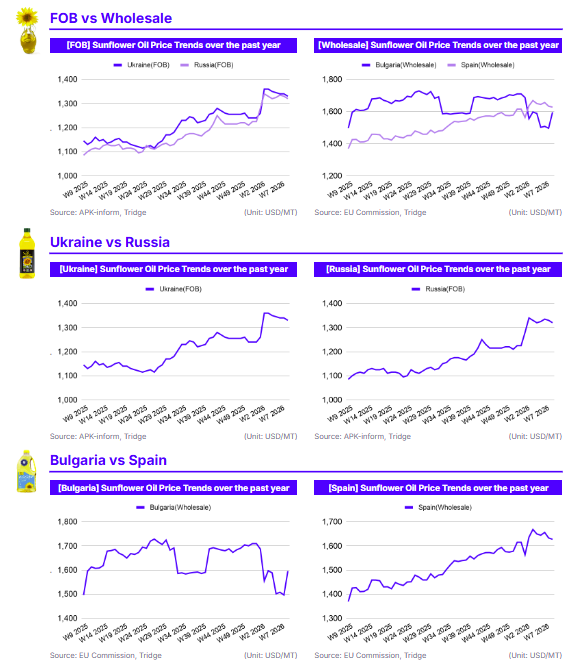

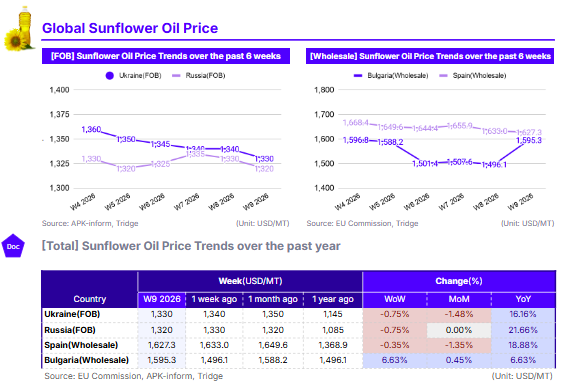

As of W9 2026, global sunflower oil prices remained high YoY due to anticipated record-low ending stocks for the 2025/26 season. Ukraine's FOB price was USD 1,330/mt (-0.75% WoW, +16.16% YoY), while Russia's FOB price hit USD 1,320/mt (-0.75% WoW, +21.66% YoY). EU wholesale markets saw Spain at USD 1,627.3/mt (-0.35% WoW, +18.88% YoY) and Bulgaria at USD 1,595.3/mt (+6.63% WoW, +6.63% YoY). The WoW price dips in Ukraine, Russia, and Spain were driven by increased supply and South American seed arrivals. However, Bulgaria’s WoW price spike was caused by pesticide residue issues in Argentine imports exceeding MRL limits. High YoY levels persist due to a 2025 production dip, with Spain 7.69% and Bulgaria 18.4% below the five-year average. Despite short-term volatility, Ukraine remains a cost-effective origin for European buyers, offering stable land-based logistics to mitigate maritime risks.

1. Weekly Price Overview

Pesticide Residue Concerns in Bulgarian Imports Cause Price Shock Amid Tight Global Stocks

In Ukraine, the Free on Board (FOB) price of sunflower oil was USD 1,330 per metric ton (mt) in W9, reflecting a 0.75% decrease week-on-week (WoW). This continued downward trend is primarily driven by increased supply reaching the market, further pressured by the arrival of South American sunflower seeds into the wider European market. Mirroring this movement, Russia’s FOB price also declined by 0.75% WoW to reach USD 1,320/mt. In Spain, wholesale prices reached USD 1,627.3/mt, down 0.35% WoW. The Spanish market remains highly sensitive to Ukrainian price signals, as approximately 41% of the European Union (EU) sunflower oil supply originates from Ukraine.

In contrast to the general softening of prices across the Black Sea and Spain, Bulgaria experienced a sharp 6.63% WoW increase, bringing prices to USD 1,595.3/mt. This volatility follows a brief price dip three weeks prior, which was triggered by the anticipation of importing 400 thousand mt of Argentine sunflower seeds. However, the recent WoW surge is likely the result of significant quality concerns, as the second shipment of Argentine seeds was found to contain pesticide residues exceeding the EU’s Maximum Residue Limits (MRL). This regulatory hurdle has restricted the immediate availability of these imports, forcing a price recovery to levels seen one month ago.

2. Price Analysis

Global Prices Remain Structurally Elevated Following 2025 Production Deficit

In Ukraine, the FOB price of sunflower oil reached USD 1,330/mt in W9, representing a 1.48% decline month-on-month (MoM) but maintaining a substantial 16.16% increase year-on-year (YoY). The MoM softening is a result of a consistent downward trend as higher supply enters the market, though the high YoY price is anchored by lower global supplies as evidenced by the United States Department of Agriculture (USDA) forecasting record-low global ending stocks for the 2025/26 season. Russia’s FOB price stood at USD 1,320/mt, remaining flat MoM while posting a significant 21.66% YoY increase. This annual surge mirrors the structural supply tightness seen in Ukraine, as Russian prices closely follow Ukrainian benchmarks amid a global deficit that continues to drive up long-term valuations.

In the EU, Spain’s wholesale price decreased 1.35% MoM to USD 1,627.3/mt, yet remains 18.88% higher YoY. Spain’s price movement closely tracks Ukraine’s because 41% of the oil in the EU originates from Ukraine. However, the elevated YoY price reflects a 2025 production dip that fell 7.69% below the five-year average. Bulgaria’s wholesale price reached USD 1,595.3/mt, up 0.45% MoM and 6.63% YoY. While the MoM increase was driven by recent regulatory hurdles regarding pesticide residues in Argentine imports, the 6.63% YoY increase, the lowest among the group, is rooted in a severe 2025 production drop of 18.4% below the five-year average.

3. Strategic Recommendations

Leverage Ukraine’s Cost-Competitive and Logistically Secure Supply to the EU

For European buyers seeking to mitigate the high domestic prices seen in markets like Spain (USD 1,627.3/mt) and Bulgaria (USD 1,595.3/mt), importing from Ukraine remains a strategically sound procurement option. In W9, Ukraine’s FOB price stood at USD 1,330/mt, offering a significant discount compared to EU wholesale levels. This cost advantage is particularly relevant as the market reacts to a consistent downward trend in Ukrainian prices due to supply availability. While global sunflower oil stocks are at record lows, Ukraine’s competitive pricing provides a vital buffer for European refiners and food manufacturers facing a year-on-year (YoY) price increase of nearly 19% in Spain.

Furthermore, Ukraine offers a distinct logistical advantage for the European market through established land-based corridors. While maritime exports in the Black Sea remain subject to geopolitical volatility and fluctuating insurance premiums, the Solidarity Lanes and rail-to-road infrastructure provide a relatively secure and continuous flow of sunflower oil into neighboring European countries. Given that 41% of the oil in the EU already originates from Ukraine, buyers should prioritize strengthening direct contracts with Ukrainian crushers to ensure supply continuity. This land-based security is essential for managing the risk of sudden maritime disruptions. By leveraging Ukraine’s price-competitive exports and stable land logistics, EU importers can better navigate the structural supply tightness currently defining the early-2026 global market.