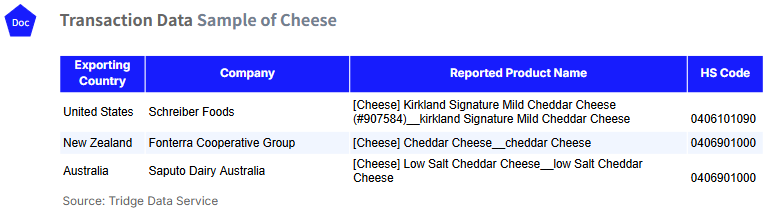

In W7 2026, EU cheddar prices fell due to subdued domestic demand and high carryover inventories, while Oceania cheddar rose, supported by seasonal supply tightening and steady exports. US cheddar declined amid ample stocks, though monthly gains reflected temporary foodservice and export support. EU cheese exports reached 1.39 mmt in 2025, highlighting cheese’s central role amid strategic adjustments, rising costs, and environmental pressures. Trade tensions with China add further complexity, as definitive anti-subsidy tariffs of 7.4% to 11.7% replaced provisional duties of 21.9 to 42.7%, restoring some competitiveness but requiring EU exporters to navigate regulatory and competitive challenges. To address weak EU prices and trade uncertainty, processors are advised to prioritize value-added cheese products, diversify export markets, and leverage seasonal demand channels in Southeast Asia, Oceania, and the Middle East to stabilize revenues and reduce exposure to commodity price volatility.

1. Weekly Price Overview

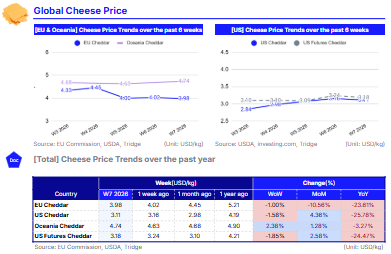

Soft Domestic Demand and High Inventories Weigh on EU and US Cheddar Prices

In W7, cheddar prices in the European Union (EU) declined to USD 3.98 per kilogram (kg), falling 1.00% week-on-week (WoW) and dropping by 10.56% month-on-month (MoM) and by 23.61% year-on-year YoY). This sustained weakness points to subdued domestic consumption across parts of Europe, coupled with elevated inventories carried over from late 2025. Improved milk availability toward the end of last year likely boosted cheese production, further adding to supply-side pressure.

In contrast, Oceania cheddar rose to USD 4.74/kg, up 2.38% WoW and 1.28% MoM, while posting only a modest 3.27% YoY decline. The upward momentum is largely seasonal. As Southern Hemisphere milk production moves past its peak, cheese output gradually tightens, lending support to prices. Oceania’s strong export orientation also plays a stabilizing role, with steady demand from Asia and the Middle East underpinning market confidence. The relatively limited annual decline compared to Europe and the United States (US) indicates a healthier structural balance between supply and export demand.

Meanwhile, US cheddar prices fell to USD 3.11/kg, declining 1.58% WoW and 25.78% YoY, although still remaining 4.36% above month-ago levels. The weekly drop signals renewed spot market pressure, likely driven by comfortable cold storage inventories and steady milk production. However, the positive monthly performance suggests that earlier in the period, improved foodservice demand and export activity to Latin America and Asia provided temporary support. The steep annual decline reflects a clear normalization from 2025, when tighter milk supplies and strong domestic consumption had pushed prices significantly higher.

US cheddar futures settled at USD 3.18/kg, decreasing 1.85% WoW and 24.47% YoY, but still 2.58% higher MoM. The futures curve indicates that market participants expect continued near-term softness rather than a sharp downturn. Earlier monthly gains reflected seasonal demand optimism, yet the recent weekly pullback highlights cautious sentiment amid adequate milk supplies and broader macroeconomic uncertainty weighing on consumer spending.

2. Price Analysis

High Inventories and Trade Uncertainty Weigh on Global Cheese Markets

In 2026, the European dairy market is undergoing strategic adjustment rather than expansion, with cheese at the core of value optimization. Structural pressures, including environmental constraints, high costs, and profitability challenges, are limiting volume growth, particularly in key producing countries such as Germany, France, the Netherlands, and Poland. As a result, processors are prioritizing higher value-added channels, positioning cheese above butter and milk powders as the primary driver of milk value creation.

The EU produced 10.8 million metric tons (mmt) cheese in 2024, decreasing slightly to 10.72 mmt in 2025, a 0.7% decline YoY, despite tighter milk availability. Exports totaled around 1.39 mmt in 2025, highlighting cheese’s central role in EU dairy trade. However, trade tensions with China have added complexity. Following an investigation launched on August 21, 2024, China imposed definitive anti-subsidy tariffs of 7.4% to 11.7% on certain EU dairy products, including fresh and processed cheeses, effective February 13 for five years. These replaced provisional duties of 21.9% to 42.7% announced in Dec-25. While the lower final tariffs are more favorable and restore some competitiveness, allowing EU exporters to maintain market access and stabilize revenues, they still create challenges. Exporters must navigate regulatory requirements, ongoing political tensions, and competitive pressure from both domestic Chinese producers and countries benefiting from free trade agreements.

Globally, cheese markets remain supported but show mixed price signals. In the US, Jan-26 cheese stocks totaled 1.38 billion pounds (lbs), up 0.2% YoY, reflecting strong demand despite rising output. The Chicago Mercantile Exchange (CME) spot Cheddar blocks rose to USD 1.5225, while inventories, especially bulk products, gradually increased. At Global Dairy Trade (GDT) Event 398, New Zealand cheddar declined overall, although volumes exceeded year-ago levels. Over 78% of traded cheddar was for Apr-26 - Jun-26 delivery, with prices ranging from +0.3% in Apr-26 to −3.9% in Jun-26. Southeast Asia/Oceania remained the top purchasing region, highlighting cheese’s continuing strategic role in global dairy trade.

3. Strategic Recommendations

Value-Added Cheese and Market Diversification Key for EU Exporters in 2026

Given the sustained weakness in EU cheddar prices, driven by subdued domestic consumption and high carryover inventories, processors and exporters should prioritize value-added product strategies rather than volume expansion. This includes increasing production of specialty cheeses, geographical indication (GI) products, and private-label premium cheeses, which can command higher margins and reduce exposure to commodity price volatility. Diversifying packaging sizes and formats for retail and foodservice channels can also stimulate consumption, particularly in markets showing softer demand.

To mitigate the impact of ongoing trade tensions with China, EU exporters should strengthen alternative export markets. While China remains an important destination, the imposition of anti-subsidy tariffs, even at reduced rates, increases regulatory complexity and competitive pressures. Expanding trade relationships in Southeast Asia, the Middle East, and Latin America can help stabilize export revenues and reduce dependency on a single market. Collaborating with local distributors, leveraging free trade agreements, and highlighting the quality and certification credentials of EU cheeses can improve competitiveness in these regions.

For globally oriented processors, prioritizing export channels with strong seasonal demand, such as Southeast Asia/Oceania for New Zealand cheddar, can help stabilize cash flows.