.jpg)

In W14 in the wheat landscape, some of the most relevant trends included:

- With stable domestic production and improved access to foreign currency, Algeria and Egypt are set to maintain wheat imports at 9.2 mmt and 13 mmt, respectively, in 2025/26. Russia and Ukraine remain key suppliers.

- With a target of 31 mmt, India has already procured over 1 mmt of wheat early in the 2025/26 season, backed by strong arrivals, state bonus incentives, and a record production forecast of 115.3 mmt.

- Ukraine's grain exports declined 5% YoY by late Mar-25, with wheat exports down to 13 mmt, well below the 16.2 mmt target due to logistical and supply chain constraints.

- Wheat prices in Russia and Ukraine were up YoY, but global prices face downward pressure from rising US stocks, crop quality concerns in France, and anticipated pre-harvest sales in Ukraine.

1. Weekly News

Algeria

Algeria's 2025/26 Wheat Imports Forecast at 9.2 MMT with Stable Domestic Production

According to the United States Department of Agriculture's (USDA) Foreign Agricultural Service (FAS) forecast, Algeria is expected to import around 9.2 million metric tons (mmt) of wheat in the 2025/26 season, maintaining the same level as the 2024/25 season due to stable domestic production. Russia continues to be the primary wheat supplier to Algeria, with Ukraine emerging as a significant source as well.

Egypt

Egypt's Wheat Imports and Production Outlook for 2025/26 Stable with Projected Increase in Domestic Harvest

Egypt expects to import 13 mmt of wheat in the 2025/26 marketing year (MY), maintaining the same level as the previous year. This stability is supported by the availability of foreign currency, enabling private companies to purchase larger volumes of milling wheat and increase wheat flour exports, according to the USDA FAS. Wheat production in 2025/26 is forecasted to grow by 1% year-on-year (YoY) to 9.3 mmt, driven by an increase in the harvested area to 1.43 million hectares (ha) from 1.4 million ha in the previous year. The rise in production is incentivized by higher procurement prices, encouraging farmers to expand their wheat areas. Total wheat consumption is expected to rise 1.5% YoY to 20.4 mmt in 2025/26, primarily due to population growth. The key suppliers of milling wheat to Egypt in recent years have been Russia, Ukraine, and the European Union (EU).

India

India Begins Wheat Procurement for 2025/26 Season with Strong Initial Purchases

The Indian government has begun wheat procurement for the 2025/26 marketing season, with over 1 mmt already purchased in the initial days, marking a significant increase compared to the previous year. Strong arrivals from states like Madhya Pradesh, Rajasthan, Uttar Pradesh, and Gujarat contributed to this early success. The government aims to reach a procurement target of 31 mmt, with states such as Punjab and Haryana expected to play a pivotal role. The agriculture ministry anticipates a record wheat production of 115.3 mmt in the 2024/25 season. Since the 2021/22 season, wheat procurement has steadily increased, driven by lessons learned from years when purchases were lower due to poor output. Madhya Pradesh and Rajasthan state governments have announced bonus payments to encourage farmers.

Ukraine

Ukraine's Wheat Exports Declined in 2024/25 Agricultural Season

During the initial months of the 2024/25 agricultural season, extending up to March 28, Ukraine's grain and leguminous crop exports saw a 5% YoY decline compared to the previous season, totaling 32.4 mmt, according to the State Customs Service of Ukraine. This drop was due to a 4% decrease in wheat exports, which amounted to 13 mmt. This figure fell short of the targeted 16.2 mmt set under a memorandum following the last harvest, reflecting a significant shortfall in wheat exports.

United States

US Projects Decreased Wheat Sowing Forecasts for 2025

The USDA's Prospective Plantings report revised its forecasts for United States (US) crop sowing areas. While analysts had anticipated that farmers would increase wheat acreage due to reduced soybean plantings, the USDA projected a 2% YoY decrease in total wheat sowing, dropping from 46.1 million acres in 2024 to 45.4 million acres, marking the second lowest level since 2019. Farmers will sow winter wheat on 33.3 million acres (0.6 million acres fewer than expected), spring wheat on 10 million acres (a 0.5 million acre reduction), and durum wheat on 2 million acres.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W14 2024 to W14 2025)

Russia

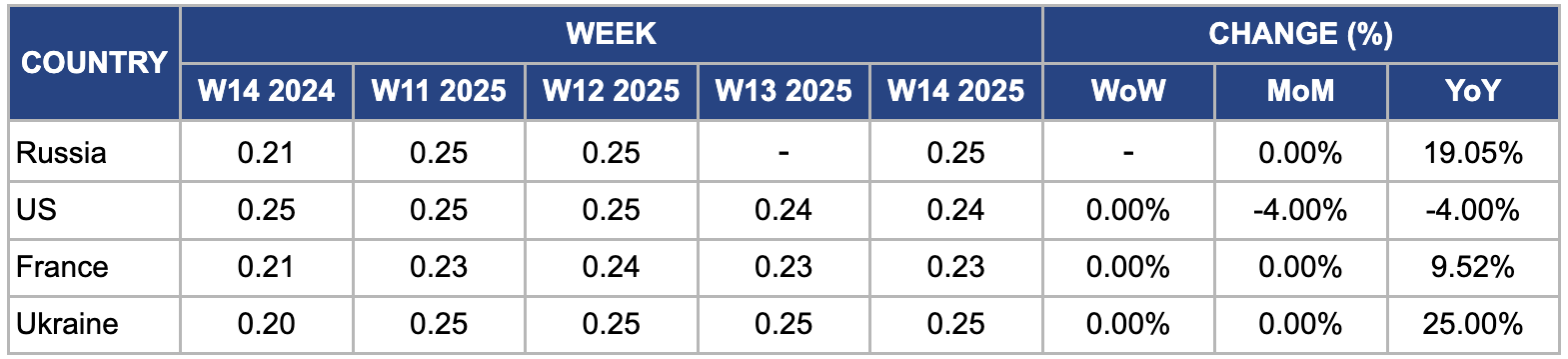

In W14, Russian free-on-board (FOB) wheat prices stood at USD 0.25 per kilogram (kg), marking a 19.05% YoY increase. Russia’s global wheat market share is forecasted to drop to 20% by the end of the 2024/25 agricultural season as lower harvests, reduced profitability for exporters, and strong yields from competitors weigh on performance. A quota limit, a strong ruble, and farmers' resistance to lowering prices will further influence export volumes. In Mar-25, Russia exported only 1.78 mmt of wheat, 2.9 times less than the previous year, according to the Russian Grain Union (RGU). Despite earlier forecasts, exports to 21 countries, including major buyers like Egypt, Bangladesh, and Sudan, also declined in volume.

United States

In W14, US FOB wheat prices averaged USD 0.24/kg, reflecting a 4% month-on-month (MoM) decline. This price drop is primarily due to increased market stock, with US wheat reserves rising by 14% YoY to 33.75 mmt as of Mar-25. Additional downward pressure on prices likely came from the US withdrawing from some export markets, thereby increasing domestic supply. Furthermore, improved weather conditions in key wheat-producing regions such as the Midwest and Kansas may have contributed to the price decline. Ongoing uncertainty about proposed US trade tariffs also pressured wheat prices, as traders remain cautious about future market developments.

France

In France, wholesale wheat prices in W14 averaged USD 0.23/kg, remaining stable week-on-week (WoW) but still 9.52% above the same period last year. This increase is partly due to crop quality concerns. According to FranceAgriMer, as of March 31, only 76% of winter soft wheat crops were in good or very good condition — better than 2024’s 65%, but still below levels in 2021 to 2023. Despite the mixed crop outlook, demand remains strong. French milling wheat exports from the Port of Rouen hit a 16-week high, reaching 87 thousand metric tons (mt) in the week ending March 26. This marked one of the highest weekly export volumes for 2024/25, with most shipments destined for Morocco and some to Portugal. However, French wheat experienced export challenges due to quality concerns and competition from Ukrainian and Russian supplies.

Ukraine

In W14, Ukraine’s FOB wheat prices averaged USD 0.25/kg, showing no change from the previous week or month but reflecting a 25% YoY increase. Despite this apparent stability, the price per mt has fluctuated slightly between USD 245/mt and USD 252/mt. The sustained high prices are likely driven by traders maintaining long positions, limiting available market supply. However, prices may decline in the coming weeks as traders increase sales in anticipation of the upcoming wheat harvest, potentially boosting supply in the market.

3. Actionable Recommendations

Diversify Import Sources Amid Supplier Shifts

Importers in Algeria and Egypt should diversify their wheat procurement portfolios to include emerging or stable suppliers such as Ukraine, EU-27, and potentially Argentina or Australia, especially as Russia's export volumes and share decline due to internal and policy constraints. This ensures supply chain stability, mitigates risks from overdependence on Russia, and potentially reduces procurement costs by capitalizing on competitive pricing from alternative suppliers.

Leverage Competitive Wheat Prices for Strategic Stockpiling

With FOB wheat prices from the US and France hovering at USD 0.23/kg, countries with foreign currency availability should consider strategic stockpiling of milling wheat during this price window, especially before new crop arrivals push prices upward. This helps save costs on bulk procurement, enhance food security, and hedge against potential price increases linked to weather uncertainties or policy changes.

Encourage Farmer Retention Through Targeted Incentives

Governments and private buyers should introduce or expand state-level bonus payments, input subsidies, or minimum support prices (MSPs) to maintain high production momentum, especially following India’s strong early procurement and record output expectations. This will sustain or boost domestic wheat supply, improve farmer income security, and support long-term export or food reserve goals.

Sources: Tridge, Agro Investor, Sinor, Ukr Agro Consult