.jpg)

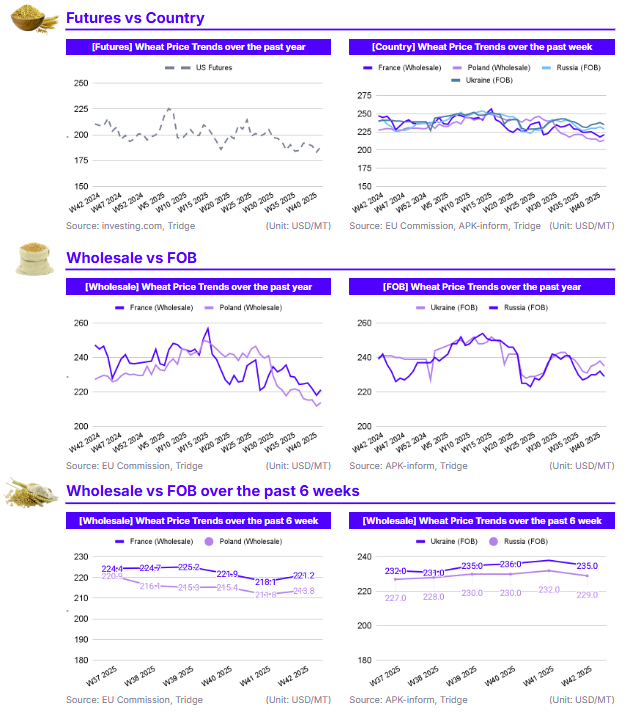

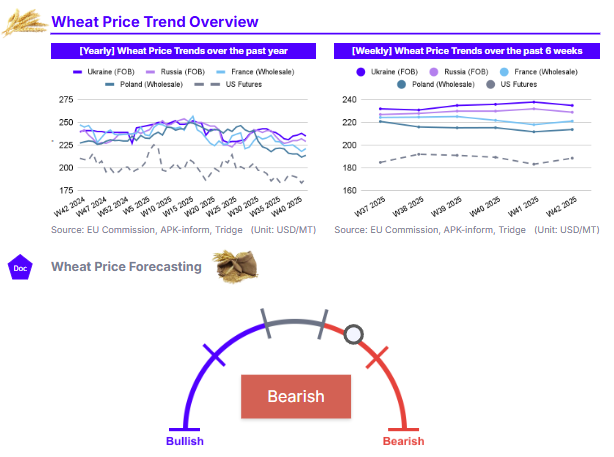

In W42, US and European prices rebounded week-on-week (WoW), with US Futures closing at USD 188.5/mt and French wholesale at USD 221.2/mt. Conversely, Black Sea prices declined, with Russian Free on Board (FOB) at USD 229.0/mt and Ukrainian FOB at USD 235.0/mt. This weekly movement, however, exists within a broader bearish trend. All major markets remain down significantly year-on-year (YoY), including the US (-10.43%) and France (-10.54%). This is driven by a global supply glut, confirmed by the USDA’s September WASDE report, which raised 2025/26 global supply and ending stock projections. Given the ample EU production (142 mmt), European buyers are advised to capitalize on regional price differences by sourcing from Poland (USD 213.8/mt), which is more competitive than France.

1. Weekly Price Overview

Western Wheat Prices Rebound as Black Sea Markets Dip

In W42, wheat prices in the United States and Europe recovered from recent lows, while Black Sea export prices declined. In the US, Wheat Futures saw the sharpest rise, closing at USD 188.5 per metric ton (mt), up 2.91% WoW. European prices followed this trend. In France, the wholesale price was USD 221.2/mt, a 1.45% increase WoW, and Poland’s wholesale price rose 0.96% WoW to USD 213.8/mt. This upward correction in the West comes after a period of sustained price drops and is likely supported by high anticipated exports, particularly for France, which anticipates a surge in exports to Morocco.

Conversely, Black Sea prices fell. The Russian Free on Board (FOB) price was USD 229.0/mt, down 1.29% WoW, while the Ukrainian FOB price saw a similar 1.26% WoW decrease to USD 235.0/mt. The downward pressure is likely linked to increased supply in the face of decreased exports in the region. Both Ukraine and Russia have reported decreased export volumes in 2025. Furthermore, the agricultural consultancy SovEcon recently increased its 2025 harvest forecast for both Russia and Ukraine, adding to supply-side pressure.

2. Price Analysis

Bearish Global Outlook Solidifies as Estimates Confirm Higher Global Production and Stocks

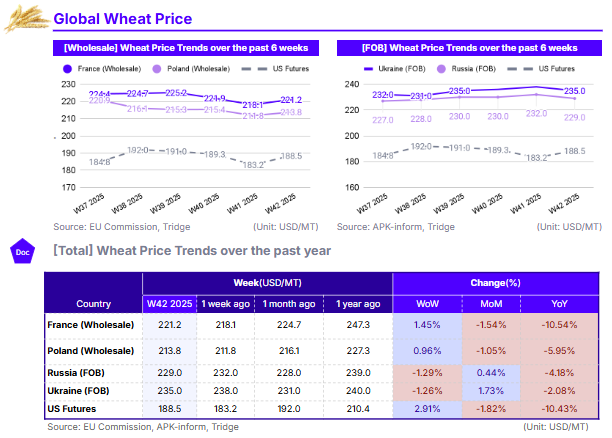

In W42, long-term price trends show significant downward pressure compared to the previous year across all major markets. In the US, Wheat Futures stood at USD 188.5/mt, down 1.82% month-on-month (MoM) and 10.43% YoY. This bearish trend was mirrored in France, where wholesale prices were USD 221.2/mt, reflecting a 1.54% MoM and 10.54% YoY decline. Poland’s price was USD 213.8/mt, down 1.05% MoM and 5.95% YoY. Even the Black Sea, which saw recent monthly gains, remained down compared to last year. Russia's Free on Board (FOB) price was USD 229.0/mt (+0.44% MoM, -4.18% YoY), and Ukraine's FOB price was USD 235.0/mt (+1.73% MoM, -2.08% YoY).

This widespread YoY price decline is underpinned by a fundamentally bearish global supply outlook, as confirmed by the USDA’s September 2025 WASDE report and recent International Grains Council (IGC) estimates. The USDA report revised the 2025/26 global wheat outlook upwards, forecasting higher supplies, consumption, and, critically, higher ending stocks. Global supplies are projected to increase by 9 million metric tons (mmt) , driven by larger production estimates for several major exporters. Production was raised for Australia (+3.5 mmt) , the EU (+1.9 mmt) , Russia (+1.5 mmt) , as well as Canada and Ukraine. This influx of wheat onto the global market has led the USDA to raise its projection for 2025/26 global ending stocks by 4 mmt to 264.1 mmt. This increase in available stocks is placing significant downward pressure on prices compared to the previous year.

3. Strategic Recommendations

European Buyers Should Leverage Ample EU Supply by Sourcing Competitively Priced Polish Wheat

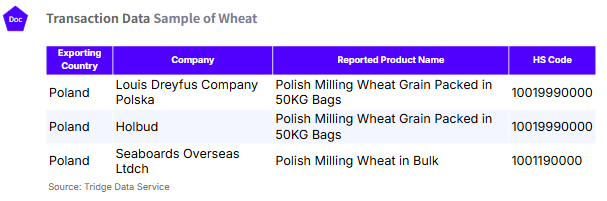

European wheat buyers are currently operating in a well-supplied regional market. The EC forecasts the 2025 EU wheat production at 142 mmt, a volume 8% above the five-year average. This strong regional supply is a key driver behind the significant YoY price declines seen across the bloc, including in France (-10.54% YoY) and Poland (-5.95% YoY) as of W42. Within this high-supply environment, European buyers should focus on intra-EU procurement strategies to maximize cost-efficiency. Poland currently presents the most compelling origin. As of W42, Polish wholesale wheat is priced at USD 213.8/mt. This offers a clear cost advantage over France, the largest wheat producer in the EU, where prices are higher at USD 221.2/mt. This procurement strategy is low-risk, as Poland’s price advantage is supported by secure fundamentals. Its harvest is expected to be on par with the five-year average, ensuring ample exportable supplies. Buyers should capitalize on this combination of supply security and a distinct price discount to manage procurement costs effectively. According to Tridge Eye transaction data, the Louis Dreyfus Company Polska, Holbud, and Seaboards Overseas and Trading Group are exporters of grain from Poland in recent months.