W8 2026: Coffee

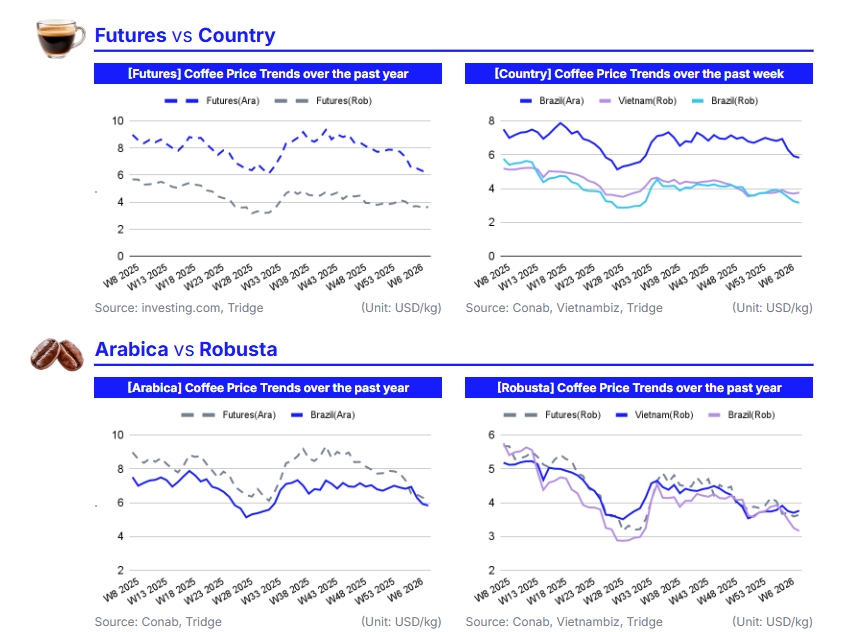

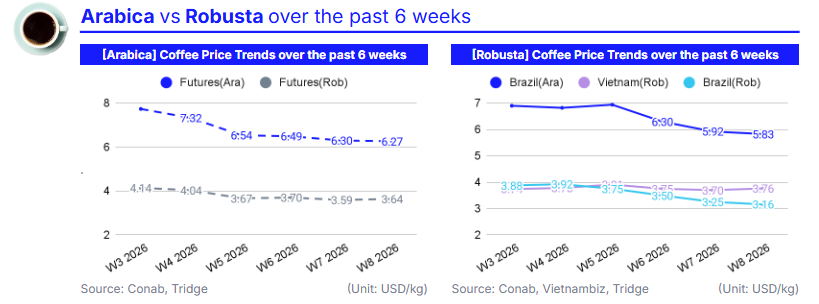

In W8 2026, global coffee prices remained under pressure as improving supply expectations from Brazil and Vietnam continued to reshape market dynamics. Arabica futures declined 0.51% WoW to USD 6.27/kg, while Robusta increased 1.34% WoW to USD 3.64/kg, though both benchmarks remain near multi-month lows following a broader three-week correction. The downward trend reflects a shift from the weather-driven risk premium observed in 2025 toward a supply normalization phase.

Brazil’s production outlook remains the primary driver of market sentiment. CONAP projects 2026 coffee production to rise 17.2% YoY to a record 66.2 million bags, supported by favorable rainfall in Minas Gerais and improved crop development. At the same time, Vietnam continues to reinforce global supply availability, with Jan-25 exports increasing 38.3% YoY and production forecast to grow 6% YoY. Recovering ICE-certified inventories further confirm improving supply conditions, contributing to continued price pressure.

For global buyers sourcing Brazilian Arabica for roasted products and Vietnamese Robusta for blends, the procurement strategy should emphasize short-duration coverage and tactical purchasing. Arabica volumes should be secured selectively during market dips to hedge weather volatility in Brazil, while Robusta sourcing should remain flexible and short-term, prioritizing Vietnamese origin to capture potential further downside linked to expanding export supply.

Positioning should remain liquidity-focused and opportunistic. As the market transitions toward supply adequacy, disciplined short-term procurement and staggered coverage provide greater advantage than aggressive forward buying, with the near-term outlook for both Arabica and Robusta remaining neutral to bearish.

1. Weekly Price Overview

Coffee Prices Remain Under Pressure as Brazil’s Record Crop Outlook and Rising Global Supply Weigh on Market Sentiment

In W8 2026, global coffee prices showed mixed movements but remained under pressure overall as expectations of stronger supply continued to shape market sentiment. The international Arabica benchmark, represented by US Coffee C Futures, declined by 0.51% week-on-week (WoW) to USD 6.27 per kilogram (kg). Meanwhile, Robusta, represented by London Coffee Futures, increased by 1.34% WoW to USD 3.64/kg. Despite the slight weekly rebound in robusta, both benchmarks remain near recent lows, with arabica reaching its lowest level in more than seven months and robusta touching a six-month low. The broader decline observed over the past three weeks has been driven largely by expectations of a significant recovery in global coffee supply, particularly from Brazil.

Supply outlooks strengthened after Brazil’s crop forecasting agency, the National Supply Company (CONAB), projected on February 5 that the country’s 2026 coffee production will increase by 17.2% year-on-year (YoY) to a record 66.2 million bags. Arabica output is expected to rise 23.2% to 44.1 million bags, while robusta production is forecast to grow 6.3% to 22.1 million bags. Favorable weather conditions have reinforced this outlook. According to Somar Meteorologia, Minas Gerais, Brazil’s largest arabica-producing region, received 72.6 millimeters (mm) of rainfall at the end of W6, equivalent to 113% of the historical average, which improved crop development and reinforced expectations of a strong upcoming harvest.

Price movements in Brazil reflected the softer global environment. Brazilian arabica prices declined by 1.62% WoW to USD 5.83/kg, while robusta prices fell 2.91% WoW to USD 3.16/kg. Export data also signaled weaker market conditions. According to the Brazilian Coffee Exporters Council (Cecafé), Brazil exported 2.78 million 60-kg bags of coffee in Jan-26, down 30.8% from 4.016 million bags in Jan-25, while export revenue declined 11.7% to USD 1.175 billion. The decline was attributed to falling prices since Jan-26, expectations of a stronger 2026/27 crop, and a weaker US dollar that reduced trade momentum. Arabica remained the dominant export category with 2.347 million bags, representing 84.4% of total shipments.

In Vietnam, the world’s largest robusta exporter, domestic coffee prices increased by 1.70% WoW to USD 3.76/kg. However, rising export volumes continue to weigh on the global robusta market. Vietnam’s National Statistics Office reported that Jan-26 coffee exports surged 38.3% YoY to 198,000 metric tons (mt), while total exports for 2025 rose 17.5% YoY to 1.58 million metric tons (mmt). Production prospects are also improving, with Vietnam’s 2025/26 output forecast to increase by 6% YoY to 1.76 mmt, equivalent to 29.4 million bags, marking a four-year high.

Additional pressure on prices has come from rising exchange-monitored inventories. ICE arabica stocks rebounded from a 1.75-year low of 396,513 bags in Nov-25 to 461,829 bags in early Jan-26, while ICE robusta inventories increased from a 13-month low of 4,012 lots in Dec-25 to 4,662 lots by late Jan-26. The combination of improving weather conditions in Brazil, expanding export supply from Vietnam, and recovering certified inventories has reinforced expectations of greater supply availability, keeping global coffee prices under downward pressure over the past two to three weeks.

2. Price Analysis

Global Coffee Prices Decline as Expanding Brazil and Vietnam Supply Signals Shift Toward Market Surplus

As of W8 2026, global coffee prices declined sharply compared with last year as improving production prospects and expanding supply from major origins shifted the market from a scarcity-driven environment toward supply normalization. Arabica coffee futures fell 30.23% YoY from USD 8.98/kg, while Robusta futures declined 35.87% YoY to USD 5.67/kg. The correction reflects the unwinding of the strong weather-risk premium that supported prices throughout 2025, as new crop expectations signal a substantial recovery in global supply.

The primary driver of the recent price decline has been Brazil’s improving production outlook. Brazil’s CONAB forecasts that the country’s 2026 coffee harvest could reach a record 66.2 million bags, representing a 17.2% YoY increase. Arabica production is expected to rise by 23.2% to 44.1 million bags, while robusta output may grow by 6.3% to 22.1 million bags. Favorable rainfall in Minas Gerais, Brazil’s largest arabica-producing region, has strengthened crop development and reduced concerns about drought-related yield losses. As the market increasingly prices in this larger harvest, Brazilian origin prices have moved lower, with Arabica declining 22.39% YoY to USD 7.51/kg and Robusta falling 45.16% YoY to USD 5.76/kg.

Additional downward pressure has come from Vietnam, the world’s largest robusta exporter. Vietnamese coffee prices declined 27.39% YoY to USD 5.18/kg as strong export performance and improving production prospects reinforced expectations of abundant robusta availability. Vietnam exported a record USD 8.6 billion worth of coffee in 2025, with output for the 2025/26 crop year forecast at approximately 31 million 60-kg bags. Together, Brazil and Vietnam account for more than 56% of global coffee production, meaning simultaneous supply growth in both origins has a significant bearish influence on international prices.

Coffee prices are likely to remain under short-term downward pressure as markets continue to absorb expectations of a large Brazilian harvest and expanding robusta supply from Vietnam. The recent price decline suggests that the market is transitioning from a weather-driven risk premium to a supply-driven equilibrium. However, the pace of further declines may slow as prices approach cost-support levels and as the market monitors weather conditions during Brazil’s key development stages. The near-term outlook for both arabica and robusta remains neutral to bearish, with supply recovery likely to cap sustained price rebounds unless unexpected weather disruptions emerge in major producing regions.

3. Strategic Recommendations

Adopt a Defensive and Opportunistic Procurement Strategy as Supply Recovery Pressures Coffee Prices

Global coffee prices remain under pressure as stronger supply expectations from Brazil and Vietnam reshape market dynamics. Arabica futures declined 0.51% WoW, while Robusta rose 1.34% WoW to USD 3.64/kg, though both remain near multi-month lows after a recent three-week correction. Brazil’s projected 17.2% YoY production increase to 66.2 million bags, expanding Vietnamese exports, and rising ICE inventories signal improving supply, supporting a neutral-to-bearish near-term outlook.

From a trade strategy perspective, procurement should emphasize flexibility and short-duration exposure. Arabica purchasing should be approached opportunistically, with buyers gradually rebuilding coverage during market dips rather than committing to large forward volumes. Although the broader trend remains soft, Arabica prices remain sensitive to weather volatility in Brazil, particularly during key crop development stages in Minas Gerais. Selective coverage during price corrections can therefore protect against potential supply shocks while maintaining cost efficiency.

Robusta's strategy should remain more defensive. Strong export growth and improving output from Vietnam suggest that the Robusta complex may face sustained supply pressure in the near term. Buyers should prioritize rolling short-term contracts and maintain light inventories to capture potential additional downside. Vietnamese origin remains the most competitive supply source for cost-efficient blends and processed coffee formats, supported by the country’s growing export capacity and expanding production base.

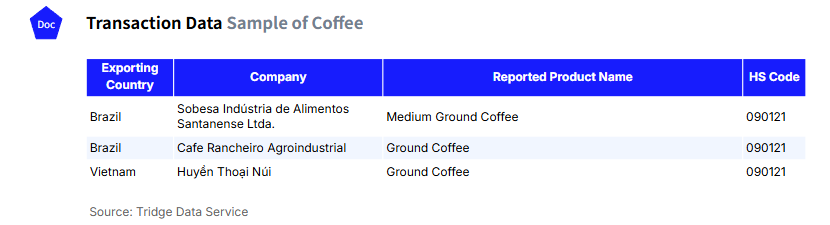

According to Tridge’s Eye transaction explorer data, export activity remains steady across key origins. In Brazil, companies such as Sobesa Indústria de Alimentos Santanense Ltda., and Cafe Rancheiro Agroindustrial continue to participate in international trade through shipments of medium ground and ground coffee. Vietnam also maintains active export flows, including transactions involving Huyền Thoại Núi for ground coffee. These commercial signals indicate continued availability of supply from major producing countries, reinforcing the case for tactical procurement rather than aggressive stock accumulation.

Over the next one to three months, the procurement strategy should remain disciplined and market-responsive. First, maintain light Robusta inventory coverage and prioritize Vietnamese supply contracts with flexible shipment terms to capture potential further price declines. Second, selectively secure Brazilian Arabica volumes during market dips to hedge against weather-related volatility while avoiding heavy forward commitments. Third, align sourcing strategies with product segmentation by prioritizing Brazilian Arabica for premium roasted products and Vietnamese Robusta for cost-efficient blends. Fourth, use limited short-term hedging through ICE futures to manage volatility while avoiding large speculative long positions until clearer signs of tightening supply or weather disruptions emerge.

Positioning should remain liquidity-focused and opportunistic, recognizing that the ongoing recovery in global coffee supply is likely to cap sustained price increases in the near term while creating favorable entry points for disciplined buyers.