Japan and South Korea Backed to Be Australia’s Most Important Beef Trading Partners in Coming Years

Overview of the Australian beef industry

Australia has long been one of the world’s leading countries in beef and veal (henceforth beef) production and trade. In 2019, Australia ranked 6th in beef production with 3.95% of total global production, corresponding to 2,431,810 tonnes (carcass weight) out of 61,642,000 tonnes. In terms of export, only Brazil outranked Australia in 2019, when 1,882,952 tonnes of beef, equivalent to 17,29% of the global 10,892,000 tonnes trade, was exported from Australia.

Australia’s beef industry is currently going through a period of herd rebuilding that causes short supply and higher prices. In such times, as Australian beef is becoming relatively uncompetitive with respect to price, it is of utmost importance to have reliable and stable trading partners, where consumers think highly of the Australian produced beef. Such partners are present in Japan and South Korea, which rank 1st and 2nd in terms of Australian beef export destinations. Agribusiness expert Rabobank predict that Japan and South Korea “will continue to form the cornerstone of the Australian beef export market”.

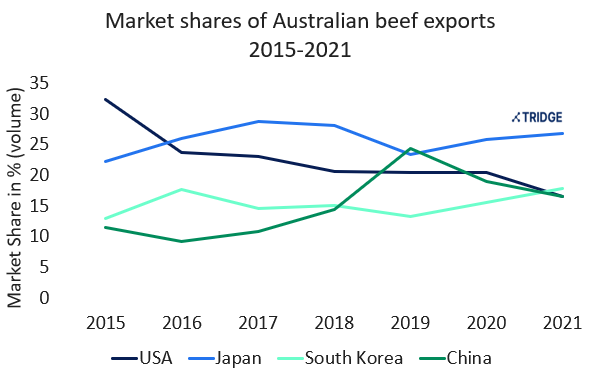

Changes in Market Shares - South Korea moving up to 2nd

During Jan-Sep 2021, South Korea increased their market share by 3.53 percentage points, so that they now hold 17.91% market share and leaves USA and China ranking third with 16.56% and 16.52% respectively. The market leader continues to be Japan that during Jan-Sep 2021 increased their market share by 1.69 percentage points and now sits at 26.77% market share.

Source: MLA Market Statistics

Since 2015, the export volumes destined for the USA have fluctuated between a high of 415,951 tonnes (shipped weight) in 2015 and a low of 211,754 tonnes in 2020, whereas China’s high was 300,133 in 2019 and their low 94,040 in 2019. These comprise fluctuations of 49% and 219% for the USA and China respectively. In comparison, the volumes fluctuated only 17% for Japan and 12% for Korea’s between high and low export volumes in the same time period.

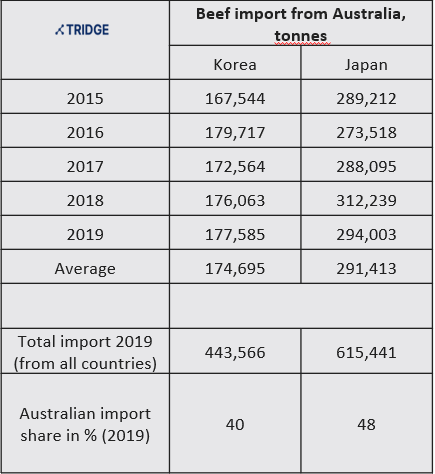

For Korea and Japan, Australia represents an important partner in satisfying their domestic beef demand. As an example, in 2019 40% and 48% of all beef imports to South Korea and Japan respectively originated from Australia.

Source:MLA Market Statistics

Safeguard triggered in South Korean - export will be affected in late 2021

However, the export for South Korea may be negatively affected in the remaining part of 2021, due to a preferential beef safeguard as agreed under the Korea-Australia Free Trade Agreement (KAFTA). According to the terms of the KAFTA, Australia can export a total of 177,569 tonnes of beef to South Korea in 2021 at an 18.6% tariff rate and once exceeded, a 30% tariff rate will apply to exports for the remainder of the calendar year. As of 19 Nov. 2021, the degree of utilisation was 99.43%, meaning a residual of only 1,005.43 tonnes can still be exported under the lower tariff rate. As the triggering of the safeguard is imminent, it can be observed that the trigger date moves slightly backwards compared to 2020, when it was triggered on November 25th. As a result, the 16,391 tonnes exported in December 2020 was subject to a 30% tariff. In 2019, the trigger date was October 17th. and in fact the safeguard has been triggered every year since KAFTA entered into force in 2014, despite the safeguard increasing by 2% per year.

The increased tariff rate for the remaining part of 2021 results in a worsening of the comparative disadvantage that Australian beef exports have in tariffs compared to US products. The tariff differential prior to safeguard triggering is 5.3%, while the post trigger differential is 16.7%.

In 2022, the tariff pre-safeguard triggering will be lowered to 16.1% and the safeguard will be completely outphased by 2029.

A somewhat similar safeguard is in place for Japan under the The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and the Japan-Australia Economic Partnership Agreement (JAEPA). In 2021 (since 1 April), the tariffs have been 25% and 27.6% under the CPTPP and JAEPA respectively. The post-trigger duty under JAEPA is 38.5% and the safeguard is set at 141,700 tonnes for chilled beef and 206,700 tonnes for frozen beef in 2021. The trigger duty under the CPTPP is applied when the import from free trade agreement partners cumulatively exceeds the safeguard. The tariff duties under both CPTPP and JAEPA will fall gradually until the JAEPA tariff rate is 23.5% in 2028 and the CPTPP rate 9% in 2033.

Consumer trends and forecast for beef export to South Korea and Japan

In Japan, beef makes up 19% of meat consumption and despite a shrinking population, Meat and Livestock Australia (MLA) see opportunities for growth for Australian beef exports to Japan, due to high demand for quality red meat and a growing consumer interest in health. Australian beef is leaner than domestically produced wagyu and has proved popular in everyday cooking and the foodservice sector. Grain fed beef from Australia is particularly popular in Japan with 48% of 2020-2021 export volumes consisting of grain fed beef, indicating that this could be an area to target for Australian producers in the years to come. Rabobank forecasts that the import volumes for Australian beef in Japan will increase around 2% per annum between 2022 and 2027.

In South Korea, 21% of meat consumption consists of beef and according to MLA Australian beef has a high status and is the most favored beef import. The South Korean consumers are known to have high awareness of production origin and like the Japanese, the Koreans have a preference for quality products. Among consumers, Australian beef is considered to be of higher quality and higher levels of safety in comparison to US products. South Korea imports mainly grass fed beef from Australia and in 2019-2020 grass fed beef comprised 65% of export volumes. Rabobank forecasts that the import volumes for Australian beef in South Korea will increase around 4% per annum between 2022 and 2027.

Sources

MLA: Korea beef safeguard trigger looming

Farmonline: Japan, Korea the cornerstone of Aussie beef exports

DFAT: KAFTA and trade in goods

Mercardo: Herd rebuild intensifies

Korea-Australia FTA Tariff Rate Quotation List

MLA MARKET SNAPSHOT l BEEF & SHEEPMEAT KOREA

MLA MARKET SNAPSHOT l BEEF & SHEEPMEAT JAPAN