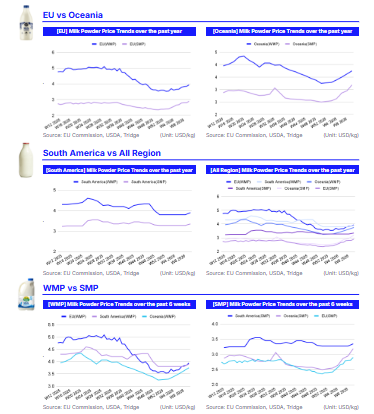

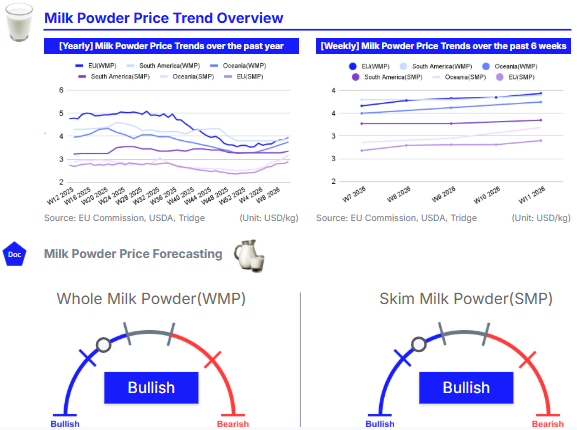

In W11 2026, the global milk powder market recorded a broad-based short-term recovery, with consistent WoW and MoM gains across major exporting regions, although YoY trends remain uneven. WMP showed modest improvements driven by seasonal supply tightening, stable export flows, and renewed buying interest, but continued to face pressure from weaker demand from 2025. SMP strengthened across all regions, supported by tight inventories, robust protein demand, and competitive forward buying. Geopolitical tensions, particularly around key shipping routes, have elevated freight and insurance costs, prompting importers to secure forward supplies and creating short-term scarcity. The market is expected to remain cautiously bullish in the near term, with SMP maintaining strength while WMP sees modest upside, though risks remain from potential demand softening or large inventory releases.

1. Weekly Price Overview

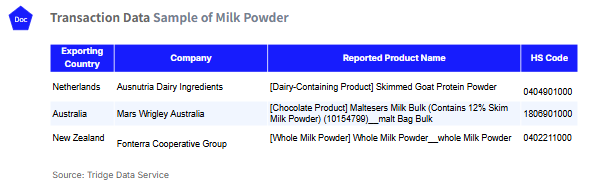

Global Milk Powder Markets Rebound Due to Seasonal Supply Tightening

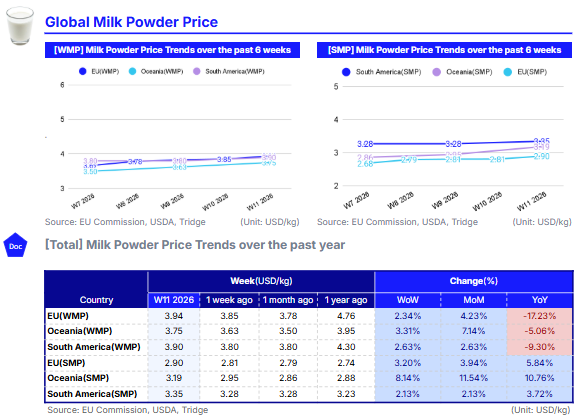

In W11 2026, the global milk powder market recorded a broad-based short-term recovery across all major exporting regions, as reflected in consistent week-on-week (WoW) and month-on-month (MoM) price increases. Despite this upward momentum, year-on-year (YoY) trends remain uneven, with whole milk powder (WMP) still under pressure while skim milk powder (SMP) has moved into a firmer growth phase.

For WMP, the European Union (EU) prices rose to USD 3.94 per kilogram (kg), up 2.34% WoW and 4.23% MoM, although still down 17.23% YoY. The gains are driven by stronger short-term domestic demand, declining inventories, and stable export flows, particularly to the Middle East and North Africa (MENA). However, the sharp YoY decline reflects the lingering impact of excess milk production and weak import demand, especially from China, throughout 2025, which continues to weigh on the market base.

A similar upward trend was observed in Oceania, where WMP prices averaged USD 3.75/kg, increasing by 3.31% WoW and 7.14% MoM, though remaining 5.06% below last year’s level. This growth is primarily attributed to seasonal tightening in milk supply, as the region enters the late production season, reducing exportable volumes. Additionally, strong performance in recent Global Dairy Trade (GDT) auctions has reinforced bullish sentiment, supported by renewed buying interest from key Asian markets.

In South America, WMP prices reached USD 3.90/kg, rising by 2.63% both WoW and MoM, but still down 9.30% YoY. The increase is largely linked to tight spot availability and firm export demand, with many producers reportedly forward-sold through May/June, limiting near-term supply. Nevertheless, the YoY decline highlights the continued influence of weaker global demand conditions observed in 2025.

For SMP, EU prices rose to USD 2.90/kg, marking a 3.20% WoW and 3.94% MoM increase, alongside a 5.84% YoY gain. This growth is supported by tight inventories, firm export demand, and a short-covering effect, where buyers re-entered the market after previously anticipating lower prices.

In Oceania, SMP prices surged to USD 3.19/kg, recording the strongest gains among all regions, with an 8.14% WoW increase, an 11.54% MoM rise, and a 10.76% YoY uptick. The rise reflects tight near-term supply due to seasonal milk production declines, combined with robust demand from North and Southeast Asia, which has intensified competition for limited volumes.

Meanwhile, in South America, SMP prices increased more moderately to USD 3.35/kg, up 2.13% WoW and MoM, and 3.72% YoY. The upward movement is driven by tight spot supplies, steady export demand, and seasonal production dynamics, with particularly strong buying interest from Brazilian importers seeking to replenish inventories ahead of near-term demand.

2. Price Analysis

Protein Demand Supports SMP as WMP Gradually Recovers from Past Declines

At GDT Event 400, held on March 17, 2026, the GDT index edged up 0.1% from the previous event, with the average winning price reaching USD 4,330 per metric ton (mt). Milk powder performance was mixed, with SMP averaging USD 3,409/mt, up 5.2%, while WMP averaged USD 3,709/mt, down 4%. The decline in WMP reflects lingering pressure from historically weaker demand, whereas the rise in SMP was supported by tight spot supply and strong global protein demand. This divergence is mirrored in regional markets, where US non-fat dry milk prices have rallied to levels last seen in 2022, highlighting constrained availability. Structurally, this reflects stronger interest in protein-based dairy products, while fat-heavy products like WMP are recovering more gradually from sharp declines in 2024/25, during which WMP fell by roughly 30% YoY, compared to about 15% YoY declines in protein-focused markets.

Supply dynamics explain much of the recent price behavior. While global milk production continues to expand, the additional output has not fully translated into market availability. In New Zealand, Feb-26 milk collections reached 183.8 million kg of milksolids (+7.4% YoY), with forecasts indicating further growth of 5.4% MoM in Mar-26 and 4.7% MoM in Apr-26. Similarly, the United States (US) reported a 2.9% YoY growth, with herd size reaching 9.62 million heads, the highest in over 30 years, while Argentina posted a 10.6% YoY growth. Despite this broad-based expansion, spot exportable supply remains tight, as processors strategically hold inventories to restore margins after the 2024/25 downturn. Seasonal declines in Oceania milk production are also reducing near-term availability, further supporting upward pressure on prices.

On the demand side, recovery is increasingly evident. While China’s dairy import contraction of 13.7% YoY in Feb-26 is beginning to stabilize, Southeast Asia and MENA are emerging as strong growth markets. This is reflected in trade flows, with New Zealand WMP exports rising by 10% YoY, while SMP exports declined 18% YoY, and total export volumes increased by 0.8% YoY to 342,677 mt, with export value down 2.8% YoY. These patterns highlight that price formation is being influenced more by spot availability and strategic buying than by overall production volumes.

Geopolitical and macroeconomic factors are further amplifying milk powder market movements. Tensions around key shipping routes such as the Strait of Hormuz due to the US-Israel-Iran war have raised freight and insurance costs, prompting importers to secure forward purchases and build inventories, effectively tightening spot supply. This risk-driven purchasing, combined with fragmented global supply chains, has created artificial short-term scarcity, pushing prices higher even amid substantial global stocks.

Looking ahead, the milk powder market is expected to remain cautiously bullish in the short term. SMP is likely to stay firm due to sustained demand and limited availability, while WMP may stabilize with modest upside as Oceania’s seasonal production declines continue. However, risks remain, particularly if China’s demand softens again or if large inventories in Europe and the US are aggressively released, which could constrain further price gains.

3. Strategic Recommendations

Practical Strategies for Stable Milk Powder Margins During Regional Market Variations

In the EU, WMP prices remain under pressure YoY despite recent short-term gains, while SMP is showing firm growth supported by tight inventories and strong export demand. EU exporters should prioritize SMP, focusing on high-demand markets such as Southeast Asia and North Africa, and consider forward contracts to secure margins amid ongoing volatility. For WMP, cautious inventory management is recommended rather than aggressive liquidation, phased shipments to stable buyers can maintain price support. Domestically, promoting value-added WMP products, such as fortified milk powder or blended dairy offerings, can help stabilize demand. Flexible pricing mechanisms, including price-adjusted contracts for key buyers, will also allow exporters to respond quickly to shifts in global supply and maintain competitiveness.

Oceania is experiencing seasonal tightening in milk supply, particularly for SMP, which has driven substantial short-term price gains. Exporters should leverage this seasonal tightness by prioritizing SMP shipments to North and Southeast Asia through premium contracts, while strategically staggering WMP shipments to avoid oversupply in weaker demand regions. Holding strategic WMP inventories for long-term buyers can safeguard future margins, while introducing value-added products, such as fortified or protein-enhanced milk powders, can help counter slower recovery in fat-heavy WMP demand. Forward sales and phased shipment scheduling are crucial to mitigate potential shipping disruptions and to capitalize on bullish sentiment from recent GDT auctions.

In South America, both WMP and SMP prices are rising, though WMP remains below last year’s levels. Exporters should take advantage of tight near-term supply to maximize margins, prioritizing SMP exports to Asia and MENA. Careful coordination of forward-sold commitments is necessary to ensure deliveries meet contractual obligations while leaving flexibility to benefit from spot market price spikes. Domestic demand, particularly in Brazil, requires attention as importers seek to replenish inventories ahead of peak demand; balancing domestic and international supply is essential to avoid price erosion. Dynamic export pricing based on spot market conditions can help maintain competitiveness and profitability during periods of regional tightness.

China’s dairy imports are stabilizing after a contraction, while Southeast Asia and MENA are showing strong demand for SMP and WMP. Suppliers should focus on SMP and protein-rich products for China, emphasizing quality and differentiation through value-added offerings such as fortified or ready-to-use blends. Southeast Asia presents opportunities to capitalize on intense competition for limited volumes; exporters should implement premium pricing and prioritize reliable buyers. In MENA, WMP exports can be optimized through forward contracts and phased deliveries, mitigating risks from elevated shipping and insurance costs due to tensions around the Strait of Hormuz.