In W10 in the soybean landscape, some of the most relevant trends included:

- Recent rainfall in Argentina stabilized soybean conditions, keeping the production estimate at 48 mmt. Meanwhile, Brazil’s harvest reached 50% completion, but drought in Rio Grande do Sul lowered yields, prompting downward revisions in production estimates.

- Brazil’s Mar-25 exports are forecast at 14.8 mmt, driven by strong Chinese demand.

- China’s 10% tariff on US soybeans will likely shift more demand to Brazil. US soybean acreage is expected to decline as farmers switch to corn.

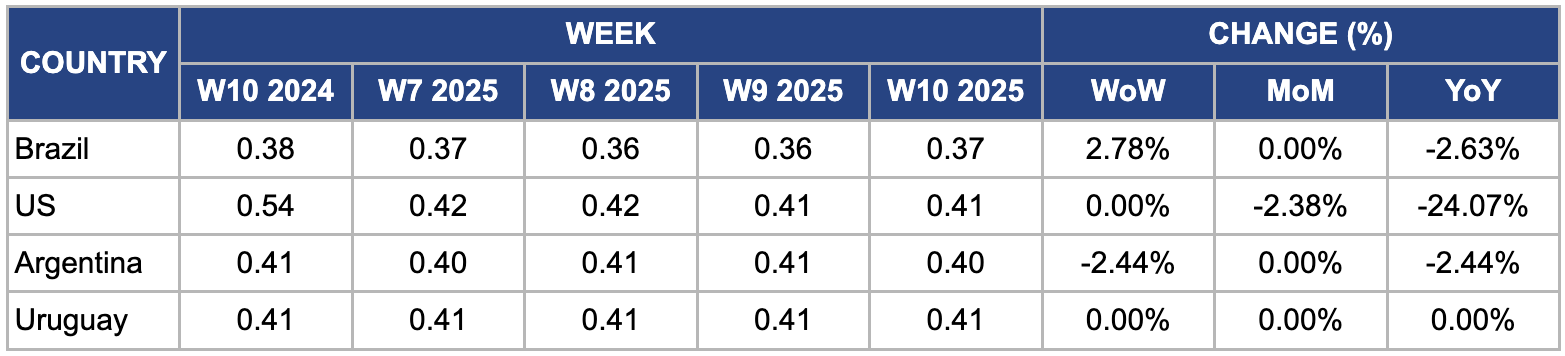

- Brazilian soybean prices rose 2.78% WoW due to increased demand, while US prices remained flat WoW but fell 24.07% YoY due to weak exports. Argentine prices declined 2.44% WoW, while Uruguay’s remained steady WoW amid expanded planting.

1. Weekly News

Argentina

Argentina’s Soybean Conditions Improved Due to Favorable Rainfall

Recent rainfall in Argentina improved soil moisture in central production areas, stabilizing crop conditions and boosting soybean ratings for the second consecutive week. Forecasts predict additional rain in central and southern regions, which could significantly alleviate moisture stress on corn and soybeans. As a result, the soybean production estimate remains unchanged at 48 million metric tons (mmt). Early planted soybeans in key areas are entering the pod-filling stage under optimal conditions, while those in northern regions continue to experience moisture stress. Double-crop soybeans, which struggled with emergence due to hot and dry conditions, have benefited from recent rains. As of late W10, soybean ratings improved, with 24% rated good/excellent (up 7% from the previous week), 43% fair, and 33% poor/very poor.

Brazil

Brazil’s 2024/25 Soybean Harvest at 50%, Second Corn Crop Planting at 80%

As of February 27, Brazil's 2024/25 soybean harvest reached 50% completion, up from 39% the previous week and slightly ahead of last year's 48%. Mato Grosso is nearing the final harvest phase, while other early-season states report steady progress. However, drought and high temperatures in the Rio Grande do Sul continue to reduce yield potential, raising concerns over final output. Meanwhile, Safrinha planting reached 80% completion in the Center-South region, advancing from 64% the previous week but slightly behind 2024's 86%. The rapid pace reflects favorable fieldwork conditions, but weather forecasts raise concerns in some areas, potentially impacting final yields.

Brazil Cuts 2024/25 Soybean Estimates Due to Poor Yields in the South

Several consulting firms have lowered their estimates for Brazil's 2024/25 soybean crop primarily due to disappointing yields in the south. Brazil reduced its forecast by 2.8 mmt to 168.2 mmt, highlighting variable yields in Paraná and Mato Grosso do Sul, with Rio Grande do Sul experiencing the most severe losses – yields are expected to decline by 30 to 40% from initial projections. Soybean acreage is estimated at 47.6 million hectares (ha), a 1.7% increase year-on-year (YoY), with an average nationwide yield of 53.6 bushels per acre. The downward revisions reflect ongoing climate challenges, particularly drought and heat stress in Rio Grande do Sul, which could further impact final production figures.

Brazil’s Soybean Exports to Rise in Mar-25, Driven by Strong Asian Demand

Brazil's soybean exports will rise to 14.80 mmt in Mar-25, surpassing the 13.55 mmt shipped during the same month last year, according to the National Association of Cereal Exporters (ANEC). This growth is due to strong global demand, particularly from Asia, with China as the top buyer. In Feb-25, Brazil exported 9.59 mmt of soybeans, while shipments from February 23 to March 1 reached 3.39 mmt. ANEC forecasts an even higher volume of 4.12 mmt for the week of March 2 to 8, reinforcing the country’s dominant position in the global soybean market.

China

China Raises Tariffs on US Agriculture, Boosting Brazil’s Soybean Outlook

China's additional tariff imposition on the United States (US) agricultural products, including a 10% tariff on soybeans, will likely shift its demand toward Brazil. As the world's largest soybean supplier, Brazil already provides nearly 75% of China's soybean imports, but experts argue that it may struggle to expand its market share further. The tariffs will also drive up soybean premiums in Brazil as global buyers respond to changing trade flows.

United States

USDA Forecasts Lower US Soybean Acreage for 2025/26 as Corn Gains Favor

The United States Department of Agriculture (USDA) expects the US soybean acreage to decline in the 2025/26 marketing year (MY) as farmers shift towards corn due to more favorable market conditions and rising competition from Brazilian soybeans. Soybean acreage will drop by 3.1 million acres to 84 million, while corn acreage will increase by 3.4 million acres to 94 million.

2. Weekly Pricing

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W10 2024 to W10 2025)

Brazil

In W10, soybean prices in Brazil rose by 2.78% week-on-week (WoW) to USD 0.37 per kilogram (kg), up from USD 0.36/kg in W9, driven by a slower harvest pace due to rainfall and increased domestic demand. As of March 2, Brazil had harvested 48.4% of its soybean area, with Mato Grosso leading at 80.5%, followed by Mato Grosso do Sul (58%), Goiás (56%), and Tocantins (55%). Heavy rainfall in Mato Grosso slowed harvesting, while irregular rainfall in Rio Grande do Sul limited production potential in some areas. In Paraná, widespread rains benefited late crops but delayed harvesting. Moreover, concerns over future crop productivity, rising logistics costs, and the USDA’s forecast of lower US soybean planting contributed to the price increase.

United States

In W10, US soybean prices remained unchanged WoW but declined by 2.38% month-on-month (MoM) and 24.07% YoY to USD 0.41/kg, driven by an increased production forecast and weaker demand. The 2024/25 US soybean crop is projected at 118.82 mmt, while ending stocks will be at 10.34 mmt, slightly below the expected market carryover of 10.39 mmt. Moreover, disappointing export sales, including a 17-year low in US soybean sales to China for 2024/25 MY, have further pressured prices. Market sentiment also weakened as trade tensions escalated, with the US imposing tariffs on Mexico, Canada, and China, prompting retaliatory measures from Canada and China. Prices fell to their lowest since early Jan-25 due to these factors.

Argentina

In W10, Argentine soybean prices declined by 2.44% WoW and YoY, reaching USD 0.40/kg. The price drop is due to recent rainfall that improved soil moisture in central production areas, stabilizing crop conditions and boosting soybean ratings for the second consecutive week. Forecasts indicate additional rain in central and southern regions, which could further alleviate moisture stress on corn and soybeans. The soybean production estimate remains unchanged at 48 mmt with improved weather conditions.

Uruguay

Uruguay's soybean prices held steady at USD 0.41/kg in W10, supported by key factors such as favorable market conditions and the expansion of planting area. For MY 2024/25, Uruguay's soybean planting area is projected to reach 1.3 million ha, a 19% increase from the five-year average. This growth is attributed to late-season soybean planting as producers brace for potential challenges from the La Niña weather pattern. The USDA forecasts Uruguay's soybean production for 2024/25 at 3.4 mmt, up from 3.2 mmt in the previous year due to favorable weather conditions.

3. Actionable Recommendations

Diversify Export Markets to Mitigate Risks from Trade Disruptions

With China imposing a 10% tariff on US soybeans, there is an increasing need for US exporters to reduce their reliance on the Chinese market. The trade tensions could reduce demand for US soybeans, making it crucial to explore alternative destinations. One viable strategy is expanding exports to regions such as the European Union (EU), Southeast Asia, and the Middle East, where demand for soybeans continues to grow. For instance, Vietnam and Indonesia are key soybean importers for animal feed and food processing, while the EU remains a significant buyer of soybeans for its livestock sector. By strengthening trade agreements, improving logistical efficiency, and marketing high-protein soybean varieties tailored to the needs of these regions, US suppliers can establish a more resilient and diversified customer base. This approach will help stabilize export demand, reduce dependence on a single market, and provide long-term security against future trade policy changes.

Optimize Supply Chain Logistics to Address Harvest Delays

Heavy rainfall in key Brazilian soybean-producing states such as Mato Grosso and Paraná has slowed the harvest, creating logistical challenges and potential supply bottlenecks. To mitigate these issues, traders and cooperatives should optimize their supply chain by prioritizing shipments from drier regions where harvesting progresses faster. For example, expediting transportation from Goiás and Tocantins, where harvest progress is relatively steady, could help maintain Brazil’s strong export pace. Moreover, investing in increased storage capacity at ports and key production hubs would allow exporters to hold soybeans temporarily during unfavorable weather conditions, reducing the risk of export disruptions.

Leverage Futures and Hedging Strategies to Manage Price Volatility

Soybean prices are experiencing volatility due to multiple factors, including lower-than-expected US export sales, trade tensions, and improving weather conditions in Argentina. With US soybean prices declining and Argentine production stabilizing, producers and traders should consider using futures contracts and options to hedge against further price declines. Farmers and exporters can minimize the financial risks of sudden market downturns by locking prices at favorable levels. For instance, US producers anticipating lower prices in the coming months can utilize soybean futures on the Chicago Board of Trade (CBOT) to secure profitable selling prices ahead of time. Similarly, Brazilian and Argentine exporters facing currency fluctuations and unpredictable demand shifts can employ hedging strategies to protect their revenue margins. Implementing these risk management tools ensures more stable financial planning, reduces uncertainty, and helps producers navigate price fluctuations effectively.

Sources: Tridge, CanalRural, NoticiasAgricolas, UkrAgroConsult