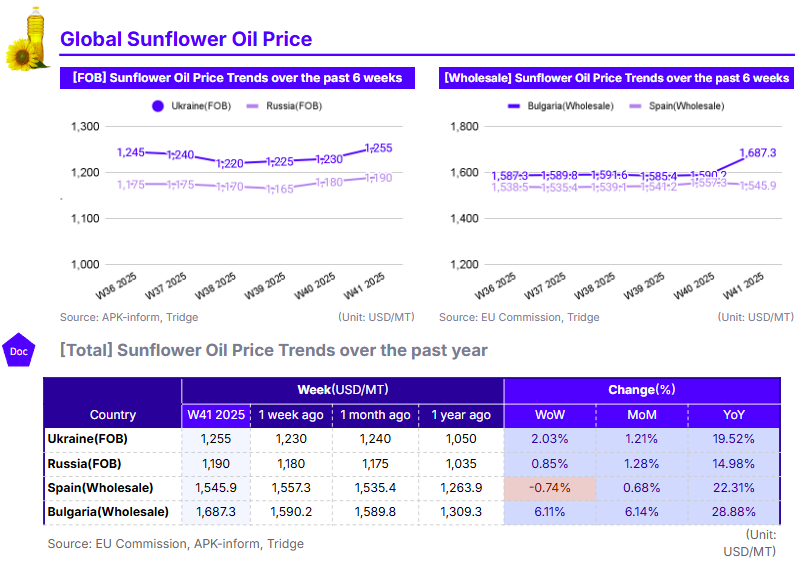

W41 2025: Sunflower Oil

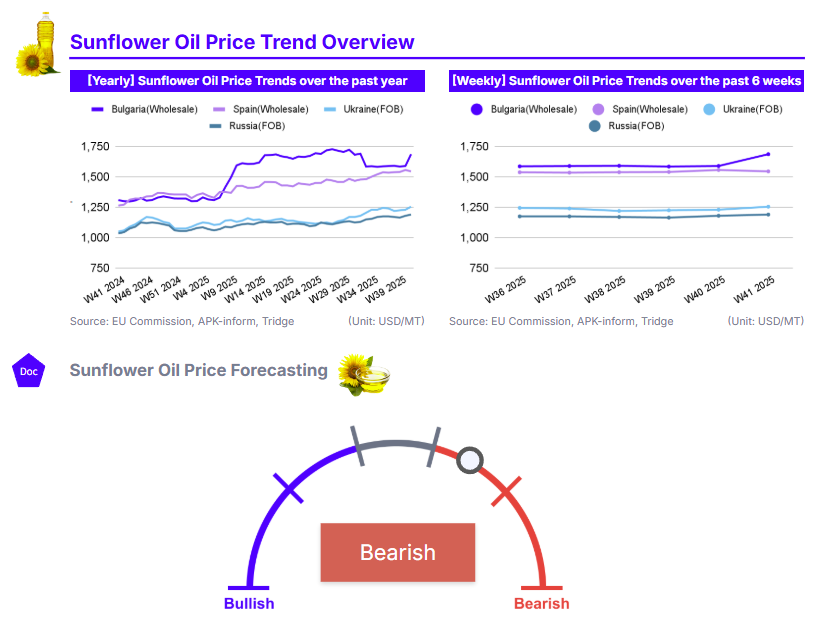

In W41 of 2025, global sunflower oil prices were primarily driven by weather-related supply concerns in the Black Sea region. Heavy rains in Ukraine delayed its harvest, causing a sharp 2.03% week-on-week (WoW) price increase, while the effects of a summer drought spurred a 6.11% price surge in Bulgaria. In contrast, Russia’s prices remained more stable due to a stronger harvest outlook, offering the most competitive export price at USD 1,190/mt. On an annual basis, prices are up significantly across all analyzed regions—ranging from 15% to 29%—highlighting market tightness from supply issues, especially in the Black Sea region. For buyers, Russia emerges as a key sourcing option due to its price competitiveness and expected large harvest. However, importers must balance this opportunity with careful management of the associated geopolitical and logistical risks to ensure supply chain stability.

1. Weekly Price Overview

Black Sea Weather Woes Drive Sunflower Oil Prices Higher

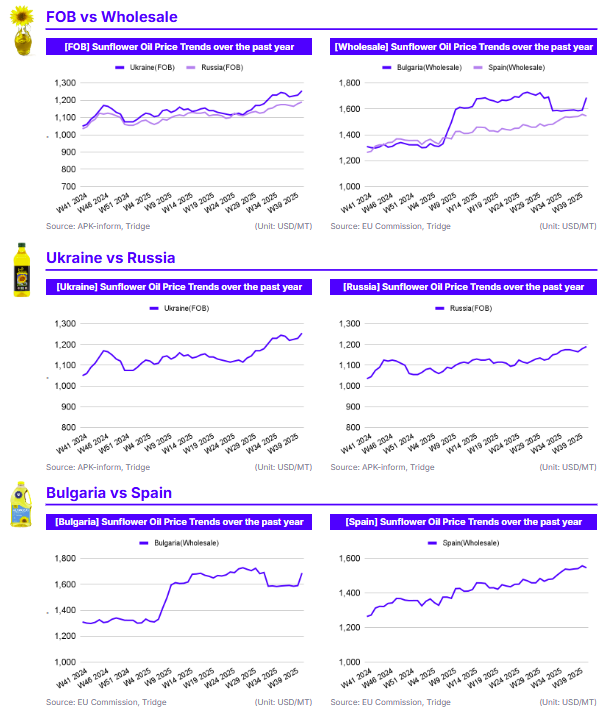

In W41 of 2025, sunflower oil prices showed mixed but predominantly upward movement, largely driven by adverse weather in key Black Sea producing regions. In Ukraine, the Free on Board (FOB) price for sunflower oil was USD 1,255 per metric ton (mt), a notable 2.03% increase WoW. Similarly, Bulgaria saw a significant wholesale price surge of 6.11% WoW to USD 1,687.3/mt. In contrast, Russia’s FOB price saw a more moderate increase of 0.85% WoW to USD 1,190/mt, while Spain’s wholesale price decreased slightly by 0.74% WoW.

The sharp price increase in Ukraine is a direct result of prolonged heavy rains, which have significantly delayed the sunflower harvest and raised concerns about potential crop losses and quality degradation. This has tightened immediately available supply. Bulgaria’s price spike reflects the lingering impact of a severe summer drought that has curtailed yield forecasts across Southeast Europe. Russia's more stable price movement is supported by a comparatively better harvest outlook and a strategic focus on increasing export volumes to key markets like India. Spain's minor price dip stands in contrast to the supply-side pressures in Eastern Europe, likely reflecting localized demand dynamics.

2. Price Analysis

Structural Supply Tightness Underpins Strong Annual Price Gains

Examining the longer-term trend, sunflower oil prices in W41 of 2025 demonstrate significant year-on-year (YoY) increases across the board, highlighting persistent market tightness. In Spain, the wholesale price has risen 22.31% YoY, while prices in Ukraine and Russia are up 19.52% and 14.98% YoY, respectively. Bulgaria has experienced the most dramatic annual increase at 28.88%. The month-on-month (MoM) changes, however, are more varied. Bulgaria’s price jumped 6.14% MoM, whereas Ukraine, Russia, and Spain posted more modest MoM gains of 1.21%, 1.28%, and 0.68%, respectively.

The strong YoY performance is rooted in structural supply issues over the past year, including geopolitical instability in the Black Sea region and challenging weather conditions. Bulgaria's sharp YoY and MoM price hikes are clear indicators of the severe impact of the recent summer drought, which has drastically tightened its supply outlook compared to other regions. The MoM and YoY increases in Ukraine is largely driven by weather related issues resulting in an expected sunflower harvest of 11.4 mmt, the smallest harvest in 10 years. High demand from European importers, who are paying premium prices, is further supporting the elevated price levels by diverting some Ukrainian supply away from other destinations such as India.

The longer term increases in Russia is brought about by a combination of factors. Russia is expecting a record sunflower harvest in the 2025 season, despite weather related issues in Southern Russia. However, Russia is also expected to export a record breaking 5 mmt of sunflower oil in the 2025/26 season, with India being the main buyer, counteracting the supply side pressure of the large harvest and pushing prices up. Despite the high demand from India, Russia still maintains the lowest price level of major exporting countries, likely driven by the large harvest unable to offset demand from international buyers.

3. Strategic Recommendations

Russia Provides Price-Competitive Sourcing Opportunity

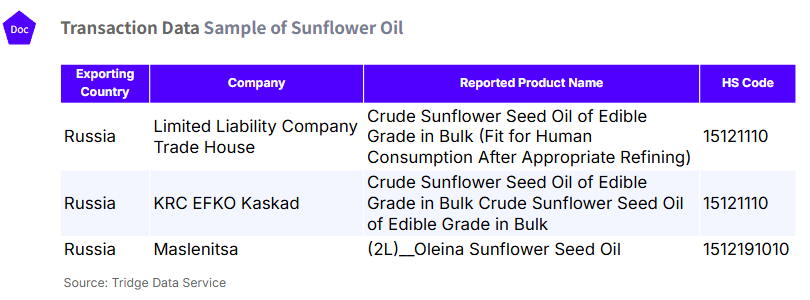

For global buyers and importers of sunflower oil, Russia presents a strategic sourcing opportunity, primarily driven by its significant price advantage and a strong harvest forecast. At USD 1,190/mt, Russia's FOB price is the most competitive among the major producers analyzed, offering a substantial discount compared to Ukrainian and particularly European supplies, which have been inflated by adverse weather conditions. With a favorable production outlook, Russia is well-positioned to increase its export volumes, especially to key demand centers like India, ensuring a more stable and available supply stream in the coming months. This combination of lower cost and higher volume makes Russia an attractive option for buyers. Tridge Eye’s transaction level data highlights Limited Liability Company Trade House, KRC EFKO Kaskad, and Maslenitsa as viable export partners in Russia.

However, pursuing this strategy requires a robust risk management framework. Buyers must diligently assess and mitigate the inherent geopolitical and logistical risks associated with sourcing from a nation involved in an active conflict. This includes securing comprehensive insurance, diversifying shipping and logistics partners to avoid potential disruptions, and staying informed on the evolving sanctions landscape. While the price incentive is compelling, it must be balanced with contingency plans to address potential supply chain interruptions, ensuring that the cost benefits are not negated by unforeseen logistical and geopolitical challenges.