Growth Strategies of German Discount Retailer Chains in the US Retail Market in 2024

The United States (US) retail market remains competitive and dynamic, driven by shifting consumer preferences, economic pressures, and the growing demand for value-oriented shopping experiences. Discount chains have seen increased opportunities as inflation and economic uncertainty push consumers to seek affordable yet quality options. Aldi and Lidl, two German discount supermarket giants, have made significant strides in the US grocery market, albeit with contrasting strategies and outcomes. While Aldi has firmly established itself as a dominant player, Lidl continues to navigate challenges in its quest for a sustainable foothold. Both companies combined cost leadership and operational efficiency, adding rapid market penetration, customer experience, and differentiation as key elements in expanding market share in the US, resulting in mixed outcomes.

Historical Context and Expansion

Aldi entered the US market in 1976, pioneering the discount grocery model with its first store in Iowa. After nearly five decades, Aldi has steadily expanded, operating over 2,400 stores across 38 states as of 2024. Aldi's methodical growth is centered around smaller, no-frills stores offering competitively priced private-label products. Aldi’s deliberate approach has allowed it to build a loyal customer base and maintain operational efficiency.

While Aldi took a more gradual approach, Lidl’s entry in 2017 was marked by a rapid expansion strategy. Lidl opened its first store in Virginia with the aim of rapidly establishing a presence along the East Coast. However, this approach led to mixed results, with some stores struggling to attract customers in highly competitive markets. By 2024, Lidl operates approximately 100 stores across nine states, a far cry from its initial ambitions of 100 new stores per year.

Current Performance

Aldi’s success in the US is evident in its consistent growth and strong market presence. The chain’s focus on cost efficiency, quality private-label products, and streamlined operations has resonated with cost-conscious consumers. Aldi’s ability to adapt to market trends, such as integrating technology into its operations, has further solidified its position. Innovations like checkout-free shopping systems (ALDIgo) and artificial intelligence- (AI) driven supply chain solutions have enhanced customer experience and operational efficiency.

On the other hand, Lidl has faced challenges stemming from its rapid expansion. Many stores struggled to compete with established players, prompting Lidl to recalibrate its strategy. The chain has since focused on improving store layouts, expanding product offerings (particularly in fresh produce and bakery items), and enhancing the overall shopping experience. While these efforts have shown promise, Lidl’s market penetration remains limited compared to Aldi.

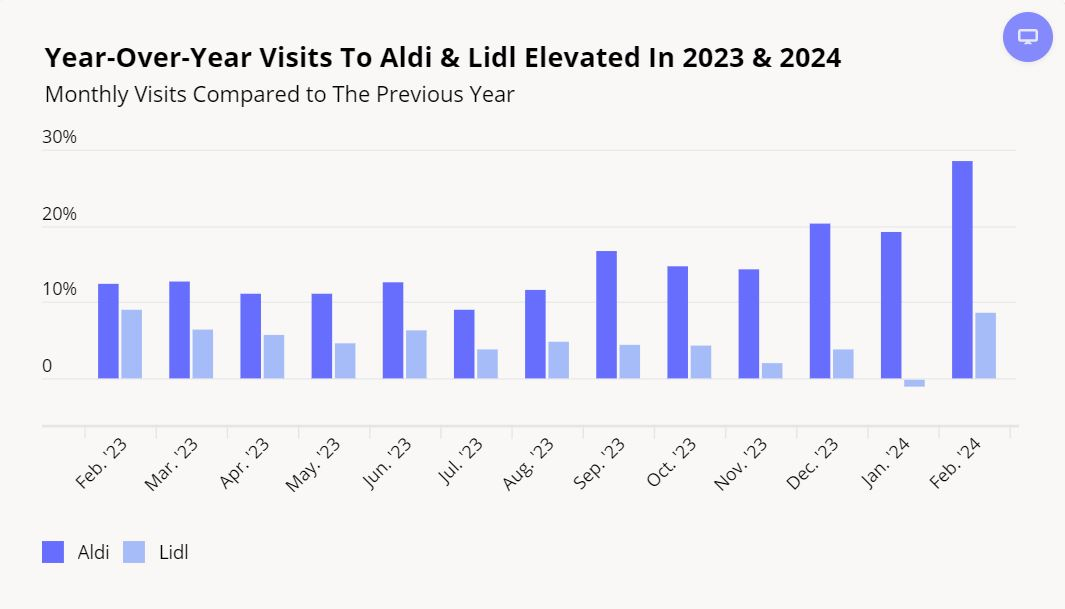

According to Placer.ai, a location analytics platform, insights, from Feb-23 to Feb-24, Aldi and Lidl had seen substantial growth in customer visits. Aldi’s vigorous expansion propelled customer visits from Sep-23, while at the same observing period, Lidl’s visit maintained a stable trend and even fell in Jan-24. Additionally, Placer revealed that while both brands are popular among suburban consumers, Aldi attracts more blue-collar customers, whilst a richer suburban section visits Lidl.

Figure 1. Year-Over-Year Visits To Aldi & Lidl

Source: Placer.ai

Strategies and Future Outlook

Aldi’s strategy revolves around cost leadership, operational efficiency, and customer loyalty. Aldi minimizes costs and margins by offering a limited assortment of private-label products. Its lean business model, combined with aggressive expansion plans—such as acquiring 400 Winn-Dixie and Harvey Supermarket locations—positions Aldi for continued growth. This acquisition will increase Aldi's market share, allowing it to capture a more significant part of the grocery market in the US. With plans to open 800 additional stores by 2028, Aldi is poised to dominate the US discount grocery segment further.

Meanwhile, Lidl focuses on stabilizing its operations and refining its market approach. The chain is investing in modernizing store designs and diversifying its product range to appeal to a broader demographic. While Lidl’s growth trajectory is slower than initially anticipated, its emphasis on quality and customer experience could lead to sustainable progress in the long term.

Aldi and Lidl exemplify two distinct approaches to the US grocery market. Aldi’s steady, methodical expansion and focus on efficiency have made it a formidable competitor, while Lidl’s rapid entry has necessitated strategic adjustments. As Aldi continues to expand aggressively and innovate, Lidl is working to solidify its presence and adapt to the competitive landscape. Both chains remain committed to the discount grocery model, although Aldi’s established dominance gives it a clear advantage in shaping the future of US grocery retail.

The key takeaway for retailers looking to enter or expand in the US market is that success depends on aligning strategy with market conditions and consumer preferences. Whether through cost leadership, rapid expansion, or customer experience, each approach has strengths and weaknesses. Aldi and Lidl’s experiences offer valuable lessons for navigating the challenges of the US retail market in 2024 and beyond.