Climate & Supply Volatility: Major Weather Events That Shaped the Agri-Food Trade In 2025

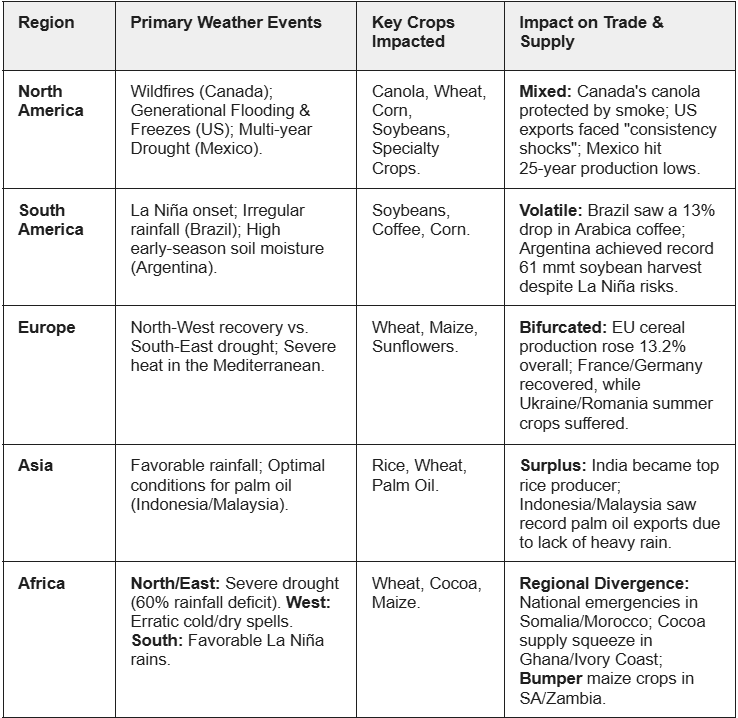

Table 1. Summary Table of Major Weather Events by Region

North America - From Wildfires in the North to Freezes in the South

In 2025, North American agriculture was defined by extreme volatility, ranging from historic atmospheric shifts to localized disasters. Canada grappled with an intense wildfire season where mid-summer smoke paradoxically shielded oilseeds from heat while hindering cereal development. Simultaneously, the United States (US) faced a staggering series of multi-billion-dollar events, including flooding in the Midwest and record-breaking freezes in the Gulf Coast. Meanwhile, Mexico struggled with a debilitating, multi-year drought that pushed grain production to a 25-year low.

Canada

In 2025, Canada’s agricultural sector was shaped by one of the most intense wildfire seasons in decades, particularly across the Prairie provinces and parts of Central Canada, driven by hotter and drier conditions. Persistent wildfire smoke became the defining mid-summer weather event, especially during Jul-25, when key crops such as canola, spring wheat, barley, and oats were in sensitive flowering and grain-setting stages. Western Canada experienced ongoing drought alongside the smoke, but the interaction between reduced sunlight and lower temperatures produced highly crop- and timing-specific outcomes.

Canola, Canada’s most important oilseed and export crop, was the clearest beneficiary of the Jul-25 smoke episode. Canada grows canola on roughly 21 million acres, making it the world’s largest producer. During flowering, temperatures above 31°C (87.8°F) can melt pollen and sharply reduce seed set. In several Prairie regions, smoke dimmed sunlight and lowered both daytime and nighttime temperatures, protecting flowers and pollen from heat stress. Farmers and crop analysts reported more pods per plant and more seeds per pod, helping offset drought stress. As a result, yield expectations for canola in parts of Western Canada were more resilient than initially feared earlier in the season.

Cereal crops such as spring wheat and barley experienced more uneven impacts. While cooler temperatures reduced heat stress, prolonged haze limited photosynthesis and slowed crop development in some areas, raising uncertainty around final yields and quality. Government researchers noted that smoke can degrade chlorophyll and reduce enzyme efficiency, suggesting that benefits seen in canola may not translate as clearly to cereals. Beyond field crops, smoky conditions also disrupted pollination activity, with beekeepers reporting reduced nectar collection as bees became less active, adding indirect pressure to honey production.

From an export supply perspective, the 2025 weather pattern produced mixed but manageable outcomes. Canola export availability remained relatively supported due to stable or improved yield expectations in key Prairie regions, helping sustain exports of canola seed, oil, and meal despite drought conditions. In contrast, wheat and barley exports faced greater uncertainty, as slower crop development and variable yield prospects increased risks to volume and quality consistency. While wildfire smoke is typically associated with negative agricultural impacts, its Jul-25 timing proved unusually supportive for canola, reinforcing Canada’s oilseed export position even as climate volatility continued to challenge cereal and specialty crop supply.

United States

During 2025, the US experienced an exceptional concentration of multi-billion-dollar extreme weather events that significantly disrupted agricultural production and export supply. Seven major disasters, led by flooding in the central US and Texas Hill Country, generated an estimated USD 378 to 424 billion in total damage and economic losses. A historic Gulf Coast winter storm in Jan-25 brought three consecutive days of ~24°F (-4°C) temperatures to parts of the Southeast, setting all-time snowfall records in cities such as New Orleans, Mobile, and Pensacola. The freeze damaged specialty crops, including strawberries in Alabama, Florida, and Georgia, and leafy greens (kale, collards, turnips, mustard), while also disrupting poultry operations and farm infrastructure. Farm-level losses were material, with individual producers reporting equipment and crop damage exceeding USD 17,000, reducing early-season fresh produce availability for domestic and export markets.

In Apr-25, the South and lower Midwest were hit by “generational” flooding, with over 12 inches of rain in some areas. Floodwaters affected roughly 31% of the nearly 840,000 acres planted by early Apr-25, and damages in Arkansas alone were conservatively estimated at USD 78.9 million. Key crops impacted included corn, soybeans, rice, and cotton, as submerged acreage, delayed fieldwork, and replanting needs constrained yield potential and tightened exportable surpluses later in the year. In Jun-25, the US recorded its first EF5 tornado since 2013, with winds exceeding 200 mph, causing localized but severe damage in North Dakota to grain bins, handling systems, irrigation, and power infrastructure, disrupting logistics for wheat and corn exports despite limited nationwide acreage losses.

Weather volatility intensified during the summer. From Jun-25, a widespread heat wave from the Rockies to New England set more than 3,000 daily temperature records, stressing corn and soybean crops during pollination and grain fill, increasing yield uncertainty and volatility in export supply forecasts. Furthermore, in Jul-25, torrential rainfall triggered catastrophic flash flooding in the Texas Hill Country, where river levels on the Guadalupe surged nearly 30 feet in six hours, peaking at a record 37.52 feet. The disaster caused at least 135 fatalities and USD 18 to 22 billion in estimated losses, with severe impacts on livestock, fencing, and farm structures, further constraining cattle and beef supply chains.

Despite the sector’s resilience, these shocks highlighted growing vulnerabilities in export reliability. Academic analysis indicates that a 1% increase in drought intensity in major producing states can lead to a 0.5–0.7% decline in domestic exports, with measurable downstream effects on food manufacturing. Overall, while US agriculture remained operational in 2025, the clustering of extreme events reduced consistency in grain, oilseed, livestock, and specialty crop exports, underscoring how increasingly frequent climate shocks are tightening margins and amplifying risk across US agricultural trade.

Mexico

Mexico’s 2025 agricultural sector was shaped primarily by persistent drought rather than acute, single weather shocks, with water stress emerging as the dominant climatic constraint across the Northern, Northwestern, and Central regions for a second consecutive year. Forecasts indicated that national grain and oilseed production fell to its lowest level in 25 years, reflecting limited rainfall, depleted reservoirs, and reduced surface water availability in key irrigated zones.

According to the Secretariat of Agriculture and Rural Development’s (SADER) 2025 Agrifood Outlook, corn production declined by 1.11% by year-end, with Sinaloa, Mexico’s leading corn-producing state, particularly affected by reduced irrigation water. Spring bean harvests in Zacatecas and Durango posted below-average yields for a second year, reinforcing pressure on staple grain supply. While localized improvements later in the year supported partial recovery in legumes, with Zacatecas producing over 350,000 mt, Durango 140,000 mt, and Chihuahua 80,000 mt, these gains did not fully offset earlier losses. In response, the government accelerated irrigation modernization, reporting 24% progress in key districts supplying Hidalgo and 76% completion in parts of Aguascalientes, alongside a national plan to recover 2.8 billion m³ of water through investments exceeding USD 3.65 billion (MXN 63 billion) between 2025 and 2030.

From an export supply perspective, drought-driven production shortfalls tightened availability of staple grains, increasing import dependence and limiting exportable surpluses. Weather stress also indirectly constrained export-oriented horticulture, as higher irrigation costs and water scarcity contributed to planted-area reductions of 18 to 25% YoY in Sinaloa, a state that generates around USD 3 billion annually in agricultural exports to the US, reinforcing Mexico’s heightened exposure to climate-driven supply risks in 2025.

South America - The La Niña Tug-of-War

Agricultural performance in South America throughout 2025 was dictated by the ebb and flow of La Niña. Brazil, the world’s leading soybean and coffee exporter, dealt with uneven precipitation that delayed planting across its primary soybean belt and caused a double-digit decline in arabica coffee output. In contrast, Argentina benefited from robust early-season soil moisture that buffered its record-breaking soybean crop against the typical dryness associated with La Niña.

Brazil

In 2025, Brazil’s agricultural sector was heavily shaped by La Niña–related weather volatility, with irregular rainfall emerging as the key driver affecting crop performance and export supply expectations for the 2025/26 season. Across the soybean belt, uneven precipitation disrupted planting between Oct-25 and Nov-25, particularly in Goiás, Mato Grosso, Minas Gerais, and Matopiba. Meanwhile, parts of Western Mato Grosso faced drought-related replanting needs, and Eastern Paraná experienced delays due to excessive rainfall. As of 23 November, soybean planting had reached 78% of the expected area, lagging 83.3% at the same point last year. These disruptions reduced yield potential and prompted forecast downgrades, with analysts cutting their estimate from 178.5 million metric tons (mmt) to 175 mmt, below the National Supply Company’s (Conab) 177.6 mmt forecast but still 3.6% above the 171.48 mmt harvested in 2024/25. Datagro also trimmed its outlook slightly to 182.9 mmt. Analysts flagged Goiás as a key risk area, where productivity is expected to fall from a record 4,190 kg/ha to around 3,900 kg/ha, while Rio Grande do Sul could partly offset losses with improved yields after last year’s poor harvest, despite forecasts of highly irregular rainfall through Dec-25. Overall, the tighter soybean outlook increased uncertainty around Brazil’s export availability later in the season, supporting global prices and raising market sensitivity to southern weather conditions.

Coffee production was also significantly affected in 2025. Brazil’s arabica crop suffered from drought, heat stress, and episodic cold fronts, including frost and hail risks, particularly in Minas Gerais, leading to a projected 13% YoY decline in arabica output for the 2025/26 harvest. Robusta performed more resiliently, but overall supply concerns remained elevated. Reflecting these risks, nearby coffee futures opened 2025 at USD 3.21 per pound (lb), reached a record high of USD 4.3797/lb on October 23, and were trading around USD 3.57/lb by December 30. Given Brazil’s position as the world’s largest exporter of soybeans and coffee, these weather-driven disruptions constrained export supply reliability in 2025, reinforcing Brazil’s growing exposure to climate variability and its increasing influence on global oilseed and soft-commodity markets.

Argentina

Argentina’s 2025 agricultural outlook was shaped primarily by the development of a La Niña weather event, which emerged as the dominant climate driver influencing crop performance and export supply expectations for the 2025/26 season. During the first half of 2025, above-average winter and early spring rainfall resulted in four consecutive months of above-average precipitation by end-October, leaving soils across core producing regions such as Buenos Aires, Santa Fe, and Entre Ríos unusually well supplied with moisture. In several areas, fields were described as closer to water excess than deficit, providing a favorable starting point for planting and partially buffering crops against the drier conditions typically associated with La Niña. However, as the season advanced into late spring and summer, rainfall became more variable, and temperatures increased, particularly between Nov-25 and Jan-26, when La Niña effects are expected to be strongest. Forecasts indicate the event will be weak and short-lived, with Nov-25 rainfall near 100–120 mm, followed by a slightly drier period through early January before conditions normalize later in the summer.

Soybeans and corn, Argentina’s two most important export-oriented crops, were the most exposed. Argentina is the world’s third-largest soybean producer, and La Niña conditions have historically been associated with negative yield deviations, especially for corn during the early part of the growing season when El Niño-Southern Oscillation (ENSO) impacts are strongest. Historical analogs show that during the strong La Niña year of 2011, corn yields finished at 558 kilograms (kg) per hectare (ha) below trend, and soybean yields 294 kg/ha below trend, highlighting the downside risk despite YoY variability. For 2025/26, the Rosario Grains Exchange (BCR) projects corn production at 47 mmt and a record soybean harvest of 61 mmt, supported initially by strong soil moisture but increasingly sensitive to mid-season dryness and heat. Wheat was less exposed due to its earlier harvest window, but the broader grain complex remained vulnerable to moisture stress during key reproductive stages. As a result, while early-season conditions reduced immediate downside risks, the emergence of La Niña during critical growth phases increased uncertainty around yields and reinforced volatility in export supply expectations for corn, soybeans, and downstream products such as soybean meal and oil heading into the 2025/26 marketing cycle.

Europe - Recovery in the North-West Offsets Droughts in the South-East

In 2025, the European Union’s (EU) agricultural landscape was defined by a stark geographical divide, with a robust recovery in Northern and Western Europe largely offsetting severe, heat-driven losses in the Mediterranean and Eastern regions, highlighting regional disparities. Nevertheless, aggregate cereal production for the EU rose by approximately 13.2% year-on-year (YoY) in 2025 to 290 mmt, following severe adverse weather conditions in 2024 which consisted of persistent rain in Western Europe which disrupted planting and reduced yields, while summer droughts in Southern and Eastern regions severely impacted crops like maize. For example, following a disastrously wet 2024, France staged a cereals production recovery, with wheat production surging by 28.6% to 34.6 mmt in 2025 due to favorable spring moisture and a dry harvest window. Similarly, Germany increased its wheat output by 25% to 23.2 mmt following similar weather issues to France in 2024, highlighting the recovery of production output in Western Europe in 2025.

In south-eastern Europe, hot and dry weather severely affected summer crops such as maize, sunflowers and soybeans. Persistent drought conditions in Romania, Bulgaria, Greece, and southern Ukraine caused irreversible yield damage in rainfed agriculture. Heat and rainfall deficit reduced yield expectations also in Hungary and eastern Croatia. Meanwhile, Romania and Bulgaria emerged as resilient contributors in eastern Europe, achieving record wheat harvests of 12.97 mmt (+40% YoY) and 7.12 mmt (+6% YoY) respectively. In Ukraine, one of the largest cereal and oilseed producers in Europe, although outside the EU, the season was marked by severe regional disparities. Persistent rainfall deficits in the eastern and southern oblasts severely impacted sunflower and maize harvests, while the west was hit by late spring frosts during the critical flowering stage for oilseeds. These factors combined with the ongoing war with Russia led to a 12.4% year-on-year decrease in total agricultural output.

Howden estimates that EU agriculture faces a USD 33.28 billion (EUR 28 billion) annual average loss from extreme weather, with this figure projected to reach USD USD 47.54 billion (EUR 40 billion) by 2050. Furthermore, only 20-30% of climate-related losses are insured, meaning that farmers shoulder 70-80% of all weather-related farm losses. In a separate but related finding, Inverto, part of Boston Consulting Group, found that the number of extreme weather events in Europe (including the UK) increased by 48% to 16,956 in 2023/24, up from 11,442 in 2021/22, highlighting the severity of disastrous weather related years such as 2024. Drought accounts for over 50% of total agricultural losses in the EU and poses the greatest threat across all EU regions. In conclusion, although on the balance of things Europe had good agricultural output in 2025, weather, especially drought, will continue to play a significant role in agricultural output in the years to come.

Asia - Bumper Harvests and Record Stocks

The 2025 agricultural narrative in Asia is one of overall positive news, with major crops such as rice and palm oil experiencing increased production. For example, India has overtaken China as the world’s largest rice producer, reaching 150.18 mmt in 2025 as compared to China’s 145.28 mmt. Furthermore, according to the USDA, wheat production in India is expected to rise to 117.9 mmt from 113 mmt in 2024. This can largely be attributed to favourable weather conditions and increased planted area in the case of rice production. Furthermore, according to the FAO, world rice stocks are forecast to increase by 2.2% to a new record high, largely due to increased output in Asia, pointing to favorable weather conditions.

The palm oil sector in Asia experienced similar conditions. In late 2025, Indonesia expected palm oil production to grow by 10% in 2025, reaching 56-57 mmt, exceeding previous forecasts, according to the Indonesian Palm Oil Association (GAPKI). This can largely be attributed to optimal weather in 2025, with no prolonged rainfall. As a result, Indonesia’s palm oil exports are expected to rise to 30-31 mmt, up from 29 mmt in 2024. Similarly, Malaysian palm oil production hit a record 20.28 mmt in 2025, largely due to favourable weather conditions combined with improved labour availability.

Russia, the world’s leading wheat exporter, faced localized weather issues, but experienced overall good weather conditions in 2025, leading to a significant grain yield. In a Dec-25 report, SovEcon, a leading consultancy specializing in Black Sea grain markets, raised its 2025 Russian wheat production forecast by 0.2 mmt to a total of 88.8 mmt. This upward revision was primarily driven by stronger-than-expected yields in Siberia, which helped offset earlier concerns regarding adverse weather. The consultancy also increased its barley estimate by 0.1 mmt to 19.4 mmt, while the corn forecast remained steady at 12.7 mmt. Together, these adjustments pushed the total grain production estimate to 136.2 mmt, an overall increase of 0.8 mmt from the previous month.

Africa - From Droughts in the North to Supply Recovery in the South

Africa’s 2025 agriculture season was characterized by climatic extremes, as can be expected of a continent of its size. The North and the Horn of Africa faced critical drought emergencies, with Morocco and Somalia declaring national crises as rainfall plummeted as much as 60% below average, forcing a heavy reliance on grain imports. In West Africa, the cocoa belt suffered from erratic weather and unseasonable cold, leading to a significant supply squeeze. However, Southern Africa saw a triumphant reversal of fortune. Favorable La Niña rains transformed the disastrous drought of 2024 into record-breaking maize harvests for South Africa and Zambia in 2025.

Northern Africa & The Maghreb

Northern Africa faced a critical year as persistent drought significantly hampered the 2025 cereal harvest. Morocco, in particular, saw cumulative rainfall during the 2025 growing season drop more than 60% below the long-term mean in key cereal producing regions. While late spring rains provided some moisture, they arrived too late to rescue the winter wheat and barley crops. As a result, Morocco’s cereal production for 2025 was estimated at roughly 4.5 mmt, about 13% below the national average. This shortfall has forced a heavy reliance on imports, with the country forecast to import 11 mmt of cereal in the 2025/26 marketing year to meet domestic demand. Similarly, in Libya, total cereal production is estimated at 160 thousand mt, about 20% below the five‑year average, largely driven by adverse weather conditions, which affected yields of winter cereals. In key producing regions of the northwest, heavy rainfall in Dec-24 caused floods and severely damaged crops. Similarly, in northeastern provinces of Al Fatah and Benghazi, early season floods affected crops in some areas. In contrast, Egypt saw more stable conditions due to continued investment in irrigation infrastructure, helping to cushion the wider regional impact. This helped Egypt to reach a record USD 11.5 billion in fresh and processed agriculture exports in 2025, highlighting the importance of investments in agricultural technology such as irrigation to help mitigate adverse weather conditions.

East Africa

The Horn of Africa experienced a severe drought crisis in 2025. Following the historic multi-year drought that ended in 2023, the region faced a renewed emergency as the 2025 short rains (Oct-25 to Dec-25) came in far below average across southern Somalia, eastern Kenya, and southeastern Ethiopia. Regions experienced between 30% and 60% less than their expected average rainfall during this period, resulting in one of the driest short-rains seasons on record.

This resulted in severe dry conditions and rainfall deficits across much of the region. Resultantly, in Nov-25, Somalia declared a national emergency following severe, countrywide drought conditions driven by an extremely poor Deyr rainfall season, which typically contributes over 40% of the nation’s annual cereal output. The drought has occurred during the main season and has affected the country’s breadbasket regions of Bay, Bakool, and Shabelle zones. Meanwhile, extreme mid-season rainfall led to localized flooding and crop damage, resulting in mixed harvest outcomes across the Kiremt/main season growing areas of Ethiopia, South Sudan, and Sudan. Conversely, favorable weather conditions in Western Ethiopia, Kenya’s North Rift, and Karamoja in Uganda have been recorded resulting in a generally above-average season. However, the overall regional output remained under pressure due to the severity of the drought conditions in the region.

West Africa

West Africa’s 2025 agricultural sector was dominated by the ongoing supply squeeze in the cocoa belt. Côte d'Ivoire and Ghana, the two largest cocoa producers, experienced overall adverse weather conditions in 2025. Ghana produced an output of 600 thousand mt in the 2024/25 season, up from 425 thousand mt in the 2023/24 season. The initial projection for the 2024/25 season was 800 thousand mt. However, a combination of erratic weather conditions and unregistered and unlicensed cross-border trade, shaved potentially as much as 200 thousand mt from the initial projection. Similarly, the USDA pegs Côte d'Ivoire’s cocoa production for 2024/25 at 1.75 mmt, nearly 3% off from the 2023/24 season. The production decrease is attributable to the impact of adverse weather conditions during the mid-crop (minor) season (Apr-25 Sep-25), which included a combination of prolonged dry spells with low rainfall and unseasonable cold weather. Industry experts predict a further 10% decrease in West African cocoa output for the 2025/26 season, which could spell significant price increases in 2026 for chocolate lovers globally.

Southern Africa

Southern Africa underwent a significant weather shift in late 2025. The region began 2025 reeling from one of its worst droughts in decades in 2024, which caused significant grain yield reductions across multiple countries in the region. For example, Zambia only harvested around 1.5 mmt of maize, far below its domestic consumption needs of 2.8 mmt, while Zimbabwe lost around 60% of its maize harvest. South Africa suffered a similar but less subdued fate and experienced a decline of roughly 22% in its 2024 harvest. Fortunately, the weather changed for the better in 2025. Zambia projected a maize production of 3.66 mmt, exceeding its annual domestic needs while South Africa experienced its second largest maize crop on record at 16.44 mmt, 28% above the disastrous output of 2024. In essence, the favourable La Niña-induced rains are the core factor behind the yield improvement across the region. These favourable weather conditions helped South Africa to increase its agricultural exports by 10% to a record high of USD 15.1 billion in 2025.

Oceania - A Region of Climatic Extremes

In 2025, Oceania’s agricultural output was shaped by sharp regional contrasts and the heavy influence of climate-driven volatility. Australia experienced a duality in weather patterns, where prolonged drought in the southern states slashed winter cereal and canola yields, while above-average rainfall in the north supported robust wheat production but complicated logistics through flooding. New Zealand similarly navigated a year of instability, as eastern droughts constrained irrigated dairy farms while intense rainfall episodes disrupted high-value horticultural exports. For both nations, the year underscored a shift where export reliability is increasingly dictated by quality constraints and transport resilience.

Australia

In 2025, Australia’s agricultural sector was defined by sharp regional contrasts in weather, with drought, flooding, heat extremes, and cyclonic rainfall directly shaping production outcomes and export supply reliability. Prolonged drought across South Australia, Victoria, parts of Western Australia, and southeastern sheep regions reduced yields and quality for winter cereals, canola, pulses, pasture, and horticulture. National winter crop production for 2025/26 is forecast at 54.5 mmt, a 9% decline YoY, with wheat output particularly constrained in drought-affected Southern states, where production is estimated at 4.2 mmt in South Australia and 4.0 mmt in Victoria, both below average. Canola production is forecast at 5.4 mmt, down 9% YoY, tightening exportable surplus and reducing 2025/26 export availability to around 4.5 mmt, compared with about 5.5 mmt in the prior season. In South Australia, drought-driven yield and quality losses in fresh potatoes caused visible retail shortages, with growers forced to source supply from Queensland and prices increasing to record levels, illustrating how specification failures rather than absolute absence can rapidly translate into commercial shortages.

By contrast, above-average rainfall and flooding across New South Wales and Queensland during summer and autumn significantly improved soil moisture and supported summer crop yields and winter sowing. New South Wales wheat production is tracking at 10.3 mmt, around 22% above the long-term average, while Queensland wheat output is forecast near its five-year average at 2.1 mmt. However, flooding damaged livestock, horticulture, and farm infrastructure, disrupting harvesting schedules and transport, and increasing variability in fruit and vegetable quality. These disruptions were compounded by heat stress later in the year, which elevated yield risk for cereals during flowering and grain fill in southern regions.

Australia’s export-heavy agricultural model, where over two-thirds of production is exported, magnified the impact of regional weather shocks in 2025. Reduced and more variable production in drought-affected southern regions constrained export supply of grains, oilseeds, sheepmeat, dairy, and selected vegetables, while stronger northern production partially offset volume losses but introduced greater logistical complexity and quality dispersion across export programs. This combination reinforced Australia’s growing exposure to climate-driven volatility, with export supply increasingly shaped by quality constraints and timing risks rather than headline production alone.

New Zealand

New Zealand’s 2025 agricultural sector faced heightened climate volatility, with alternating droughts, heavy rainfall, and flooding emerging as the defining weather events shaping production and export supply. Prolonged dry spells, particularly in parts of Canterbury and other Eastern regions, constrained pasture growth and reduced irrigation reliability, weighing on dairy, sheep, and beef systems. Irrigated dairy farms were especially exposed, as low river flows triggered water restrictions, limiting milk output and reducing exportable volumes of dairy products during peak production periods.

At the same time, episodes of intense rainfall and flooding disrupted farming and logistics in several regions, damaging horticultural crops such as kiwifruit, apples, and vegetables, and delaying harvests. These events also affected transport and port operations, causing short-term interruptions to exports of fresh produce and meat. More variable temperatures and soil moisture conditions increased pressure on pasture-based systems, raising feed costs and constraining livestock productivity.

The combination of water scarcity in key dairying regions and weather-related disruptions to horticulture and livestock systems reduced the reliability of New Zealand’s export supply in 2025. Dairy, meat, and horticultural exports remained structurally strong but were increasingly exposed to intra-year volatility, reinforcing the need for greater resilience in water management, land use, and supply chain planning to stabilise export performance under more extreme and unpredictable weather conditions.

Conclusion and Outlook for 2026

In conclusion, the agricultural narrative of 2025 serves as a powerful reminder that while the global food system remains resilient in the aggregate, it is characterized by regional fluctuations and instability. The resilience of global supply does not eliminate the friction caused by localized climatic shocks. Rather, it masks the severe challenges faced by specific regions in sourcing and exporting vital commodities. As seen from the Canadian prairies to the African Horn, a single weather event—be it a generational flood or a severe drought—can ripple through the global market, tightening margins and destabilizing trade routes even when total world volumes remain stable.

Looking toward 2026, the primary challenge for the agricultural sector will be navigating this environment of constant climatic friction. Success will depend on the dual strategy of geographic diversification and the rapid adoption of adaptive technologies. Innovations in precision irrigation, drought-resistant seed varieties, and real-time climate modeling are no longer just tools for efficiency, they are the essential buffers required to manage the mounting risks of a volatile atmosphere. By leveraging these advancements, the global agricultural community can move beyond reactive crisis management toward a model of proactive resilience, ensuring that regional disruptions no longer translate into global instability.