From Conflict to Crisis: How the US–Israel–Iran War Is Disrupting Global Supply Chains

1. Overview of the US–Israel–Iran Conflict and Escalation Dynamics in 2026

The war involving the United States (US) and Israel against Iran in 2026 marks a significant escalation of long-standing tensions in the Middle East. The situation intensified in late Feb-26, with February 28 emerging as a key turning point, when coordinated US–Israeli strikes targeted Iranian nuclear and military infrastructure. These strikes were aimed at curbing Iran’s nuclear capabilities and broader regional influence. However, Iran quickly retaliated with missiles and drone attacks on Israeli cities, US military bases in the Gulf, and strategic infrastructure across the region, pushing the conflict into a wider and more complex confrontation. While the conflict remains ongoing, its intensity and geographic spread have already resulted in heightened security risks across several Middle Eastern countries such as Iraq, the United Arab Emirates (UAE), and Saudi Arabia, particularly through airspace disruptions and heightened security risks.

This escalation follows the Jun-25 Israel–Iran 12-day war, which had already exposed the vulnerability of regional logistics networks, particularly maritime and air transport corridors. However, unlike the brief and contained nature of the 2025 conflict, the 2026 confrontation has evolved into a more prolonged and structurally disruptive crisis. The involvement of the US has significantly increased the scale of military operations and the risk profile of key global trade chokepoints, especially the Strait of Hormuz. As a result, the conflict has led to sustained disruptions to maritime trade routes in the Persian Gulf and raised the level of risk facing key global trade routes, particularly around the Strait of Hormuz.

2. Strategic Importance of the Strait of Hormuz

The Strait of Hormuz is one of the most strategically critical corridors in global trade, connecting Gulf producers to major consumer markets in Asia, Europe, and Africa through the Arabian Sea and the Indian Ocean shipping network. According to the United Nations Conference on Trade and Development (UNCTAD), the Strait of Hormuz handled an average of 20 million barrels of oil per day in 2024, representing about 34% of all seaborne oil exports. UNCTAD data further indicates that the Strait facilitated 38% of crude oil shipments, 29% of liquefied petroleum gas (LPG), 19% of liquid natural gas (LNG), 19% of refined oil products, 13% of chemicals including fertilizers, 2.8% of containers, and 2.4% of dry bulk cargo such as grains a week before the military escalation that began on February 28. These figures illustrate the scale of energy and commodity flows passing through this maritime chokepoint and the potential global consequences if these flows are disrupted.

Given this strategic significance, the military escalation by the US and Israel against Iran on February 28 immediately heightened the risk of widespread disruption. The conflict has raised insurance and security costs for vessels and forced carriers to explore alternative routes, affecting bulk, container, and air freight traffic. In addition to shipping, the movement of key commodities such as fuels, LNG, and fertilizers has been significantly affected, with potential ripple effects on global energy markets and agricultural supply chains.

Figure 2.1. Global Trade Share Transiting the Strait of Hormuz Before the February 28 Escalation

3. Strait of Hormuz Crisis Triggers Ship Freight Volatility and Supply Chain Disruptions

The ongoing war has severely disrupted maritime freight routes, especially through the Strait of Hormuz. Within a short period, a series of tanker attacks near the strait led to a sharp decline in vessel traffic, with only a few ships permitted to pass under strict verification measures. According to UNCTAD data, average daily ship transits between February 1 and February 27 stood at 129 vessels, with 141 vessels recorded on February 27. However, traffic dropped to 81 vessels on February 28 and continued to decline, reaching just four vessels by March 7. This significant reduction is largely attributed to warnings issued by Iran’s Revolutionary Guard, coupled with repeated attacks on vessels in the region.

Figure 3.1. Total Daily Vessel Transits Through the Strait of Hormuz

Major carriers including CMA CGM, Maersk, MSC, and Hapag-Lloyd responded by suspending bookings to and from key Gulf markets such as the UAE, Qatar, Bahrain, Oman, Kuwait, Iraq, and Saudi Arabia, while also restricting flows from India and the Far East. Container operations were further strained when DP World temporarily suspended activities at Jebel Ali, the region’s largest port. As a result, Gulf-bound cargo began accumulating at origin ports, particularly in India and Bangladesh, while alternative transshipment hubs in Singapore, Malaysia, and Sri Lanka saw rising yard utilization.

As the conflict extended into early Mar-26, the disruption spread beyond the Gulf, with renewed security threats in the Red Sea and Eastern Mediterranean forcing carriers to suspend or reroute services. Shipping lines that had cautiously resumed Red Sea transits reverted to diversions around the Cape of Good Hope, adding 10 to 15 days to transit times and increasing schedule unreliability. Despite these disruptions, early freight rate movements remained relatively muted due to seasonal factors due to the Lunar New Year, with the Freightos Baltic Index showing flat rates on Asia–US lanes, and slight declines of 1-2% on Asia–Europe and Mediterranean routes. However, prices for Gulf-specific routes surged sharply, with Shanghai–Jebel Ali rates rising from approximately USD 1,800 per 40-foot equivalent unit (FEU) before war to over USD 4,000/FEU within days due to emergency surcharges. Carriers introduced War Risk Surcharges (WRS) and emergency fees of up to USD 3,000/FEU, alongside fuel surcharges of USD 70 per 20-foot Equivalent Unit (TEU) to USD 75/TEU (regional) and USD 150/TEU (long-haul). Rising oil prices further compounded cost pressures, increasing bunker fuel expenses and pushing insurance premiums to as high as 0.7-1.0% of vessel value per voyage, significantly elevating operating costs.

By mid-Mar-26, the cumulative impact of prolonged disruptions began to spread more broadly across global freight markets. Although non-Gulf container flows initially remained stable, capacity constraints and rising fuel costs started feeding into wider rate volatility, with transpacific rates increasing by 10% to approximately USD 2,022/FEU and Asia–Europe rates rising by 6-15%, depending on the route. Operationally, worst-case scenarios are increasingly materializing, with shippers forced to reroute cargo to alternative ports, change Ports of Discharge (POD), or even return shipments to Ports of Loading (POL). These disruptions are compressing margins for exporters, especially those dealing in low-margin goods, while heightening risks of contract cancellations and weakening demand across affected Middle Eastern markets.

3.1. Global Freight Outlook Amid Strait of Hormuz Disruptions

Looking ahead, logistics and freight markets are likely to remain volatile, with elevated costs and constrained capacity as the war around the Strait of Hormuz could be prolonged. Carriers are rerouting vessels around Africa’s Cape of Good Hope, significantly increasing voyage distances and adding 10 to 15 days to schedules, while war-risk insurance coverage has been canceled by some markets and premiums have risen four- to six-fold. If shipping remains restricted and Red Sea hostilities re-emerge, capacity tightening could force more carriers to suspend Gulf bookings altogether, potentially triggering larger rate spikes and wider congestion at alternative hubs such as Singapore, India, and Oman.

In response, shippers and supply-chain managers should diversify beyond single chokepoints by securing capacity through alternative discharge ports in India, Oman, East Africa, and even Europe, while strengthening landbridge and feeder connections to mitigate Gulf dependency. Contracts should be renegotiated to include dynamic surcharge pass-through mechanisms, force majeure clauses, and flexibility around POD and loading sequences. Securing forward commitments or freight hedges can also help lock in capacity ahead of further rate escalation, particularly on sensitive routes where surcharges have quadrupled. Importers and exporters should maintain pricing buffers of at least 10-20% to account for extended transit times, higher fuel and insurance costs, and potential rerouting.

4. Global Air Freight Disruption from the Gulf Crisis

The US–Israel–Iran war has had an immediate and significant impact on global air freight through widespread airspace closures and airport disruptions across the Gulf, a region that functions as a critical east–west aviation hub. Key airports in the UAE (Dubai and Abu Dhabi), Qatar (Doha), Bahrain, and Kuwait were either fully or partially closed following missile and drone strikes linked to Iran’s Islamic Revolutionary Guard Corps (IRGC), forcing the grounding or diversion of major cargo carriers. This disruption is particularly significant because Gulf airlines, which include Qatar Airways Cargo, Emirates SkyCargo, and Etihad Cargo, collectively account for approximately 13% of global air freight capacity and handle a substantial share of Asia–Europe and Asia–North America transit flows. At the peak of the disruption, Qatar Airways’ operations through Doha were largely suspended, effectively removing around 5% of global cargo capacity from the market. These constraints disrupted major trade lanes, especially those linking South Asia and Southeast Asia to Europe and North America, where cargo typically relies on Gulf hubs for transshipment.

As a result, air freight rates surged sharply across multiple corridors due to capacity shortages and rerouting inefficiencies. According to the Freightos Air Index, South Asia–Europe rates rose by up to 84% to USD 4.72 per kilogram (kg) in the second week of the war, while Southeast Asia–Europe rates increased by 26% to USD 4.23/kg, and Europe–Middle East rates jumped 57% to USD 2.82/kg. On long-haul routes, China–US rates climbed to over USD 7.00/kg, up by approximately 20%, while broader trends showed China–North America rates rising by 2–11% and China–Europe up 2–13% week-on-week (WoW), reflecting both war-related disruptions and seasonal demand factors. In some cases, rates from South Asia to North America and Europe increased by as much as 50% overall, reaching approximately USD 6.00/kg and USD 4.00/kg, respectively.

To mitigate the loss of Gulf hub capacity, forwarders began chartering direct Asia–Europe and Asia–US flights, while others diverted cargo to alternative airports, particularly in Saudi Arabia, with onward delivery by road. Although partial reopening of Gulf airspace and the return of limited capacity from UAE-based carriers have led to some short-term rate stabilization in mid-Mar-26, the continued suspension of key hubs like Doha and ongoing security risks suggest that air freight markets will remain tight and volatile, especially for Asia–Europe lanes that are structurally dependent on Middle East transit routes.

4.1. Global Air Freight Outlook Following Gulf Airspace Disruptions

The ongoing disruption to Gulf airspace is expected to keep global air freight markets tight and volatile, particularly on Asia–Europe and Asia–North America routes that depend on Middle Eastern hubs. With capacity constraints and rate spikes registered, costs are likely to remain elevated despite partial recovery in UAE operations. Continued limitations around Doha and rerouting inefficiencies will sustain pressure on transit times and pricing. In response, shippers should diversify away from Gulf hubs by leveraging direct Asia–Europe and transpacific services, even at a premium, to ensure continuity. Engaging in short-term block space agreements (BSAs) or charter arrangements can help lock in capacity amid uncertainty, while contracts should incorporate flexible routing clauses and fuel surcharge adjustments to manage cost fluctuations. Additionally, building inventory buffers and planning for 20–50% cost fluctuations will be critical to maintaining supply chain resilience in the near term.

5. Impacts on Oil and Fuel Markets

The closure of the Strait of Hormuz has triggered a systemic shock to global energy prices, especially oil. Facilitating roughly a third of the world’s total seaborne oil exports, the Strait is the primary fuel valve for the global economy. In the context of agri-food trade, this disruption acts as a significant cost-multiplier, inflating every stage of the supply chain in the form of more expensive fuel, from farm-level production to international distribution.

5.1. Oil Price Surge and Agriculture Impact

Since the conflict in the Middle East started on February 28, 2026, Brent crude prices have surged past the USD 100 per barrel threshold, compared to around USD 70 per barrel before the conflict, as illustrated in Figure 5.1.1. The primary reason for this price spike is that around 34% of global seaborne oil exports flow through the Strait of Hormuz, the closure of which has cut this supply off from global markets. This oil price shock translates directly into higher fuel prices across the entire supply chain. For example, on average, fuel prices across all US states have risen by 31.03% in the month from 18 Feb-26 to 18 Mar-26, according to data from AAA's Fuel Price Tracker.

This oil and subsequent fuel price spike can have devastating cost implications for the agriculture sector, especially when taking into account that fuel and oil-based lubricants represent between 13% and 15% of total on-farm input costs for mechanized grain production. In regions currently in mid-harvest or preparing for spring planting, such as Northern Hemisphere countries, the sudden jump in diesel prices can drastically compress farmer margins, especially when taken together with higher fertilizer and shipping costs, also due to the conflict.

Furthermore, in developing economies, where transport infrastructure is heavily reliant on road freight, the surge in oil prices can have an even more profound effect. For example, in South Africa, the transportation of agricultural products heavily relies on road transport. Roughly 81% of maize, 76% of wheat, and 69% of soybeans are transported by road. On average, 75% of South African grains, oilseeds, and a substantial share of other agricultural products are transported by road. Should this oil crisis persist, farmers will face tighter margins and profitability issues while consumers will ultimately face higher food inflation.

Figure 5.1.1. Daily Brent Crude and LNG prices, Jan-25 to Mar-26

5.2. Escalation of Bunker Fuel and Maritime Shipping Costs

While crude oil prices dictate the general energy climate, the most immediate and punishing burden on the global agri-food trade is the drastic inflation of marine bunker fuel. The closure of the Strait of Hormuz has created a localized and global scarcity of Very Low Sulphur Fuel Oil (VLSFO) and High Sulphur Fuel Oil (HSFO), the primary fuels for the bulk carriers and container ships that move agriculture commodities globally. As illustrated in Figure 5.2.1., the price for bunker fuel was relatively stable before the conflict, but increased significantly since the conflict started. Prior to the February 28 outbreak, VLSFO (Low Sulphur) prices hovered around USD 510 per metric ton (mt). However, between February 27 and March 9, VLSFO prices surged by 117.7%, jumping from USD 512.50/mt to a staggering USD 1,116.00/mt. HSFO followed a similar trajectory, nearly doubling from USD 436.75/mt on the eve of the conflict to USD 1,073/mt by March 9. Although prices moderated slightly toward mid-Mar-26 as markets adjusted, they remain fundamentally nearly double their pre-war levels.

Figure 5.2.1. Daily Fuel Prices of High and Low Sulfur Bunker Fuel in Singapore

The increase in bunker fuel has added considerable increased costs to maritime logistics, which makes maritime transport of agricultural goods and commodities more expensive, compressing margins along the supply chain as well as ultimately increasing costs to consumers and resulting in food inflation. Furthermore, the closure of the Strait of Hormuz has forced a wholesale abandonment of the most efficient maritime corridor connecting the East and West. By removing the ability to transit the Persian Gulf and subsequently the Suez Canal in some cases, the conflict has fundamentally altered the geography of global trade, shifting the burden to the fuel-intensive bypass around the Cape of Good Hope.

Forcing vessels to avoid the Middle Eastern chokepoints in favor of the Cape route adds approximately 3,500 to 4,000 nautical miles to a standard voyage between Asia and Northern Europe or the US East Coast. This represents a nearly 40% increase in total distance for one of the world's most high-traffic trade lanes. The physical distance translates into a mandatory time penalty as well as increased fuel usage. Depending on the vessel, the rerouting adds between 10 and 15 days to the standard transit time. For the agri-food trade, these delays are not merely a matter of convenience, they represent a critical threat to the shelf-life of perishable goods and disrupt delivery schedules for essential farming inputs and products to markets. Ultimately, agricultural inputs and commodities will take longer to arrive in destination markets and will become more expensive to get to market, increasing costs along the entire supply chain.

6. Impacts on LNG and Fertilizer Markets

The commencement of the Middle East conflict and the subsequent closure of the Strait of Hormuz have fundamentally destabilized the global trade of LNG and agricultural fertilizers. This chokepoint is not only a conduit for global shipping and oil flows, but a vital artery that sustains global energy needs in the form of LNG and global agricultural supply chains in the form of fertilizer supply. The disruption of fertilizer supplies can result in significantly increased production costs for fertilizer reliant crops and can endanger food security in developing countries over the short term.

6.1. Extent of LNG and Fertilizer Exports via the Middle East

The Middle East, including Iran, Qatar, Saudi Arabia, contains some of the world’s largest natural gas reserves, with almost 20% of the world's LNG passing through the Strait of Hormuz, a critical feedstock and energy component in synthetic fertilizer production. Fertiliser production is energy-intensive, relying heavily on natural gas as a feedstock, with energy making up as much as 70% of production costs, as illustrated in Figure 6.1.2. As a result, much of the world's fertilizer is made in the Middle East, with roughly 33% of the world’s fertilizer supply passing through the Strait of Hormuz. A significant portion of global fertilizer production is either directly impacted by the closure of the Strait of Hormuz, or indirectly by the interruption of LNG flow through the strait, including that highlighted in Figure 6.1.1.

Figure 6.1.1. Global Fertilizer Market Exposure to Strait of Hormuz

Collectively, more than 15 million metric tons (mmt) of annual export fertilizer capacity is concentrated in the Persian Gulf and thus affected by the closure of the Strait of Hormuz including the following:

- Qatar - 5.5 to 6 mmt

- Iran - 5 mmt

- Saudi Arabia - 4 to 5 mmt

Fertilizers can be divided into three major nutrient groups - nitrogen, phosphorous, and potassium. Nitrogen is used the most, accounting for approximately 59% of total global fertilizer use in 2023, compared to 21% for phosphate and 20% for potassium. Roughly 45% of global nitrogenous fertilizer use is for growing staple grain and cereal crops like wheat, rice, and maize, which provide over 40% of global caloric intake. Thus, fertilizer is a critical component in agricultural production, especially in ensuring food security in developing countries.

Figure 6.1.2. Monthly Natural Gas Price Index and Urea and DAP Prices, Jan-90 to Feb-26

6.2 Effect of the Hormuz Closure on Global Fertilizer Markets

Since the closure declaration by Iranian forces on March 2, 2026, vessel transits have plunged by 95%, falling from a pre-conflict average of 144 ships per day, according to UNCTAD data, to fewer than five. This has paralyzed LNG and fertilizer supply and has resulted in several fertilizer plant closures, including the following:

- Qatar Energy halted output at the world's largest urea plant after shutting down gas output following attacks on its LNG facilities.

- India cut output in three urea plants as LNG supplies from Qatar have decreased : India buys more than 40% of its urea and phosphatic fertilisers from the Middle East, and recently agreed to buy 1.3 mmt of urea.

- Bangladesh has shut four of its five fertiliser plants.

- Australia's Wesfarmers has warned of possible shipment delays, including for urea.

- Egypt, which supplies 8% of globally traded urea, could struggle to produce nitrogen fertiliser after Israel declared force majeure on gas exports to the country.

The closure of the Strait of Hormuz has triggered a significant spike in global fertilizer prices, driven by the dual pressures of restricted physical supply and soaring feedstock costs. With the Middle East accounting for nearly half of the world's urea exports, the sudden removal of this volume has forced benchmarks to record highs. For example, Middle East Granular Urea prices surged by approximately 40% in the first three weeks of the conflict, jumping from a pre-war baseline of just below USD 500/mt to over USD 700/mt by mid-Mar-26. This volatility is compounded by opportunistic pricing in alternative markets, such as Egypt’s NCIC recently selling Single Super Phosphate (SSP) at USD 335/mt free-on-board (FOB), a significant premium compared to early Feb-26 levels.

As a result, fertilizer prices in the US have surged as much as 32%, with analysts predicting that prices for nitrogen-based fertilisers like urea could roughly double if the war drags on. This shortage and subsequent price surge comes with unfortunate timing, just as the Northern Hemisphere gears up for spring planting season, threatens to compress farmer margins and reduce application rates for the upcoming 2026 season.

6.3. Countries at Highest Risk of Fertilizer Disruptions

Several markets are highly exposed to the conflict in the Middle East from a fertilizer perspective, easier due to direct reliance on fertilizer imports from the Middle East, or reliance on LNG as a feedstock for fertilizer production. According to UNCTAD data, the countries highlighted in Figure 6.3.1. are highly reliant on fertilizer imports from the Persian Gulf and could be severely impacted should the conflict in the Middle East drag on and the Strait of Hormuz remain closed.

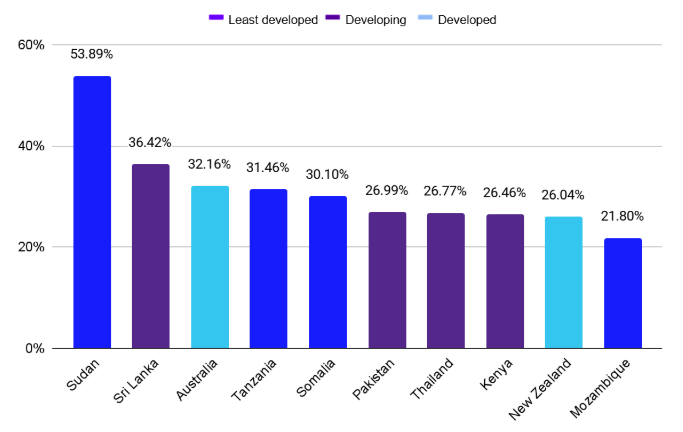

Figure 6.3.1. Share of Fertilizers Imported From Middle East by Country in 2024

Apart from the countries cited above, India and Brazil are also heavily impacted. Brazil imported about 49.11 mmt of fertilizer in 2025, making it the world’s largest fertilizer importing country. Brazil imports 85% of its fertilizer needs, with Middle Eastern suppliers being critical in this supply chain. Although Brazilian officials have noted that the country is well positioned to weather short-term disruptions, any prolonged disruption to production or shipping from the Middle East could tighten fertilizer availability and raise production costs for Brazilian farmers. Prices are already rising rapidly in Brazil. According to the consultancy SoneX, urea has risen over 15% and ammonium nitrate roughly 28% at Brazilian ports. Furthermore, imported nitrogen based fertilizer prices are up about 20% on a regional basis in Mato Grosso, according to the Famato state agricultural federation.

India is in a similarly vulnerable albeit slightly different position. India is the largest DAP importer, accounting for 28.7% of the global market, with much of its supply originating from Saudi Arabia (24%) and Morocco (22%). Similarly, India imports between 20% and 25% of its domestic urea needs, accounting for 7.2% of the global market, again much of its supply originating from the Middle East, from countries such as Oman (15%) and Saudi Arabia (9.5%). Furthermore, India imports about half of its LNG needs, which is a critical feedstock for its 30 urea manufacturing plants. Thus, India is affected by both direct fertilizer imports as well as LNG imports to feed its domestic fertilizer industry. Long term disruptions could be devastating for India’s agricultural sector.

6.4. Alternative Routes and Sourcing Options

Unlike the oil market, which can utilize Saudi Arabia’s East-West Pipeline to the Red Sea, the LNG and fertilizer markets in the Persian Gulf lack scalable infrastructure to bypass the Strait of Hormuz. Furthermore, the fertilizer industry in general does not maintain a strategic reserve but rather largely functions on a just-in-time basis. Seasonal import spikes align with planting cycles, and inventories are not built to absorb major geopolitical shocks such as the current conflict in the Middle East. Thus, countries that rely heavily on fertilizer or LNG supplies from the Middle East could face significant supply challenges and price spikes in the coming months if domestic fertilizer stocks are insufficient for near term planting. This is especially true for Northern Hemisphere countries that are gearing up for the spring planting season.

Furthermore, major fertilizer exporting countries such as Russia and China are unable to cover the shortfall caused by the closure of the Strait of Hormuz. In mid-Mar-26, China banned exports of nitrogen-potassium fertiliser blends and certain phosphate varieties. This was done to protect its domestic market by prioritising food security and insulating their domestic market against price shocks. That would mean between half and three quarters of China's 2025 exports are restricted, which could translate to 40 mmt. This could result in severe supply deficits for countries such as Ethiopia, Malaysia, and Vietnam, which sources more than 50% of its nitrogen and blended fertilizers from China.

Furthermore, Russia, the world’s largest fertilizer exporter, is unlikely to be able to compensate for a potential global shortfall caused by the US-Iran conflict, as their capacity to increase production is limited. Russia accounts for about 20% of global fertilizer trade, but limited production capacity, export restrictions, and recent Ukrainian strikes on major fertilizer plants constrain Russia’s ability to rapidly scale up output and exports. In conclusion, the supply shortfall caused by the conflict in the Middle East cannot be covered from alternative sources and could cause severe fertilizer shortages should the conflict drag on and the Strait of Hormuz remains closed.

7. Implications for Global Food Markets from US-Israel-Iran Conflict

The escalating US–Israel–Iran conflict is emerging as a significant external shock to global food systems, transmitting inflationary pressures through higher energy, fertilizer, and logistics costs. While global agricultural production remains relatively stable, the disruption of key maritime routes, particularly the Strait of Hormuz, is driving up freight costs, delaying shipments, and increasing market uncertainty. These dynamics are disproportionately affecting import-dependent regions such as the Middle East, Africa, and South Asia, where food security is closely tied to global trade flows.

7.1. Global Food Inflation Pressures Intensify as the US–Israel–Iran War Disrupts Supply Chains

The US–Israel–Iran war is beginning to transmit inflationary pressures into global food systems primarily through fuel, fertilizer, and freight, which are the primary input components, creating immediate and lagged effects on food prices. According to the International Food Policy Research Institute (IFPRI), these input cost increases are already feeding into food inflation, with early estimates suggesting food prices could rise by 0.5–1% in developed markets in the short term, and much higher in import-dependent and low-income countries. Moody’s Ratings indicate that since food and fuel account for 30–50% of inflation baskets in emerging markets, compared to less than 25% in developed economies, these shocks are disproportionately amplifying inflation in vulnerable regions.

The direct impact on food prices is uneven but increasingly visible both regionally and globally. In the short term, higher fuel and freight costs are raising the retail prices of perishable goods, meat, and dairy, while shipping disruptions are increasing import costs for staple foods. In the Gulf and Middle East, where countries rely heavily on imported grains, vegetable oils, and sugar, food inflation risks are rising as rerouting and insurance costs push up landed prices. In Africa and South Asia, the impact is more severe, with the Food and Agriculture Organization (FAO) reporting that countries such as Kenya, Bangladesh, and Pakistan, already reporting fertilizer cost increases of up to 40%, face reduced fertilizer use, which could lower agricultural output and tighten domestic food supply later in the year.

Globally, the fertilizer shock is expected to have a delayed but more structural effect, reducing yields for key crops such as wheat and corn and pushing up prices for staples, animal feed, and downstream products like poultry and eggs. While current global food supplies remain relatively stable, analysts warn that if the conflict persists, the cumulative effect of higher input costs, reduced productivity, and disrupted trade flows could drive a sustained rise in global food inflation, particularly in low-income, import-dependent economies.

7.2. Global Agricultural Trade Disruptions from the Strait of Hormuz Conflict

The US–Israel–Iran conflict, particularly following disruptions to the Strait of Hormuz, is creating a logistics-driven shock across key agricultural commodities, including wheat, corn, beef, and tea, rather than an immediate supply-side collapse. Global grain markets remain fundamentally well supplied, with world wheat trade exceeding 200 mmt annually and corn trade above 180 mmt, but flows are highly dependent on maritime chokepoints and Gulf transshipment hubs. According to the United States Department of Agriculture (USDA), the Middle East and North Africa collectively account for around 15% of global wheat imports, with countries such as Iran, Iraq, Saudi Arabia, and the UAE relying heavily on imports. Disruptions at the Strait of Hormuz have already caused delays to dozens of grain vessels and forced rerouting through longer corridors, increasing freight costs by an estimated 10–25% on affected routes. This has translated into short-term volatility in futures markets, with wheat and corn prices recording week-on-week (WoW) increases in early Mar-26 before stabilizing. This reflects heightened risk premiums driven by logistics uncertainty and energy-linked cost pressures.

At the regional level, the Strait of Hormuz disruption is tightening grain import flows into Gulf markets, exposing structural vulnerabilities in food security systems that rely on imports for 60–90% of staple consumption in several countries. For instance, Iran depends on imports for a significant share of its wheat and nearly all of its corn needs as per USDA data, with shipments largely originating from Brazil, Russia, and the Black Sea region. With airspace restrictions and maritime risks, grain vessels have faced delays, and some cargo has been diverted to alternative ports in Oman and the Red Sea, adding inland transport costs and extending delivery times. While Gulf countries such as Saudi Arabia and the UAE maintain strategic reserves covering 4–6 months of consumption, the reliance on rerouted logistics increases handling costs and congestion at secondary hubs. For corn, which is widely used as animal feed, these disruptions indirectly affect livestock production costs across the region, further amplifying food price inflation risks.

For beef, the impact is concentrated on export-oriented supply chains serving Middle Eastern demand, where the Gulf functions as a premium destination for chilled and frozen meat. In Kenya and the broader Horn of Africa, meat exports to Gulf markets, especially during the Ramadan peak, have collapsed to as low as 5% of normal volumes, with shipping costs for livestock rising from about USD 1,000/mt before the war to USD 2,200/mt. This has resulted in stranded cargo at ports such as Mombasa and forced redirection to domestic markets, depressing farmgate prices and incomes. Similarly, major exporters such as Brazil and Australia are facing higher freight and insurance costs, with shipping rates for livestock and chilled beef rising by 20–50% on certain routes and transit times extended due to rerouting. Australia faces disruptions to a market that accounts for 10% of its sheepmeat exports and 3 to 4% of beef exports.

In the tea market, conflict has disrupted the trade by affecting key export markets, logistics corridors, and pricing dynamics, particularly for producers in Kenya and India that rely heavily on Middle Eastern demand. For example, India exported a record 280 million kg of tea in 2025, with Iran and other East Asian markets accounting for a substantial share, while Assam’s orthodox tea segment has increasingly depended on premium demand from the Middle East. Similarly, Kenya exported about 13 million kg of tea to Iran in 2024, valued at approximately USD 30–45 million, with coffee, tea, and spices together contributing over USD 45 million of Kenya’s exports to Iran. However, partial airspace closures over Iran, Iraq, and parts of the Gulf, along with disruptions in maritime routes through the Strait of Hormuz, have led to shipment delays, higher freight and war-risk insurance premiums, and payment uncertainties for consignments in transit. These challenges have particularly impacted orthodox tea, which commands a premium of USD 0.43-0.53/kg (INR 40–50/kg) over crush, tear, curl (CTC) tea and depends on timely delivery to premium Middle Eastern buyers. As a result, exporters are facing margin compression, port congestion, and limited market flexibility, with continued instability likely to sustain volatility in trade flows, costs, and market access.

7.3. Strengthening Agricultural Trade Resilience in Response to Geopolitical Disruptions

To mitigate the ongoing inflationary pressures and trade disruptions, stakeholders across the agricultural value chain should prioritize supply chain diversification and route flexibility. Import-dependent countries, particularly in the Middle East, Africa, and South Asia, should reduce reliance on single chokepoints such as the Strait of Hormuz by expanding the use of alternative corridors through the Red Sea, Oman, and overland logistics where feasible. Governments and large importers can formalize contingency sourcing agreements with multiple exporting regions like Black Sea, Latin America, and Southeast Asia to ensure continuity of grain, beef, and tea supplies.

At the same time, exporters should actively diversify destination markets beyond the Middle East to reduce exposure to geopolitical volatility, leveraging regional trade agreements and emerging demand in Africa and Asia. For instance, tea exporters in Kenya and India should deepen direct relationships with buyers in alternative markets while renegotiating contracts to include flexible pricing clauses that account for freight and insurance volatility. For beef exporters, adopting cold chain improvements, regional processing hubs, and shorter supply cycles can reduce spoilage risks and improve resilience against shipping delays and congestion at ports.

Meanwhile, governments should consider temporary subsidies, tariff reductions, or strategic procurement of fertilizers during periods of price spikes to prevent sharp declines in application rates, which can negatively affect yields of wheat and corn in subsequent seasons. Encouraging local blending, regional fertilizer trade partnerships, and long-term contracts with diversified suppliers can also help smooth supply. In parallel, investments in energy efficiency, such as optimizing transport logistics and promoting fuel-efficient shipping routes, can partially offset rising freight costs that are currently estimated to have increased by 10–25% on affected corridors.