In W4 in the apple landscape, some of the most relevant trends included:

- Weather conditions continue to play a crucial role in shaping apple yields globally. Apple production in Poland declined due to frost and hail damage, while South Africa’s recovery from previous hail and flood damage contributed to improved supply.

- In India, Kashmir apple growers accelerated releases from CA storage due to strong demand, while Moldova faces sluggish exports despite high stocks, with rising electricity costs adding pressure. Storage management remains a key factor in market dynamics.

- Driven by increased production and strong varietal performance, South Africa’s apple exports are expected to grow in 2025. Moldova seeks opportunities in the EU market amid domestic stock pressures. Apple prices showed mixed trends—rising in Italy and the US due to stable demand and tighter supply, while South Africa and Uruguay saw price drops due to increased supply. In Chile, prices rose MoM but declined YoY as supply normalized.

- The US apple market experiences steady demand for premium varieties like Honeycrisp and Evercrisp, while Poland sees surging juice concentrate prices amid reduced production. European apple exports continue to face competitive pressures.

1. Weekly News

Chile

Chile Introduces Geneva Rootstock to Boost Apple Orchard Productivity and Competitiveness

The introduction of the Geneva rootstock in Chile aims to enhance the productivity and competitiveness of apple orchards, particularly in older plantations, which make up 27% of the national total. This rootstock enables replanting in used soils, is resistant to woolly aphids, and boosts yields in high-density orchards. Leading Chilean company in premium fresh fruit production and export AgroPacal has leveraged the rootstock to improve apple volume, quality, and size through strategic varietal replacements. This marks a significant advancement for the industry.

India

Kashmir Apple Growers Accelerate Early Releases Due to Strong Demand

Driven by rising demand across India, apple growers in Kashmir have started releasing their produce from Controlled Atmosphere (CA) storage units earlier than usual. While shipments typically begin in mid-February, this year’s dispatches started in early Jan-25 due to favorable market conditions. Standard apple boxes are currently selling for USD 15 per 10 kilograms (kg) to USD 18/10 kg, while larger boxes are fetching USD 21/16 kg to USD 24/16 kg. In Oct-24, cold storage units in Pulwama and Shopian were filled as growers stored apples in anticipation of better prices. Last year, around 20% of stored apples went unsold due to increased imports, but this season has started more optimistically. With over 40 cold storage units, Kashmir produces more than 2 million metric tons (mmt) of apples annually. Growers stress the need for expanding storage infrastructure to stabilize supply chains and market prices.

Moldova

Moldova Faces Slow Apple Exports Despite High Stocks

Moldova's apple exports have been sluggish despite substantial stock levels, with just over 6 thousand tons shipped in Dec-24, far below pre-holiday norms and previous years' figures. From July 1 to December 31, 2024, approximately 37 thousand tons of apples from the 2024 harvest were exported, while 220 thousand tons were directed toward concentrate production, falling short of earlier forecasts. As of mid-Jan-25, an estimated 150 thousand to 160 thousand tons remain in storage, but rising electricity costs and energy market uncertainty are adding pressure. Experts predict that 10 thousand to 15 thousand tons may be processed, and 20 thousand to 25 thousand tons will be consumed domestically, leaving 100 thousand to 120 thousand tons for export over the next five months. Moldova's ability to sustain monthly exports of 20 thousand to 25 thousand tons remains uncertain, though a mild apple shortage in some European Union (EU) markets could present opportunities.

Poland

Poland's Apple Production Declines Due to Frost and Hail Damage

Poland's 2024 apple production is estimated at nearly 3.4 mmt, reflecting a 13.1% year-on-year (YoY) decline due to severe frost damage to flower buds in late April and early May, compounded by hailstorms in May. Despite this drop, the estimate exceeds the World Apple and Pear Association’s (WAPA) initial forecast of 3.2 mmt. Additionally, apple concentrate production is expected to fall to around 220 thousand metric tons (mt) for the 2024/25 marketing year, down from 255 thousand mt in 2023/24. Meanwhile, prices for high-acidity apple juice have surged by 43.2% YoY to USD 2,759.22/mt (EUR 2,650/mt), while medium-acidity juice has risen by 22.5% YoY to USD 2498.92/mt (EUR 2,400/mt). However, trading activity remains subdued as buyers have secured short-term supplies, with a potential market rebound expected by mid-Feb-25.

South Africa

Increased Production and Strong Varietal Performance Drive South Africa's Apple Export Growth in 2025

South Africa's 2024 apple export season concluded, reaching 48.6 million equivalent cartons (12.5 kg), a 12% YoY increase. South Africa's apple exports for the 2025 season are projected to rise by 5% YoY, driven by increased production from young orchards, higher-yielding varieties, and favorable weather conditions following recovery from the 2023 hail and floods. The forecasted growth is primarily attributed to bi-colored apples such as Royal Gala/Gala (+6%), Cripps Pink/Pink Lady (+7%), and Bigbucks/Flash Gala (+24%), along with a strong outlook for Cripps Red/Joya varieties (+9%). With excellent fruit quality and new hectares (ha) coming into production, South Africa’s apple export sector is well-positioned for continued success.

United States

Steady Demand for Michigan Apples Despite Lower Production

Apple demand in Michigan remains stable, although overall United States (US) consumption is gradually declining as consumers turn to other fruit options. Michigan's apple volume is down 15% YoY but remains 20% above the five-year average due to increased bearing surfaces and younger plantings reaching full potential. The 2024/25 season has seen a smaller Eastern US apple crop, with Honeycrisp production notably lower due to its biannual bearing cycle. Golden Delicious volumes in Michigan have also declined due to strong early-season processing demand, reducing its availability. Despite an initial surplus that led to promotions in late summer and early fall, apple prices have strengthened as supply tightens, with further market adjustments expected in spring.

Uruguay

Apple Prices Decline Due to Increased Supply in Uruguay

In Uruguay, apple prices at the Metropolitan Agri-Food Unit (UAM) dropped from USD 2.28/kg to USD 2.19/kg (UYU 99/kg) to (UYU 95/kg) over the past week, driven by a 28% YoY reduction in sales volume. This decline is linked to the arrival of new harvest batches, the continued sale of stock from the previous season, and increasing competition from imports, leading to price variations. Apples now account for 4.7% of total sales at the UAM, reflecting the shifting market demand dynamics. While newly harvested apples influence prices, concerns about quality and maturity due to weather conditions further impact local competitiveness.

2. Weekly Pricing

Weekly Apple Pricing Important Exporters (USD/kg)

Yearly Change in Apple Pricing Important Exporters (W4 2024 to W4 2025)

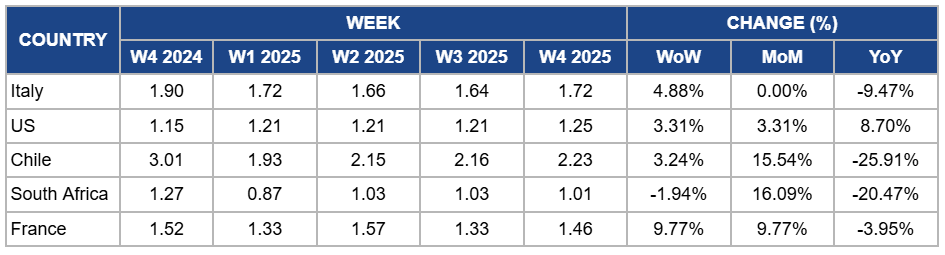

Italy

Italy's apple prices increased by 4.88% week-on-week (WoW) to USD 1.72/kg in W4, with no month-on-month (MoM) change due to stable supply levels and consistent demand for apples during the period. However, there is a 9.47% YoY decline due to the ongoing effects of a high supply from the extended harvest season, which has kept prices lower than last year. The previous year's prices were relatively higher due to stronger post-holiday demand and a more constrained supply. Additionally, competition from other European apple producers has continued to exert downward pressure on prices, contributing to the YoY decrease.

United States

In W4, apple prices in the US increased slightly by 3.31% WoW and MoM to USD 1.25/kg in W4, showing an 8.7% YoY increase due to sustained demand for premium varieties like Honeycrisp and Evercrisp, which have continued to support higher market prices. The increase in prices is also due to the tighter supply conditions resulting from a smaller national apple crop in 2024/25, particularly the decline in Honeycrisp production due to its biannual bearing cycle. Additionally, reduced volumes of Golden Delicious due to strong early-season processing demand have further tightened supply, reinforcing upward price pressure. Limited international availability and ongoing export challenges have also contributed to the price increase, as market dynamics remain influenced by these factors.

Chile

Apple prices in Chile increased by 3.24% WoW to USD 2.23/kg in W4, reflecting a 15.54% MoM increase due to steady demand from local and international markets, combined with strong export activity. The price rise is also due to the continued tightening of supply, as inventory levels remain under pressure to meet market needs, particularly for premium apple varieties. Additionally, favorable conditions for high-density orchards and the use of Geneva rootstock have contributed to higher-quality production. However, YoY prices dropped by 25.91% due to the normalization of production levels and supply conditions. This followed the exceptionally high prices seen in 2023, which were caused by severe global supply shortages and elevated demand. This YoY decline reflects the market’s adjustment to a more balanced supply-demand dynamic.

South Africa

South Africa's apple prices dropped by 1.94% WoW to USD 1.01/kg in W4. This marked a 20.47% YoY drop, influenced by high prices in the same period last year due to supply constraints from adverse weather events and lower production volumes. However, MoM prices surged by 16.09% due to the positive impact of increased production, driven by young orchards reaching full production and higher-yielding apple varieties. The recovery from the 2023 hail and flood damage, along with more favorable weather conditions, has strengthened supply, leading to a rise in prices compared to the previous month.

France

In France, apple prices increased by 9.77% WoW and MoM to USD 1.46/kg in W4 due to a seasonal reduction in supply, with improved quality and the availability of stored apples, which stimulated local and European market demand. The upward pressure on prices was further supported by stronger demand following the post-holiday season. However, YoY prices dropped slightly by 3.95% due to reduced demand and lower export volumes, particularly to third countries, reflecting the continued decline in exports compared to the previous year.

3. Actionable Recommendations

Adjust Apple Supply Strategy to Stabilize Market Impact

Michigan apple growers should adjust harvest schedules to better align with market demand, focusing on varieties with higher consumer interest. Strengthening partnerships with processors and retailers for consistent distribution can help manage supply fluctuations, particularly with the reduced availability of Golden Delicious and Honeycrisp apples. Additionally, growers should explore targeted promotions for premium varieties to maintain price stability as market conditions evolve.

Adapt Apple Production Strategy for Market Stability

Poland's apple producers should prioritize diversifying production by focusing on more resilient apple varieties to mitigate frost and hail damage. They should also optimize harvest timing to balance supply with current market demand while exploring new export markets to offset domestic declines. Growers should collaborate with juice processors to manage the decrease in concentrate production and adjust pricing strategies to align with market conditions.

Sources: Tridge, Agroexpert, Eastfruit, Freshplaza, Hortgro, KashmirLife, Mintec/Expana, Portaldelcampo