In W17 in the tomato landscape, some of the most relevant trends included:

- India resumes tomato exports to Bangladesh from Kolar with restrictions. Despite lower export volumes, strong domestic demand has cushioned farmers from losses.

- Moroccan tomato exports to Norway hit a record high, increasing Morocco’s share in the Norwegian market.

- Nigeria suffers heavy post-harvest losses and remains the top tomato paste importer despite high production.

1. Weekly News

India

India’s Kolar Tomato Market Restarts Exports to Bangladesh Under New Restrictions

After nearly a year-long pause, Kolar, India, South Asia’s second-largest tomato trading hub, is resuming tomato exports to Bangladesh. This is with a strict condition that traders must not re-route the produce to Pakistan, which the Central government still bans exports. Authorities halted exports to Pakistan three years ago and suspended shipments to Nepal and Bangladesh about a year ago due to political unrest and rising local production. Seasonal shifts have boosted demand, prompting traders to restart exports to Bangladesh within a month. Although export volumes have dropped in 2025, strong domestic demand in India has protected farmers and traders from losses. Between June and October, Kolar typically dispatches 400 to 500 metric tons (mt) of tomatoes daily to destinations such as Dubai, Nepal, Afghanistan, Sri Lanka, Hong Kong, and Singapore.

Morocco

Morocco Sets Seasonal Tomato Export Record to Norway as Market Share Climbs to 29%

From Jul-24 to Mar-25, Morocco exported 5 thousand mt of tomatoes to Norway, marking a 37.9% year-on-year (YoY) increase and setting a seasonal record. This growth reflects Morocco’s rising significance in the Norwegian market, especially during winter when import demand peaks. Jan-25 alone saw a record monthly shipment of 1,150 mt. While Spain and the Netherlands still dominate with nearly 70% of Norway’s tomato imports, their volumes have declined, allowing Morocco’s market share to climb from 6% in 2019/20 to over 29% in the first nine months of 2024/25. Tomatoes remain Morocco’s top fruit and vegetable export by volume and value, with Norway emerging as an increasingly important market alongside traditional buyers like France, the United Kingdom (UK), and the Netherlands.

Nigeria

Nigeria Battles 45% Tomato Losses Despite Leading Africa in Production

Nigeria produces nearly 4 million metric tons (mmt) of tomatoes annually, making it Africa’s largest producer. However, it loses about 45%, or 1.8 mmt, of its harvest due to post-harvest losses and supply chain inefficiencies. According to the Agriculture Minister, poor infrastructure, weak farmer-processor linkages, and outdated farming methods drive these losses. Ironically, this has turned Nigeria into the world’s largest importer of tomato paste. The spread of the Tuta Absoluta pest, which can devastate entire crops if unmanaged, has further worsened the situation. In response, companies have launched initiatives like a tomato processing plant in Kebbi State, which can process 25 thousand mt annually. This investment aims to reduce waste, generate employment, and boost local value addition.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W17 2024 to W17 2025)

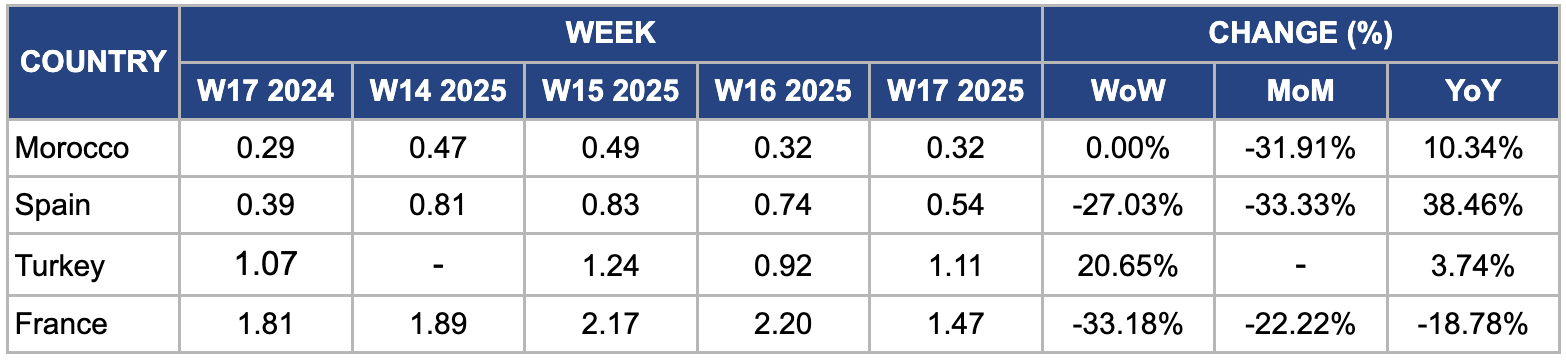

Morocco

In W17, Morocco's tomato prices fell sharply by 31.91% month-on-month (MoM) to USD 0.32 per kilogram (kg), driven by the government’s decision to implement strict export quotas that slashed daily tomato shipments to Europe by 90% for round and grape varieties. This move aimed to boost domestic availability and curb price inflation, particularly ahead of holidays, when food demand traditionally rises. As a result, a surge in local supply significantly pulled prices down, highlighting the immediate impact of policy interventions on market dynamics.

Spain

In W17, Spain's wholesale tomato prices dropped by 27.03% week-on-week (WoW) and 33.33% MoM to USD 0.54/kg, primarily due to increased production and improved supply chain efficiency, which led to market oversupply. Favorable weather conditions allowed for accelerated harvesting and higher yields, while expanded greenhouse operations in southern Spain boosted early-season volumes. Moreover, higher import volumes from Morocco and other non-EU suppliers intensified market competition. Consumer demand shifted toward alternative vegetables due to price sensitivity and seasonal eating habits, weakening tomato demand.

Türkiye

In W17 2025, Türkiye's wholesale tomato prices surged by 20.65% WoW, reaching USD 1.11/kg. This sharp increase is primarily due to factors impacting supply and demand dynamics. Firstly, adverse weather conditions, including unseasonal rainfall and temperature fluctuations, have disrupted the tomato harvest in key producing regions, leading to reduced supply in the domestic market. Moreover, the ongoing economic challenges in Türkiye, characterized by high inflation rates and currency depreciation, have increased production and transportation costs, further contributing to the rise in tomato prices. On the demand side, there has been a notable increase in export demand for Turkish tomatoes, particularly from neighboring countries facing supply shortages. This heightened export activity has.

France

In W17, France's wholesale tomato prices dropped sharply by 33.18% WoW, reaching USD 1.47/kg, down from USD 2.20/kg in W16. This significant decline is primarily due to a rapid increase in domestic supply due to peak spring production in key growing regions such as Provence-Alpes-Côte d’Azur and Brittany. Favorable weather conditions accelerated harvests, leading to a temporary glut in the market. Furthermore, reduced demand during the post-Easter period, combined with steady imports from neighboring EU countries like Spain and Morocco, added downward pressure on prices. The price correction reflects seasonal patterns common during periods of high output and reduced consumer buying momentum.

3. Actionable Recommendations

Diversify Export Markets to Reduce Dependency and Stabilize Prices

Tomato-exporting countries such as Morocco and Spain should actively diversify their export destinations beyond traditional European Union markets. Overreliance on EU demand has proven risky, especially when policy interventions like Morocco’s recent 90% export quota cut for tomatoes lead to sudden price collapses. By expanding into under-served markets in Eastern Europe, Central Asia, and Sub-Saharan Africa, exporters can reduce exposure to EU market fluctuations. For instance, Morocco’s growing presence in Norway demonstrates the potential of tapping into northern and non-traditional European markets. A broader geographic footprint will help stabilize export demand and pricing throughout the year, especially during oversupply periods.

Strengthen Post-Harvest Infrastructure to Cut Losses

Nigeria must urgently address post-harvest losses, which claim nearly 45% of national tomato production, equivalent to about 1.8 mmt annually. Investments in cold storage, ventilated transport, and rural collection centers are essential to preserving quality and extending shelf life. Introducing affordable plastic crates in place of traditional woven baskets and encouraging better harvesting practices can also reduce damage. These can be implemented through public-private partnerships, supported by incentives such as tax breaks or matching grants. Reducing post-harvest losses boosts marketable supply, supports farmer incomes, and decreases reliance on tomato paste imports, making Nigeria more self-sufficient.

Implement Dynamic Export Quota Systems

Moroccan governments managing volatile domestic food prices should adopt dynamic and data-driven export quota systems rather than abrupt or fixed restrictions. The sharp MoM drop in Morocco’s tomato prices following the sudden quota cut illustrates the unintended consequences of rigid policy tools. A more flexible system, calibrated using real-time domestic and export market data, can allow for gradual adjustments to export volumes in response to seasonal shifts or domestic inflation concerns. This would protect consumer interests without destabilizing farmgate prices or discouraging production.

Sources: Tridge, Fresh Plaza, News Central