China’s Milk Production is Expected to Increase in 2024 Despite Price Declines

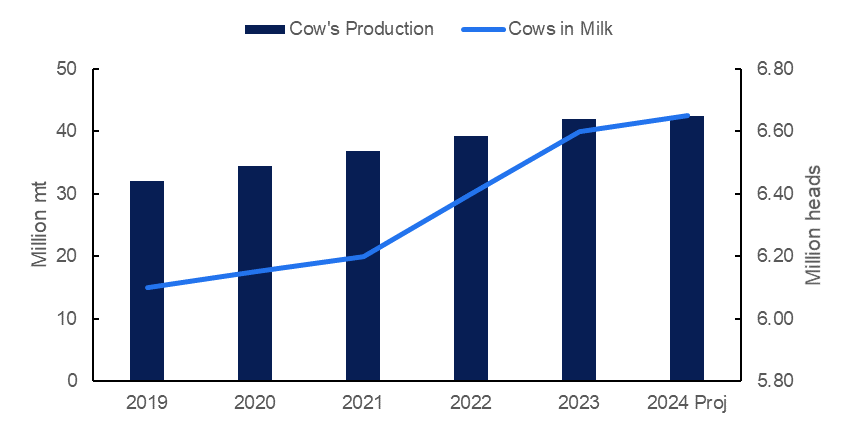

According to the latest report from the United States Department of Agriculture (USDA), China's milk production is expected to reach 42.5 million metric tons (mmt) in 2024, a 1.26% year-on-year (YoY) increase and a 2.41% growth compared to the Jan-24 estimate. Increases in cow inventory and herd productivity have been driving this consistent growth since 2018. USDA data indicates that the number of cows in milk totaled 6.65 million heads at the beginning of 2024, a 0.76% increase compared to the 2023 number. Additionally, the National Bureau of Statistics reported that average milk production per cow was 10.6 metric tons (mt) in 2023, an increase of 0.3 mt per cow from 2022, attributed to improved dairy cow genetics and better herd management practices.

Figure 1: China's Milk Production and Cows in Milk from 2019 to 2024

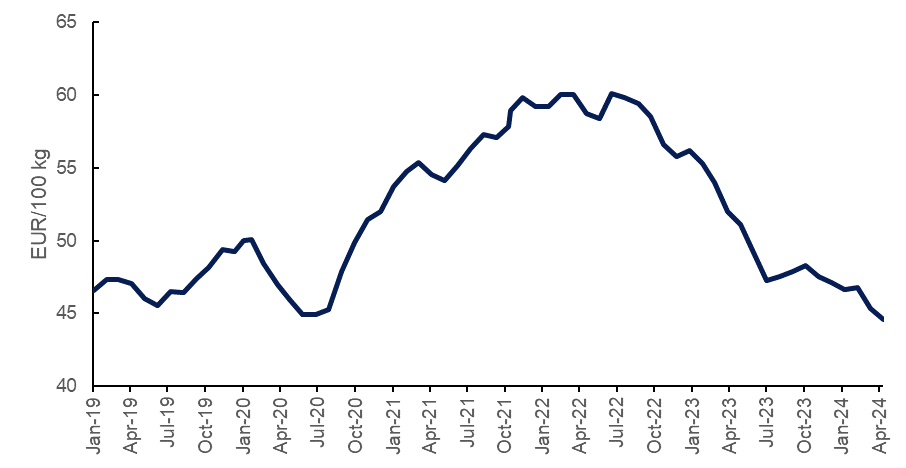

The increased milk production has resulted in an oversupply in the Chinese market, surpassing consumption amid a weak economic environment. The USDA expects China's milk consumption to reach 44.22 mmt in 2024, a 1.10% YoY increase and a 1.70% rise compared to the Jan-24 forecast. This oversupply has caused a significant drop in farm-gate prices. According to the Ministry of Agriculture and Rural Affairs (MARA), milk prices averaged EUR 44.55 per 100 kilograms (CNY 346.85/100 kg) in Apr-24, a 1.74% decline compared to Mar-24 and the lowest level since Oct-18. Farm-gate milk prices have been falling since reaching a historic high of EUR 60.11/100 kg in Jul-22, defying the usual trend of raw milk prices peaking at the beginning of the year.

Figure 2: China's Farm-Gate Milk Price Trend from 2019 to 2024

The persistent decline in milk prices has significantly impacted dairy farmers in China, particularly given the elevated production costs due to geopolitical issues such as the Russia-Ukraine war. The war significantly impacted feed supply in China due to disruptions in the global grain trade, considering that Russia and Ukraine are major exporters of wheat, corn, and barley, which are key components of animal feed. According to the National Dairy Industry Technology System, the average production cost of raw milk on ranches averaged USD 0.53/kg (CNY 3.82/kg) in 2023, matching the highest level in history seen in 2022. This caused the price-to-cost ratio to drop from 1.07 in Jan-23 to 0.98 in Dec-23, marking the first time in over a decade that it has fallen below 1. Consequently, many dairy farms have been operating at a loss, with the USDA indicating that over 70% of farms were selling their milk at a loss by the end of 2023. This financial strain has led to the exit of some small and medium-sized dairy farms from the market in 2023.

Despite the elevated production costs and the closure of some small and medium-sized farms, dairy cow inventories in China continued to grow in 2023, although at a slower pace than in previous years. The National Bureau of Statistics (NBS) reported a nearly 3% YoY increase in cattle inventory for 2023, primarily due to herd expansions at large dairy farms. The USDA noted that the top 40 dairy cattle breeding groups had a stock of 3 million dairy cows at the end of 2023, a 35% increase compared to 2021, which helped more than offset declines among smaller farms. This growth in large farms can be attributed to the adoption of vertically integrated dairy processing operations, which allow these farms to balance lower raw milk prices with net benefits from processing and sales. Additionally, declining beef prices during this period, driven by a supply and demand imbalance, did not incentivize culling dairy cows, further supporting inventory growth.

Looking ahead, China's domestic milk production is expected to continue rising in 2024, albeit at a slower pace than in previous years. This growth is anticipated to be supported by relatively stable dairy cow numbers, improvements in dairy cow genetics, and better herd management practices. However, elevated milk production and subdued consumption amid a challenging economic environment are expected to keep milk prices declining. This oversupply situation is also poised to negatively impact the imports of dairy products into China.