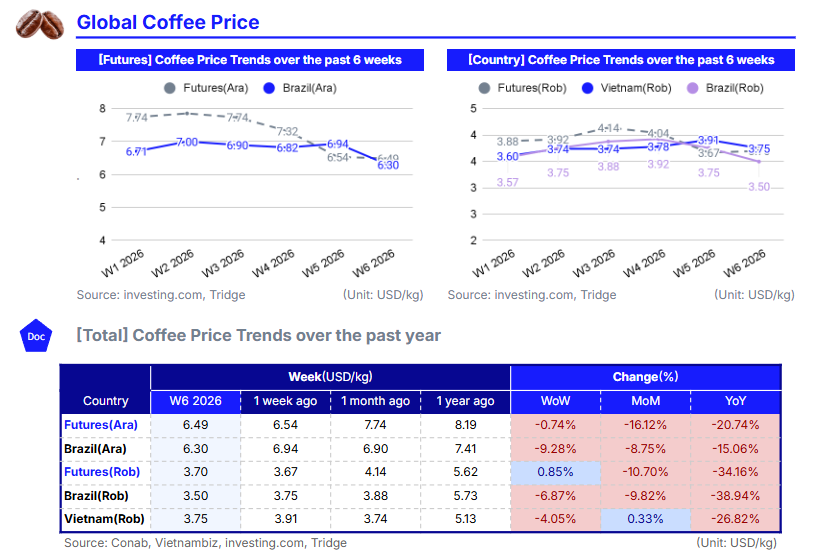

In W6 2026, global coffee prices continued to correct as improved crop conditions in Brazil and strong export momentum from Vietnam reinforced expectations of ample supply. Arabica futures declined 16.12% MoM and 20.74% YoY, while Robusta fell 8.75% MoM and 15.06% YoY, reflecting a shift from weather-risk premium to supply-driven repricing. Brazil’s projected 17.2% YoY increase in 2026 production and above-average rainfall in Minas Gerais have reduced crop stress concerns, while Vietnam’s 38.3% YoY surge in January exports and projected 6% output growth confirm expanding robusta availability. Rebuilding ICE inventories further weakens the scarcity narrative that supported 2025 highs, keeping both benchmarks under pressure, particularly Robusta, where structural acreage expansion in Brazil caps upside potential.

For a global food manufacturer sourcing Brazilian Arabica for roasted products and Vietnamese Robusta for blends, the core strategy should focus on defensive, short-duration procurement aligned with supply normalization. Arabica volumes should be secured selectively on price dips for near- to mid-term shipment windows to hedge against potential weather volatility, while avoiding heavy forward exposure. Robusta procurement should remain rolling and flexible, prioritizing Vietnamese origin to capture the continued downside linked to export expansion and structural supply growth.

Positioning should emphasize liquidity, staggered coverage, and limited speculative exposure. In a market transitioning from risk premium to supply adequacy, disciplined short-term sourcing and tactical hedging provide greater advantage than aggressive long positioning.

1. Weekly Price Overview

Coffee Prices Extend Decline as Improved Brazil Weather and Rising Vietnam Exports Reinforce Global Supply Outlook

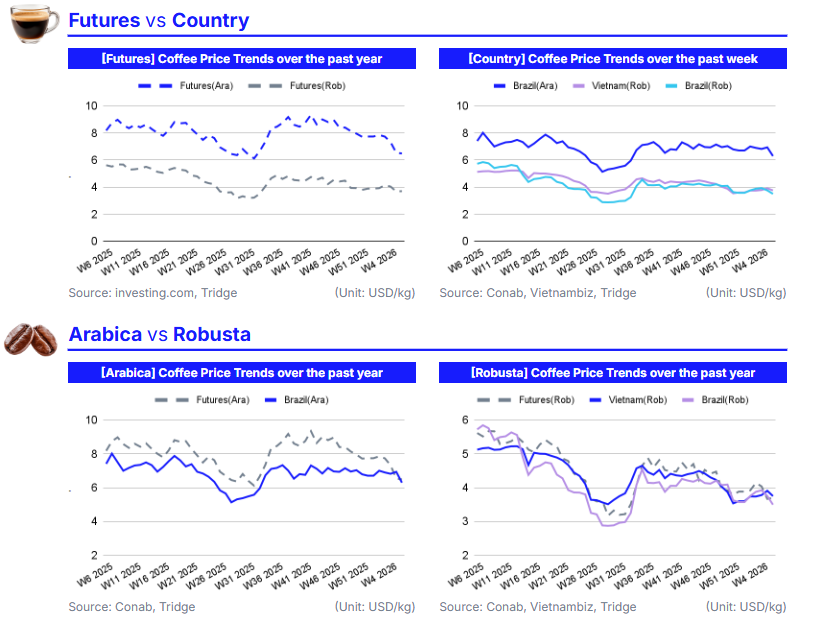

In W6 2026, global coffee prices remained under pressure for a third consecutive week as improving crop prospects and rising export flows reinforced expectations of ample supply. The international Arabica benchmark, represented by US Coffee C Futures, declined 0.74% week-on-week (WoW) to USD 6.49 per kilogram (kg), marking its lowest level in over seven months. Meanwhile, Robusta, represented by London Coffee Futures, rose 0.85% WoW to USD 3.70/kg but remains near a six-month low. The broader downward trend over the past two weeks reflects easing weather concerns in Brazil and confirmation of strong global production outlooks.

According to the USDA’s Foreign Agricultural Service (FAS) biannual report released on December 18, global coffee production for 2025/26 is projected to rise 2.0% year-on-year (YoY) to a record 178.848 million bags. While arabica output is forecast to decline 4.7% to 95.515 million bags, robusta production is expected to increase 10.9% to 83.333 million bags. Brazil’s total coffee production is projected at 63 million bags, down 3.1% YoY, whereas Vietnam’s output is forecast to rise 6.2% YoY to 30.8 million bags, a four-year high. Although global ending stocks are expected to fall 5.4% to 20.148 million bags, near-term market sentiment has been dominated by improving harvest conditions rather than stock tightening.

In Brazil, Arabica prices fell 9.28% WoW to USD 6.30/kg, and Robusta declined 6.87% WoW to USD 3.50/kg. Price weakness accelerated after Somar Meteorologia reported that Minas Gerais received 72.6 millimeters (mm) of rainfall in W6, equivalent to 113% of the historical average, easing earlier drought concerns and improving crop development prospects.

In Vietnam, domestic coffee prices decreased 4.05% WoW to USD 3.75/kg. The bearish tone was reinforced by strong export data from the National Statistics Office, which reported that Jan-26 coffee exports surged 38.3% YoY to 198,000 metric tons (mt), while cumulative 2025 exports rose 17.5% YoY to 1.58 million metric tons (mmt). Vietnam’s 2025/26 production is projected to increase 6% YoY to 1.76 million metric tons, or 29.4 million bags, further supporting robusta supply expectations.

Coffee prices over the past two weeks have been driven by improved weather in Brazil and expanding robusta availability from Vietnam, shifting market sentiment toward supply adequacy despite slightly lower projected global ending stocks.

2. Price Analysis

Coffee Futures Slide as Brazil’s Expanding Output and Vietnam’s Strong Exports Shift Market into Supply-Driven Correction

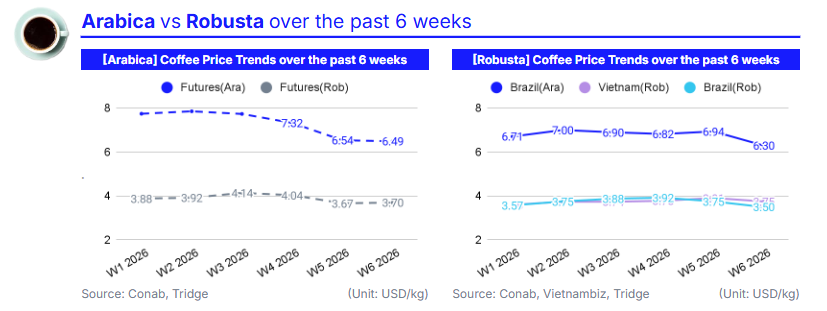

As of W6 2026, coffee futures are undergoing a broad correction driven by a rapid shift from supply-risk pricing to supply-normalization expectations. Arabica declined 16.12% MoM and 20.74% YoY from USD 8.19/kg, while Robusta fell 8.75% MoM and 15.06% YoY from USD 7.41/kg. The sharper drop in Arabica reflects the unwinding of last year’s weather premium, as improved rainfall in Brazil and projections of a 17.2% YoY increase in 2026 output significantly reduced fears of crop stress. With Arabica production forecast to rise 23.2%, futures markets have repriced to reflect improved availability, triggering fund liquidation and accelerating the three-week decline.

Brazil’s domestic data confirms that supply expectations are the dominant driver. Arabica prices fell 8.75% MoM and 15.06% YoY, while Robusta dropped 9.82% MoM and 38.94% YoY from USD 5.73/kg. The much steeper YoY fall in Robusta indicates structural expansion rather than temporary adjustment. Elevated prices over the past two seasons incentivized acreage growth beyond traditional producing areas, improving productivity and increasing medium-term supply elasticity. This expansion reduces Brazil’s vulnerability to localized shocks and structurally caps upside potential, particularly in the Robusta segment.

Vietnam reinforces the bearish tone. Although domestic Robusta rose marginally 0.33% MoM, it remains 26.82% below last year’s USD 5.13/kg level. A 38.3% YoY surge in January exports signals active shipment flows and a comfortable exportable supply. At the same time, Intercontinental Exchange (ICE)-monitored inventories have rebuilt, weakening the scarcity narrative that supported record prices in 2025. Together, Brazil’s production expansion and Vietnam’s export momentum explain the synchronized decline across both benchmarks.

Prices are likely to remain under pressure in the short term as harvest data confirms larger Brazilian volumes and Vietnamese exports stay elevated. Arabica may find support sooner due to a tighter global balance relative to Robusta and stronger quality differentiation, but sustained recovery would require either renewed weather stress or a material drawdown in exchange stocks. Robusta faces greater downside risk if Brazil’s geographic expansion continues, as structural supply growth could shift the market from cyclical tightness to persistent surplus. Recent data suggest a transition toward range-bound to moderately bearish pricing, with volatility increasingly tied to confirmation of production rather than speculative risk premiums.

3. Strategic Recommendations

Adopt a Defensive and Origin-Differentiated Strategy as Supply Normalization Caps Near-Term Upside

As of W6 2026, price behavior confirms that the coffee market has shifted from weather-risk premium to supply-driven repricing. With Arabica down 16.12% MoM and 20.74% YoY and Robusta falling 8.75% MoM and 15.06% YoY, the dominant driver is improving Brazilian crop conditions and expanding Vietnamese exports. Brazil’s projected 17.2% YoY production increase and Vietnam’s 38.3% YoY export surge signal comfortable near-term availability, while rising ICE inventories further weaken the scarcity narrative. Robusta faces structurally heavier pressure due to acreage expansion in Brazil and stronger Vietnamese output, whereas Arabica may stabilize sooner given relatively tighter balance dynamics.

From a trade strategy perspective, buyers should prioritize short-duration and opportunistic procurement rather than locking in long-dated volumes. Arabica exposure can be rebuilt gradually on price dips, particularly for Q2–Q3 shipment windows, as downside appears limited unless harvest confirmations materially exceed expectations. Robusta, by contrast, should be sourced on a rolling basis with minimal forward exposure, allowing portfolios to benefit from continued supply-driven weakness.

According to Tridge’s Eye transaction explorer data, commercial flows remain active in Brazil through companies such as Melitta and Nestle for toasted coffee, while Vietnam shows continued activity via Trung Nguyên in ground coffee. These transaction signals indicate steady export participation from both origins, reinforcing the case for tactical short-term sourcing rather than aggressive stock accumulation.

Over the next one to three months, strategy should remain disciplined and data-driven, reflecting continued supply normalization and limited upside momentum.

First, maintain light inventory coverage for Robusta and favor Vietnamese origin contracts with flexible shipment terms to capture potential additional downside. Second, selectively secure Brazilian Arabica volumes during market dips to hedge against renewed weather volatility while avoiding excessive forward commitments.

Third, align procurement with product mix strategy, leveraging Brazilian suppliers for roasted and premium formats and Vietnamese supply for cost-efficient blends. Fourth, use selective short-term hedging on ICE to manage volatility, but avoid building large speculative long positions until confirmed evidence of tightening stocks or weather disruption emerges.

Positioning should remain defensive, liquidity-focused, and opportunistic, recognizing that structural supply expansion, particularly in Robusta, continues to cap sustained upside potential.