In W8 in the maize landscape, some of the most relevant trends included:

- The 2024/25 global corn output is projected at 1.21 billion mt, down 1.4% YoY, with production declining in the US, the EU, and Ukraine. Conversely, Brazil’s output is expected to rise by 3.3% to 126 mmt.

- Argentina’s corn estimate declined by 1 mmt to 46 mmt due to irregular rainfall and high temperatures, while Bulgaria recorded its smallest harvest since 2012, impacted by heat, drought, and heavy rains. Brazil’s first crop planting is nearly complete, with accelerated harvest.

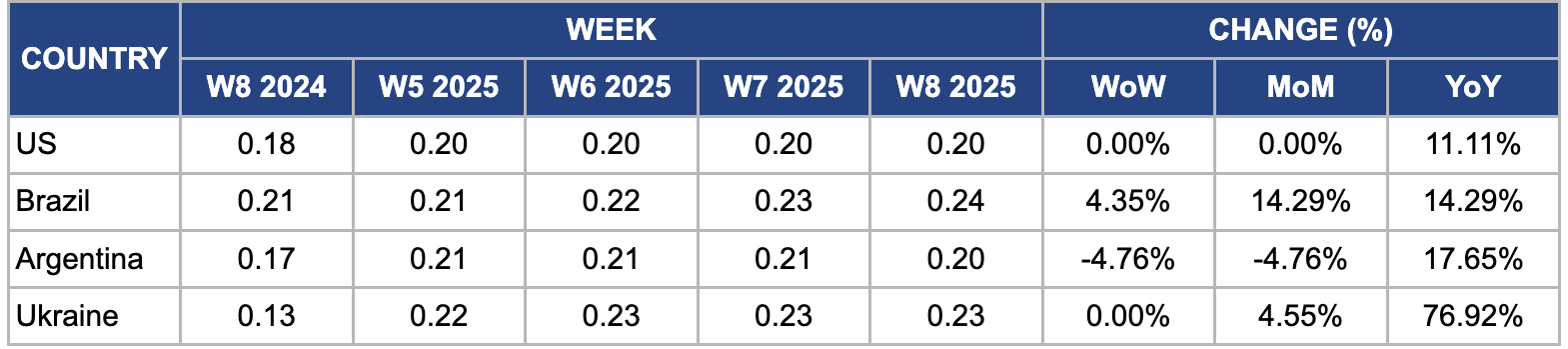

- In W8, US maize prices remained stable but rose 11.11% YoY, while Brazil’s prices surged due to strong export demand and logistical disruptions. In contrast, Argentina’s prices fell MoM as supply improved, whereas Ukraine’s prices spiked YoY due to severe drought-driven production declines.

1. Weekly News

Global

Global Corn Production to Decline 1.4% YoY in 2024/25

Global corn production for the 2024/25 season is at 1.21 billion metric tons (mt), marking a 1.4% year-on-year (YoY) decline from 1.23 billion mt in 2023/24. The United States (US) is expected to produce 377.6 million metric tons (mmt), down 3.1% YoY, while China’s output is forecast to rise by 2.1% to 294.9 mmt. Forecasts indicate a 6.3% decline in the European Union (EU) to 58 mmt and an 18.5% drop in Ukraine to 26.5 mmt. In contrast, Brazil’s corn output should increase by 3.3% to 126 mmt.

Argentina

Argentina’s Corn Output Cut to 46 MMT Due to Heat and Irregular Rain

Rainfall in W7 benefited Córdoba, Southern Santa Fe, Entre Ríos, and Northern Buenos Aires, while additional precipitation hit North-Central and Eastern Argentina over the weekend. Irregular rainfall and high temperatures have lowered Argentina’s corn production estimate by 1 mmt to 46 mmt. The corn rated good/excellent has dropped 9% from the previous week to 16%. Meanwhile, 33% of the crop suffers from poor/deplorable conditions, while 51% remains in fair condition. Soil moisture levels have also declined, with 41% falling into the short/very short category, while 59% remains favorable/optimum, marking a 4% decrease in favorable/optimum moisture from the previous week.

Brazil

Brazil’s 2024/25 Summer Corn Harvest Reached 21.1%, Planting Nears Completion

The National Supply Company (CONAB) reports that planting for Brazil’s first 2024/25 corn harvest reached 98.1% as of February 16, up from 96.8% in W7 and in line with last season’s 98.3%. Piauí, Bahia, Goiás, Minas Gerais, São Paulo, Paraná, and Santa Catarina have completed planting (100%), while Rio Grande do Sul (99%) and Maranhão (81%) are nearing completion. Harvesting is advancing rapidly, with 21.1% of crops harvested, up from 13.3% last week, closely tracking the 21.4% progress recorded in 2024. Paraná (67%), Rio Grande do Sul (60%), Santa Catarina (24.2%), São Paulo (4%), and Bahia (0.4%) lead the harvest. Scattered rains in Paraná aided operations, while Bahia has just begun harvesting activities.

Bulgaria

Bulgaria’s 2024/25 Corn Harvest Hits a Decade Low

In the 2024/25 season, Bulgaria experienced its smallest corn harvest since 2012, with production dropping by 37% YoY, according to the United States Department of Agriculture (USDA). Intense summer heat and drought, followed by heavy rains during the harvest, significantly affected both yields and crop quality, leading to high variations in aflatoxin levels.

United States

US Corn Acreage to Rise 4.2% YoY in 2025 Amid Strong Demand

In spring 2025, US farmers are set to expand corn acreage by 4.2% YoY to 94.6 million acres, driven by rising global prices, strong export demand, and record ethanol production. Profitable margins in the livestock and poultry sectors are further boosting corn demand. While traditional crop rotations typically guide planting decisions, higher corn prices compared to other crops have prompted farmers to adjust acreage. Moreover, some acres previously used for silage corn will be converted to grain corn production, increasing grain corn acreage by 5% to 87 million acres. However, the report warns that potential trade conflicts with Canada and Mexico could threaten US corn exports, with disputes possibly restricting ethanol exports to Canada and significantly reducing corn shipments to Mexico.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W8 2024 to W8 2025)

United States

In W8, the US wholesale maize prices remained stable week-on-week (WoW) but rose 11.11% YoY to USD 0.20 per kilogram (kg). This increase reflects higher production costs, including rising input prices for fertilizers, fuel, and transportation over the past year. Moreover, stronger export demand, particularly from key buyers like Mexico and China, may have supported prices. Weather-related concerns, such as dry conditions in some US growing regions, could have also influenced market sentiment, keeping prices elevated compared to last year.

Brazil

In W8, Brazil’s wholesale maize prices climbed 4.35% WoW, 14.29% month-on-month (MoM), and 14.29% YoY to USD 0.24/kg, driven by strong export demand, particularly from China, as Brazilian corn exports surged 12.3% YoY in Jan-25. Domestic logistics disruptions, including transportation delays in Mato Grosso and Paraná due to heavy rains, have slowed maize shipments to ports, tightening domestic supply. Furthermore, lower-than-expected early harvest yields in some regions have added upward pressure on prices.

Argentina

In W8, Argentine maize prices declined by 4.76% WoW and MoM, reaching USD 0.20/kg. This is due to improved supply conditions as the harvest progressed, increasing market availability. Favorable weather conditions in key maize-producing regions, such as Buenos Aires, Córdoba, and Santa Fe, may have supported higher yields, contributing to the price drop. Moreover, currency fluctuations and macroeconomic instability played a role in price movements. The Argentine peso’s depreciation against the US dollar has made exports more competitive, encouraging higher shipments and potentially increasing supply in the domestic market. However, inflation and financial instability may have also impacted production costs and farmer selling decisions, adding to price volatility.

Ukraine

In W8, Ukraine’s wholesale maize prices remained stable WoW but surged 4.55% MoM and 76.92% YoY to USD 0.23/kg, reflecting supply concerns driven by a sharp decline in domestic maize production. Severe drought conditions throughout the growing season significantly reduced yields, limiting overall supply. The USDA projects Ukraine’s 2024/25 marketing year (MY) corn output at 25 mmt, marking a 23% YoY decline and the lowest production level since 2017. The drought stunted crop development and delayed harvest progress in some regions, exacerbating supply constraints. With tighter domestic availability and strong global demand, particularly from key export markets, maize prices continue to receive upward support.

3. Actionable Recommendations

Diversify Corn Export Markets and Strengthen Trade Agreements

To reduce reliance on key buyers like Mexico and China, US exporters should actively explore new markets in Southeast Asia and Africa, where demand for animal feed and biofuels is rising. Countries like Vietnam, Indonesia, and Nigeria are increasing corn imports to support their growing livestock and poultry industries. Engaging in trade missions, participating in international agricultural trade fairs, and forming strategic partnerships with regional grain importers can help establish long-term trade relationships. By diversifying their export destinations, US corn producers can mitigate risks associated with trade disputes and fluctuating demand from dominant buyers.

Enhance Supply Chain Efficiency to Mitigate Logistics Disruptions

Brazil, one of the world’s top corn exporters, has faced significant logistical challenges due to heavy rainfall disrupting transportation in key producing states like Mato Grosso and Paraná. Investment in better road, rail, and port infrastructure is necessary to prevent such disruptions from tightening domestic supply and delaying shipments. Exporters and farmers should collaborate with logistics providers to optimize transport routes and improve storage facilities near ports. Streamlining supply chain operations will help maintain consistent export flows, reduce costs and enhance Brazil’s global competitiveness.

Promote Sustainable Corn Production to Counter Climate Risks

Extreme weather conditions have severely impacted corn yields in countries like Ukraine and Argentina, where droughts and irregular rainfall patterns have lowered production. To mitigate climate risks, farmers should adopt sustainable farming practices, such as using drought-resistant corn varieties, optimizing irrigation systems, and implementing precision agriculture techniques like satellite monitoring of soil moisture levels. Governments and agribusinesses should also promote climate-smart agriculture programs to help farmers adapt to changing weather conditions. Investing in resilient farming methods will improve yield stability, ensuring long-term supply security, and reducing price volatility in global markets.

Sources: Tridge, NoticiasAgricolas, UkrAgroConsult