In W6 in the soybean oil landscape, some of the most relevant trends included:

- Bangladesh is experiencing soybean oil shortages despite higher imports, causing price hikes and supply imbalances ahead of Ramadan.

- Prices fluctuate in Bangladesh, Brazil, and the Netherlands due to varying supply and demand factors, such as strong domestic demand and market distortions.

- Record soybean production in Brazil and Argentina has boosted global supply, but weak demand in sectors like European biodiesel has led to downward price pressure, particularly in the Netherlands.

- The US soybean oil market faces pressure from increased competition and trade tensions. Meanwhile Nepal’s soybean oil exports surge due to tariff differences with India.

1. Weekly News

Bangladesh

Bangladesh Grapples with Bottled Soybean Oil Shortage Despite Rising Imports

Bangladesh is facing a shortage of bottled soybean oil, with consumers struggling to find supplies in major markets. Despite a 69% year-on-year (YoY) increase in crude soybean oil imports, bottled oil remains scarce due to supply chain delays, trader hoarding, and ineffective policy interventions, leading to higher prices and market distortions. Loose soybean oil prices have also surged as traders capitalize on demand. The government has reduced import duties and called for meetings with suppliers to address the crisis. Meanwhile, global soybean oil prices have declined, highlighting a disparity between international trends and local market conditions. Experts warn that if the shortage persists, it could worsen ahead of Ramadan.

Bangladesh Faces Soybean Oil Shortage and Price Hikes Due to Political Instability and Financial Crisis

Since the government was overthrown in Aug-24, Bangladesh has experienced market instability and high inflation, leading to a shortage of cooking oils, including soybean oil. This has resulted in price hikes for both branded and non-branded oils. The interim government reduced value added tax (VAT) to stabilize prices, but supply chains have been affected, especially after local refiners' requests for price hikes were denied. Ahead of Ramadan, strategic pricing by producers has led to higher soybean oil prices, with bottled oil reaching USD 1.44 to 1.45 per liter (BDT 175 to 176/L) and loose oil increasing by 4%. The country's financial crisis has been exacerbated by the suspension of foreign aid, including from the US and Switzerland.

India

India's Soybean Oil Imports Increase as Palm Oil Demand Declines

In Jan-25, India reduced its edible oil imports by 16% to 1 million metric tons (mmt), with a notable 46% drop in palm oil imports. However, soybean oil imports rose by 4%, reaching a seven-month high of 438,000 metric tons (mt). This shift is attributed to higher palm oil prices, which have made it less competitive compared to soybean and sunflower oils. Despite a reduction in palm oil imports, soybean oil and sunflower oil saw increased demand from India, influencing global market prices.

Nepal

Nepal's Soybean Oil Exports to India Surge Due to Tariff Arbitrage, Raising Sustainability Concerns

Nepal's soybean oil exports to India have surged 45-fold in the first half of the fiscal year (FY), despite minimal domestic soybean production. This growth is driven by traders exploiting tariff differentials, as Nepal refines imported crude soybean oil and exports it duty-free under the India-Nepal Trade Treaty. India's past tariff adjustments led to sharp declines in Nepal's exports, but the reinstatement of a 20% customs duty in Sep-23 revived the trade. Experts warn that such arbitrage-driven exports are unsustainable and do not contribute to Nepal's long-term economic stability. Future shifts in India's import policies could significantly impact this trade.

Surge in Refined Soybean Oil Exports Through Nepal's Birgunj Checkpoint in the First Half of FY 2025

Exports of refined soybean oil through Nepal's Birgunj checkpoint have significantly increased in the first half of the current fiscal year (FY). A total of 560.66 million L of refined soybean oil, valued at USD 138.12 million (INR 11.99 billion), were exported, marking a sharp rise from 111.11 million L worth USD 1.27 million (INR 111 million) during the same period last year. The growth in soybean oil exports reflects improved trade with India.

United States

US Soybean Farmers Face Market Uncertainty Due to Trade Pressures and Policy Shifts

The American Soybean Association (ASA) warns that growing efforts to discredit seed oils, including claims that soybean oil is harmful, could significantly impact United States (US) soybean farmers. The ASA Chairman emphasized that domestic soybean oil markets provide stability, and restrictions on its use could lead to price declines at a time when the industry is still recovering from the 2018 trade war with China. The sector also faces intensified competition from Brazil, which expanded production following Chinese tariffs on US soybeans.

Additionally, potential new tariffs on Canadian imports could raise fertilizer costs, further straining farmers. With a strong US soy harvest coinciding with record production in Brazil and Argentina, the economic slowdown in China and its shift toward Brazilian soy add further pressure. Industry leaders also expressed concerns over tariff-driven supply chain disruptions, funding freezes affecting agricultural programs, and the need for a new farm bill to provide stability amid declining crop prices and rising input costs.

2. Weekly Pricing

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W6 2024 to W6 2025)

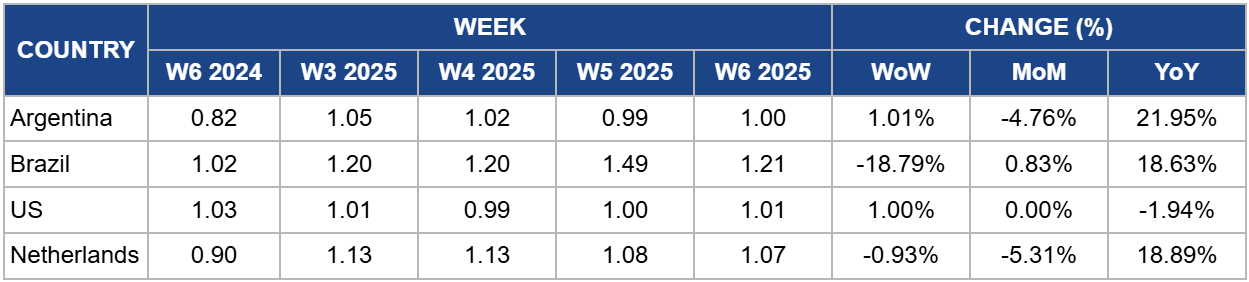

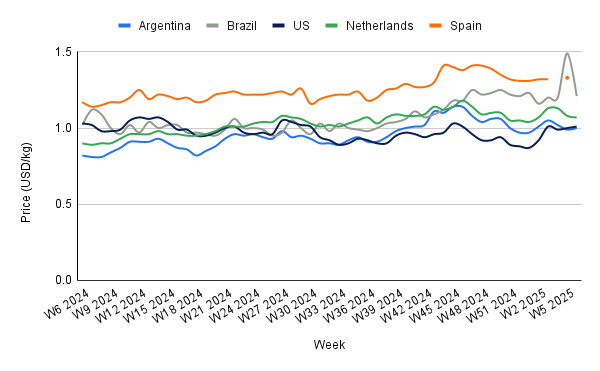

Argentina

Argentina's soybean oil prices have risen to USD 1 per kilogram (kg) in W6, reflecting a 1.01% week-on-week (WoW) increase, and a decrease of 4.76% month-on-month (MoM). This price surge is supported by record-breaking soybean processing levels in Dec-24, which reached 3.65 mmt, indicating strong industry activity. From Apr-24 to Dec-24, the total processed soybeans hit 34.75 mt, matching the record set during the 2014/15 season.

The increase in soybean oil prices can be attributed to the significant rise in soybean oil and meal exports, driven by robust external demand. Argentina's soybean oil exports reached historically high levels, surpassing only the 2006/07 campaign in terms of total volume. This high demand for derivatives, especially soybean oil, has kept processing rates at a peak.

The continuation of this trend into 2025 suggests that soybean oil prices will likely remain elevated due to sustained export demand and the ongoing processing boom.

The increase in soybean imports—accounting for 17% of total processed soybeans—also indicates a reliance on foreign supply to maintain output levels.The global demand for oils, combined with Argentina's strong processing capacity, indicates that soybean oil prices are likely to stay elevated, potentially influencing future pricing trends in international markets.

Brazil

In W6, Brazil's soybean oil prices have decreased to USD 1.21/kg, reflecting an 18.79% WoW drop, though they have risen 18.63% YoY. This price decline can be attributed to strong demand for biodiesel production, which is driving increased soybean crushing in Brazil. The country's soybean crush is expected to reach a record 57.10 mmt in 2025, up from 55 mmt in 2024, supported by a projected record soybean harvest of 171.7 mmt.

This crushing activity surge and soybean supply could increase soybean oil production, potentially putting downward pressure on prices in the short term. However, as biodiesel demand remains robust and soybean crushing intensifies, long-term price dynamics may be influenced by competing needs for soybeans, particularly in biodiesel production versus edible oil markets.

United States

US soybean oil prices rose to USD 1.01/kg in W6, marking a 1% weekly increase but a 1.94% decrease compared to the previous year. This price movement comes as ASA warns of potential risks to the market. Efforts to discredit seed oils, including claims about soybean oil's health impacts, could undermine demand, leading to future price declines. ASA highlights that such developments, combined with domestic and international market pressures, could disrupt the US soybean oil industry, which is still recovering from the 2018 trade war with China.

The rise of Brazil's soybean production and potential new tariffs on Canadian imports could exacerbate the strain on US farmers, affecting soybean oil production costs. Additionally, concerns over potential trade disruptions and rising input costs, such as fertilizers, may put further pressure on prices. With competition from Brazil and Argentina, coupled with a slowdown in China's economy, future soybean oil prices could face volatility, depending on trade dynamics and regulatory changes.

Netherlands

In W6, soybean oil prices in the Netherlands decreased to USD 1.07/kg, marking a 0.93% weekly decline and an 18.89% increase YoY. This drop is primarily driven by increased global supply and weakened demand from key sectors. Brazil's record soybean production, expected to reach 171.7 mmt in 2024/25, has significantly boosted global soybean oil availability, with exports projected to reach 106.1 mmt. Additionally, Argentina's temporary reduction in export taxes on soybeans and derivatives has further enhanced supply.

On the demand side, the European biodiesel producers, which are major soybean oil buyers, have encountered challenges due to feedstock limitations and high biodiesel prices, which have dampened demand. This combination of abundant supply and reduced demand has placed downward pressure on soybean oil prices in the Netherlands. Looking ahead, if global supply continues to outpace demand, prices may remain under pressure in the short to medium term, especially if production in Brazil and Argentina continues at high levels and European demand does not recover.

3. Actionable Recommendations

Stabilize Supply Chains

To address the ongoing soybean oil shortages, the Bangladesh government should further collaborate with local refiners and global suppliers to streamline imports and ensure consistent supply. Measures like temporarily relaxing trade barriers or subsidies for local producers could help ease bottlenecks, especially ahead of high-demand periods like Ramadan.

Enhance Trade Relations and Export Strategies

In markets like Nepal, where soybean oil exports have surged due to tariff differentials, it is crucial to work on long-term trade agreements with neighboring countries to ensure sustainable growth. Nepal could explore diversifying its market base while ensuring stability in trade with India by securing preferential tariffs or aligning with global soybean oil demand trends.

Focus on Diversified Domestic Demand

As global soybean oil markets face price fluctuations due to biodiesel demand and other market forces, producers and distributors should diversify their product lines and cater to both edible oil and biofuel industries. By balancing production for both sectors, businesses can shield themselves from extreme price volatility while tapping into growing demand for biodiesel in markets like Brazil.

Sources: Tridge, AgFunderNews, The Kathmandu Post, The Daily Prothom Alo, Grain Trade, OpIndia, My Republica, 3tres3