1. Weekly News

Brazil

São Paulo Tomato Production Rose 18.4% YoY Despite Severe Drought

According to the Institute of Agricultural Economics (IEA-Apta) of the Secretariat of Agriculture and Supply of the State of São Paulo (SAA), canned or table tomato production increased by 18.4% year-on-year (YoY) during the 2023/24 winter harvest. Despite severe drought conditions in São Paulo, tomato productivity is projected to be 17.6% YoY higher, with table tomato production exceeding 392 thousand metric tons (mt) and an average yield of 92.4 mt per hectare (ha). Similar to peanuts, rice, and soybeans, tomatoes are susceptible to dry weather. However, with significant support from the São Paulo government, the sector is expected to conclude the harvest positively. The state has allocated nearly USD 179 million (BRL 1 billion) in emergency funds for agriculture in response to the drought.

Israel

Israel Faces Tomato Supply Crisis Amid Multiple Challenges

Israel is currently experiencing a tomato crisis due to several factors severely impacting supply. A long-time reliable source of tomatoes, Turkey has halted its exports to Israel. Moreover, the discovery of cholera bacteria in Jordan's Yarmouk River, used for irrigating tomatoes in Jordanian greenhouses, has led the Israeli Ministry of Health to ban the import of Jordanian tomatoes. This situation is aggravated by extreme heat, which could cut tomato harvests by 50% in the coming weeks. The ongoing conflict has also disrupted tomato supply, making some fields inaccessible to farmers. The Gaza Strip, once self-sufficient in tomatoes and a supplier to the Palestinian Authority, now depends on international humanitarian aid for its tomato supply, further straining local resources. To address the shortage, Israel's Ministry of Agriculture has temporarily expanded the duty-free import quota for tomatoes to 5 thousand mt until the end of Sept-24. The first batches of European tomatoes have already started arriving, with deliveries from Greece, the Netherlands, and Poland.

Moldova

Moldovan Tomatoes Export to Israel Approved Amid Trade Expansion

The National Food Safety Authority (ANSA) of the Republic of Moldova has announced that Israel has approved the import of fresh tomatoes from Moldova. According to the decision of the Israel Plant Protection and Inspection Services (PPIS), Moldovan tomato producers can now export their products to Israel, provided they meet specific requirements. Tomatoes must be grown within Moldova and protected against the pest Leptinotarsa decemlineata. Additionally, they must undergo pre-export inspection to confirm the absence of this pest, which is in line with ISPM-31 guidelines. This move is expected to boost trade opportunities for Moldovan producers and offer additional supply options for the Israeli market.

Ukraine

Tomato Prices in Ukraine Increased for Third Consecutive Week Amid Supply Shortages

In W35, the upward trend in tomato prices in Ukraine continued for the third consecutive week, driven by reduced supply from greenhouse plants and crop losses from unfavorable weather affecting ground tomatoes. Greenhouse tomato prices increased 12% WoW, ranging between USD 0.97 and 1.34/kg , due to high demand amidst a shrinking supply. Additionally, tomatoes are now 2.4 times more expensive than at the end of Aug-23. Analysts predict that prices may continue to rise as the farm supply diminishes.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W35 2023 to W35 2024)

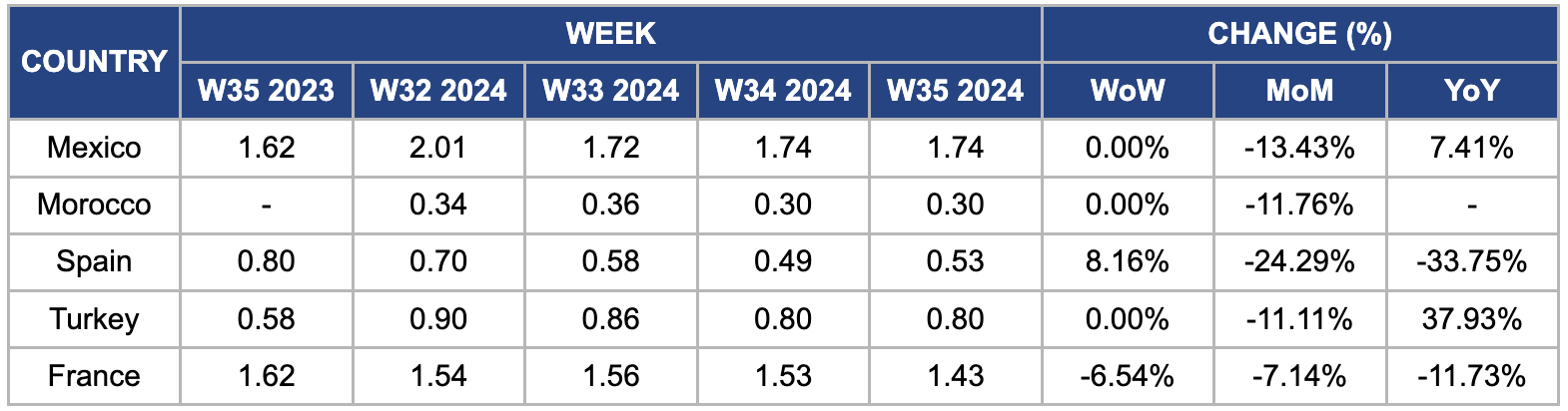

Mexico

In W35, wholesale tomato prices in Mexico remained steady at USD 1.74/kg, maintaining their position as the highest among global suppliers, including France, Turkey, Spain, and Morocco. However, there was a 13.43% month-on-month (MoM) price drop. Mexico's 2024 tomato production forecast is 3.30 million metric tons (mmt), representing a 2% increase from the 3.22 mmt produced in 2023. This anticipated rise in production contributed to price stabilization and potential decreases in the past few weeks. Despite some producers investing in protected cultivation methods, many regions still depend on open-field farming, which exposes them to climatic risks and results in lower yields.

Morocco

In W35, Moroccan tomato prices remained steady WoW at USD 0.30/kg but experienced an 11.76% drop MoM. This decrease is mainly due to overproduction in the latter part of the season, driven by hotter temperatures, which has caused a significant fall in tomato prices both locally and for export. Additionally, a 6.8% reduction in Moroccan tomato exports to the EU from Sept-23 to May-24 has further impacted prices. This decline is part of a broader trend, with overall EU tomato imports down by 5.7% YoY IN the 2023/24 season.

Spain

In W35, Spain's wholesale tomato prices increased by 8.16% WoW, rising from USD 0.49/kg in W34 to USD 0.53/kg. This price hike is due to seasonal fluctuations, as the peak summer production period concludes and early autumn varieties are not fully available. Localized weather challenges, including intense heat waves and irregular rainfall, have negatively impacted tomato yields. The transition between growing cycles and extreme weather conditions has reduced overall production, increasing the prices. Despite this weekly rise, prices remain lower compared to the previous year and W34. Last year, strong export demand, particularly from Northern Europe and the Middle East, coupled with domestic supply constraints, drove higher local prices as exporters prioritized international contracts.

Turkey

In W35, Turkey's tomato prices held steady WoW at USD 0.80/kg but fell 11.11% MoM. The decline is due to an overproduction of tomatoes in 2024 and a persistent export ban on tomato paste, which has led to a surplus and reduced prices. Despite this, prices have risen by 37.93% YoY due to drought conditions worsened by climate change, severely impacting agricultural output and increasing diesel fuel and transport costs. These issues have led to frequent protests by farmers in provinces such as Bursa, Kahramanmaras, Balikesir, Aksaray, and Nigde. In Gaziantep, some farmers have protested by dumping unsold tomatoes on the road, drawing attention to their economic hardships, rising costs, and declining profits amid inflation.

France

In W35, tomato prices in France fell by 6.54% WoW, dropping from USD 1.53/kg to USD 1.43/kg. After a difficult start to the season, the French tomato market is beginning to recover, with increased consumption and moderated production. However, forecasted high temperatures across Europe will likely lead to additional production losses and potential price increases. This trend is expected to continue, especially in the Mediterranean region, where extreme heat could further affect tomato crops grown in tunnels, shelters, or open fields.

3. Actionable Recommendations

Adapt to Seasonal and Climatic Challenges through Flexible Pricing and Production Practices

The varied tomato price trends in Spain and Turkey underscore the importance of adaptable pricing and production practices. In Spain, the recent increase in wholesale prices, driven by seasonal fluctuations and weather challenges, indicates the need for flexible pricing models and optimized production practices. Spanish producers should focus on managing supply and demand effectively through these adaptable strategies. Similarly, in Turkey, the impact of overproduction and climate-related issues necessitates flexible pricing and improved production techniques. Addressing these challenges can help stabilize prices and support farmers experiencing economic hardships. By adopting flexible strategies to cope with seasonal and climatic variations, producers in Spain and Turkey can better navigate market fluctuations and ensure more stable production and pricing.

Capitalize on Price Fluctuations for Strategic Market Positioning

In light of the price fluctuations observed in Mexico and Morocco, strategic market positioning can be a practical approach. For Mexico, where tomato prices have remained high but experienced a recent MoM drop, enhancing production efficiency and exploring new export opportunities can help stabilize prices and capture market share. Similarly, Morocco, facing price declines due to overproduction and reduced EU exports, should capitalize on its competitive pricing to expand into new markets and strengthen trade agreements. By leveraging price fluctuations and adopting strategic market positioning, Mexico and Morocco can better manage market dynamics and enhance global competitiveness.

Diversify Supply Sources and Build Strategic Trade Relationships

Israel’s tomato crisis highlights the need for diversifying supply sources and building strategic trade relationships. With disruptions in supply from Turkey and Jordan, and the Gaza Strip relying on international aid, Israel’s decision to temporarily expand the duty-free import quota for tomatoes is a step towards mitigating shortages. To further address supply issues, Israel should explore additional trade partnerships and diversify import sources beyond Europe. Building relationships with tomato-producing countries in the Middle East and Southeast Asia could provide alternative supply channels and reduce vulnerability to disruptions. Strengthening strategic trade relationships will enhance supply chain stability and ensure a more reliable tomato supply.

Sources: Tridge, Agro Times, East Fruit, Canal Rural, Agraria , Fresh Plaza