indicating that physical availability is sufficient to support incremental forward procurement at current levels.

From a trade execution perspective, buyers are advised to secure short- to medium-term coverage through staggered contracts rather than locking in large forward positions. This approach allows importers to benefit from continued downside risk while gradually building protection against potential late-cycle tightening linked to ethanol arbitrage or weather-related delays to the crushing season. Opportunistic extensions of coverage should be considered on any technical rebounds in futures or FOB offers, but overall exposure should remain light until clearer evidence of export tightening emerges.

Mexico should be treated as a secondary and tactical origin. Although prices remain elevated on a YoY basis, recent WoW declines and ongoing policy uncertainty around USMCA quota negotiations increase downside risk. Traders with access to Mexican refined sugar should consider accelerating sales into the current price window, particularly as low-priced global sugar continues to cap domestic upside. Tridge’s Eye transaction data confirms the ongoing availability of White Refined Sugar from Ingenio San Nicolás, suggesting that near-term supply continuity is intact and that holding long inventory positions carries an increasing risk of normalization.

In Pakistan, the recent stabilization following strong crushing performance and improving recovery rates supports a neutral stance. Buyers should avoid chasing prices higher, as improving planting conditions and rising output are likely to limit further upside. Export-oriented strategies should remain cautious and opportunistic rather than directional.

The recommended action plan is to remain lightly covered physically from Brazil, monetize relative price strength in Mexico where possible, and maintain downside protection through conservative hedging. A bearish-to-neutral trading posture remains appropriate, with flexibility preserved to respond to any unexpected weather shock or abrupt policy-driven supply disruption later in the year.