1. Weekly News

Argentina

Argentina's 2024/25 Corn Season Faces Major Setback with Sharp Decline in Planted Area

The 2024/25 corn season in Argentina faces significant challenges compared to last year, with only 930 thousand hectares (ha) of early-planted corn expected, a sharp decline from the nearly 2 million ha planted in the previous year. This year, 30% of the intended area remains unplanted, and with the planting window closed, corn production in the core region is forecasted to be 52% lower than last year if no significant late plantings occur. This would make the 2024/25 season the third lowest corn planting area in the past decade.

Brazil

Paraná's 2024/25 First-Crop Corn Progress

For the 2024/25 harvest in Paraná, first-crop corn planting advanced, with 99% of the expected area now planted as of W45, a 3% increase from W44, according to the latest Department of Rural Economy (DERAL) report. Of the cultivated crops, 48% are in vegetative development, and 45% have entered the flowering phase. Regular rainfall and mild temperatures in some regions have contributed to the corn's good performance.

Mato Grosso Corn Exports in 2024 See Major Shift Toward Northern Ports

From Jan-24 to Sep-24, Mato Grosso exported 16.89 million metric tons (mmt) of corn, with 10.28 mmt or 60.8% of the total flowing through ports in Northern Brazil and 39.1% exported through southern ports. In 2021, 47.6% of Mato Grosso’s corn exports flowed through the northern ports. The two main northern ports for corn exports from Mato Grosso are Barcarena at the mouth of the Amazon River and the upriver port of Santarem. The Mato Grosso Institute of Agricultural Economics (IMEA) indicated that these two ports exported 8.65 mmt of corn from Jan-24 to Sep-24 or 84.1% of the total.

Russia

Russia's 2024 Corn Harvest Expected to Drop by 25%

Russia's 2024 corn harvest, excluding the territories of Donbas and Novorossiya, is expected to reach around 12.2 to 12.3 mmt, nearly 25% lower than the 16.6 mmt harvested in 2023. This forecast highlights corn as the crop with the most significant decline. The drop in yield is mainly due to the drought in the southern regions, particularly the Southern Black Earth Region, which significantly impacted corn production.

Ukraine

Corn Harvest Progress in Ukraine Shows Strong Regional Yields

According to the Ministry of Agrarian Policy, Ukraine's corn harvest has reached 18.29 mmt from 75.9% of the sown areas as of W45, with an average yield of 59.5 metric tons (mt) per ha, down from 2023’s total of 31 mmt and yield of 78.1 mt/ha,. Leading regional harvests, Poltava Oblast has produced 2.566 mmt, followed by Chernihiv with 2.517 mmt, and Cherkasy with 2.134 mmt. Additionally, five other regions have recorded over 1 mmt each: Kyiv with 1.433 mmt, Sumy with 1.406 mmt from 71.3% of its area, Vinnytsia with 1.387 mmt, Kirovohrad with 1.064 mmt, and Khmelnytskyi with 1.055 mmt.

United States

USDA Revises 2024/25 Corn Production Forecast in The US

According to the United States Department of Agriculture (USDA) Nov-24 estimate, the United States (US) corn production forecast for the 2024/25 season has been reduced from 386.16 mmt to 385.55 mmt. Productivity has decreased slightly from 11.54 to 11.53 mt/ha.

2. Weekly Pricing

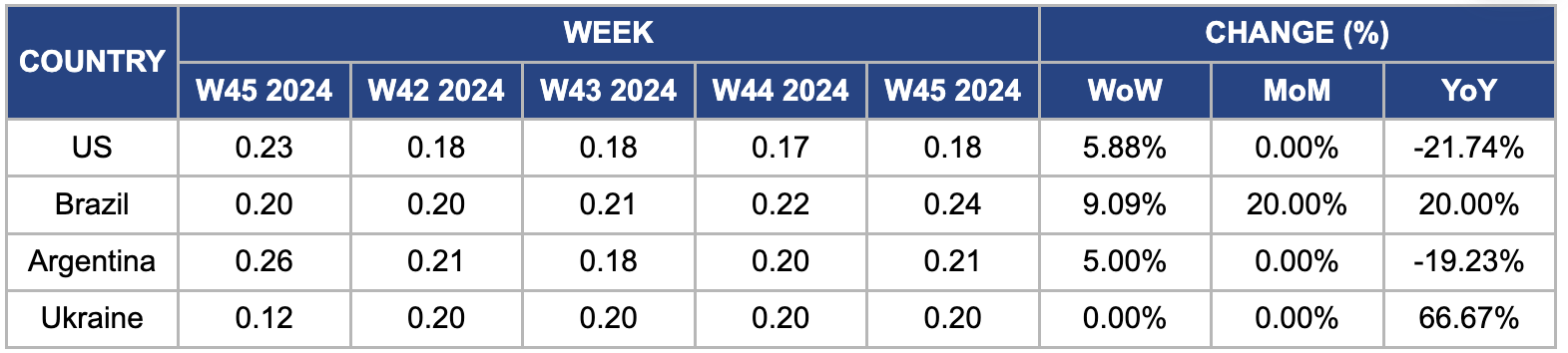

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W45 2023 to W45 2024)

United States

In W45, wholesale maize prices in the US rose by 5.88% week-on-week (WoW) and 21.74% year-on-year (YoY), reaching USD 0.18 per kilogram (kg). This price increase followed the USDA's reduction in its 2024/25 corn estimate, with the production forecast revised from 386.16 mmt to 385.55 mmt and productivity slightly decreasing from 11.54 to 11.53 mt/ha. Despite this adjustment, the US corn crop was harvested from 91% of the sown areas by November 3, ahead of the average pace, according to the National Agricultural Statistics Service (NASS).

Brazil

In W45, wholesale maize prices in Brazil rose by 9.09% WoW, 20% month-on-month (MoM), and 20% YoY, reaching USD 0.24/kg. This price surge is due to delays in corn planting caused by adverse weather, including drought, which has significantly reduced supply and led to variable productivity depending on rainfall. Moreover, the total acreage for the first corn crop is estimated at 9.26 million acres, reflecting a 6% YoY decrease, with a production estimate of 23 mmt, down 2% YoY. Conversely, the safrinha (second crop) corn acreage is projected to cover 39.19 million acres, a 2% decrease, with production expected to reach 100 mmt.

Argentina

In W45, the wholesale price of Argentine corn increased by 5% WoW, reaching USD 0.21/kg . This price rise is due to a severe corn leafhopper outbreak during the 2023/24 season, which led to a 30% reduction in corn planting for the upcoming season. Despite improved weather conditions, farmers have reduced their planting in the first phase of the current season. While the number of traps with no insects has increased, particularly outside of Northeastern Argentina, the impact on late-planted corn acreage and crop rotation decisions remain uncertain. However, the price dropped by 19.23% YoY. Recent rainfall in Argentina has benefited crop growth in Northeastern La Pampa and Central Buenos Aires, with more rain expected in East and Central Buenos Aires. While the rain has supported newly planted crops, it has not fully restored soil moisture. Corn planting is progressing, with 34.5% of planting completed and core areas 70 to 75% planted.

Ukraine

Ukrainian wholesale maize prices held steady WoW at USD 0.20/kg in W45, reflecting a substantial 66.67% YoY increase from USD 0.12/kg in 2023. The Ukrainian Agrarian Council (UAC) revised the USDA's forecast for Ukraine's corn harvest downward by 1 mmt to 26.2 mmt due to dry weather conditions, contributing to the price surge. Challenges persist as the country’s reliance on deep-sea ports has led to a 13% YoY decline in the once-significant export route through Constanta.

3. Actionable Recommendations

Enhance Irrigation and Water Management

To mitigate the effects of water scarcity in Argentina, farmers should invest in drought-resistant corn varieties such as Pioneer P3520, Dekalb DKB390, Syngenta NK6030, Monsanto's DEKALB DKC70-10, and SmartStax® Drought Tolerant Corn. These varieties are bred specifically to optimize water usage, enhance root development, and maintain stable yields under dry conditions. Farmers can reduce their reliance on irrigation by adopting these drought-tolerant hybrids while ensuring better crop resilience and productivity during dry spells. When paired with efficient water management practices like drip irrigation, which minimizes water waste by delivering water directly to the plant roots, these measures can significantly improve water use efficiency and stabilize maize production, reducing price volatility.

Expand Export Routes in Ukraine

Ukraine should diversify its export routes by strengthening trade relationships with neighboring countries such as Poland, Romania, and Hungary. By enhancing rail and road transport links and improving river port infrastructure, Ukraine can bypass the blockages in the Black Sea and access alternative ports. This would provide a more stable and efficient logistics network, allowing Ukrainian maize to reach global markets despite the disruptions. Diversifying export routes reduces dependency on a few key ports, ensuring consistent and competitive maize exports and helping Ukraine maintain its position as a key global supplier.

Invest in Crop Protection and Pest Management

Brazil should take a proactive approach by investing in integrated pest management (IPM) strategies to minimize the risk of infestations. This could include better monitoring systems to detect early signs of pest problems and using organic pesticides to reduce crop damage. Ensuring a balanced approach to pest control, alongside improved crop rotation practices, would help maintain the stability of Brazil’s corn production and mitigate the price surges driven by supply disruptions. This would ensure consistent yields and contribute to the country's food security and export potential.

Sources: Agrotimes, UkrAgroConsult, PortalDBO, CanalRural, Pig 333, Milknews