In W10 in the tomato landscape, some of the most relevant trends included:

- French and Moroccan producers are set to finalize an agreement in mid-Mar-25 to regulate Moroccan cherry tomato imports into France. The deal aims to ease competition at the start of the French season while maintaining Morocco's complementary supply role. Advances in Moroccan greenhouse production and lower costs have intensified market competition, prompting the need for regulatory commitments.

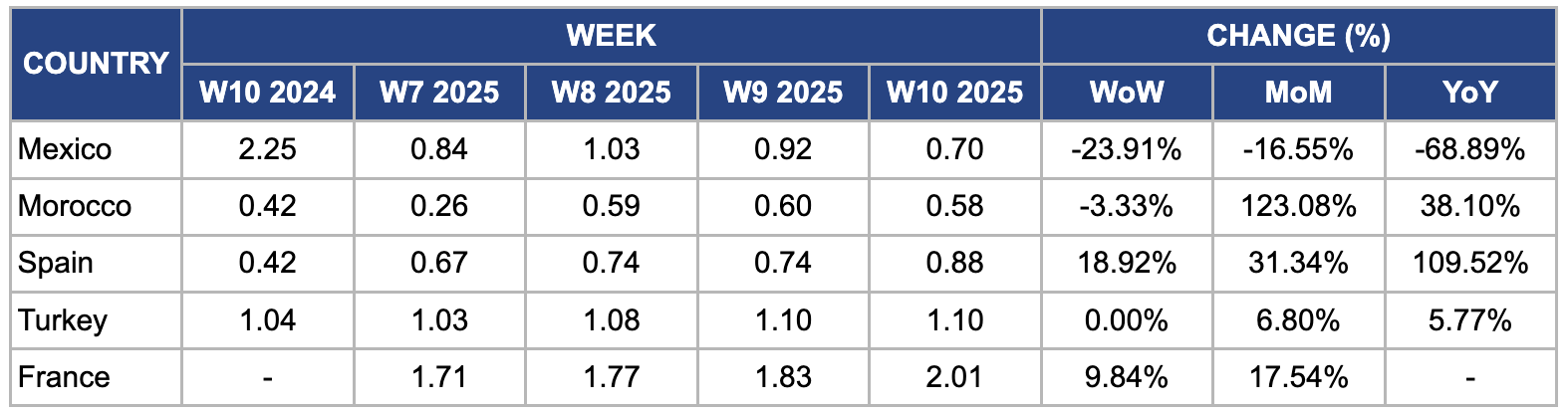

- Mexico's tomato prices plummeted due to oversupply, worsened by a new 25% US tariff. Meanwhile, Spain’s tomato prices surged due to cold weather slowing harvests. Morocco’s prices fell WoW due to improved supply but remained significantly higher MoM. Türkiye's and France’s tomato prices rose due to strong export demand and seasonal consumption shifts.

- The NATPAN has called for government intervention to curb post-harvest losses in Nigeria. Smallholder farmers struggle with infrastructure and financial limitations, requiring storage investment, processing, and transportation to stabilize Nigeria’s tomato supply chain.

1. Weekly News

Morocco

Morocco-France Tomato Agreement Expected in March to Regulate Cherry Tomato Market

Moroccan and French tomato producers are expected to finalize a bilateral agreement in mid-Mar-25 to regulate Moroccan cherry tomato imports into France, aiming to ease competition with local production at the start of the French season. Moroccan tomatoes have historically complemented French supply during the off-season. However, advances in Moroccan greenhouse production and lower costs from cheaper labor and desalinated seawater irrigation have intensified market competition. This has led to tensions, as Moroccan cherry tomatoes now enter the French market earlier in the season at more competitive prices.

The agreement, initiated by both countries’ agriculture ministries, will formalize seasonality commitments. It follows discussions at key events, including the Meknès Agricultural Fair (Apr-4) and the Paris Agricultural Fair (Feb-25).

Nigeria

NATPAN Urged FG Action to Curb Tomato Post-Harvest Losses in Nigeria

The National Tomato Growers, Processors, and Marketers Association of Nigeria (NATPAN) has urged the federal government to curb post-harvest losses in the tomato sector. According to the NATPAN Chairman, smallholder farmers lack the necessary infrastructure and financial resources to minimize spoilage and improve value addition. Increased government intervention, including storage investments, processing, and transportation, is critical to reducing losses and improving Nigeria’s tomato supply chain.

Philippines

Tomato Prices in Mangaldan Declined in W9 Due to Oversupply

Tomato prices in Mangaldan Public Market have fallen to USD 0.17 per kilogram (kg) in W9, down from USD 0.35/kg in previous weeks, due to an oversupply and weak demand. Vendors are struggling to sell their stock, with many tomatoes turning overripe and unsold. At the farm gate level, prices have dropped to USD 0.070 to 0.087/kg, forcing some farmers to sell at a loss. Simultaneous harvesting across the province has intensified the glut. However, prices are expected to stabilize by Mar-25 as supply levels normalize.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W10 2024 to W10 2025)

Mexico

In W10, Mexico's tomato prices plummeted 23.91% week-on-week (WoW), 16.55% month-on-month (MoM), and 68.89% year-on-year (YoY) to USD 0.702/kg. This sharp decline is mainly due to higher domestic production, particularly in Sinaloa, which contributes 22% of national output. Favorable growing conditions have boosted yields, leading to oversupply and downward price pressure. Moreover, the global processing tomato production is expected to fall 11.5% YoY in 2025, which could introduce market volatility and future price fluctuations. Meanwhile, the recent 25% tariff imposed on Mexican tomato exports to the United States (US) may have redirected surplus supply into the domestic market, further intensifying the price drop.

Morocco

In W10, Morocco's tomato prices declined 3.33% WoW and surged 123.08% MoM to USD 0.58/kg. The weekly decline was primarily due to improved supply as favorable weather conditions supported higher production, increasing market availability. Moreover, exporters ramped up shipments to the European Union (EU), easing domestic price pressure. Improved logistical conditions also contributed to the decline, ensuring a more stable flow of tomatoes to local and international markets. However, the sharp 123.08% MoM increase reflects the lingering effects of earlier supply constraints and strong European demand, pushing prices higher in Feb-25.

Spain

In W10, Spain's tomato prices increased 18.92% WoW, 31.34% MoM, and 109.52% YoY to USD 0.88/kg. The price surge is mainly due to adverse weather conditions in Almería and Murcia, where cold temperatures in Feb-25 daytime averages of 17 to 19°C and nighttime lows of 7 to 9°C slowed plant growth and delayed harvests, tightening market supply. In Mar-25, persistent supply constraints kept prices elevated, although a gradual improvement in weather conditions was observed. The Spanish State Meteorological Agency (AEMET) reported a warming trend, with temperatures rising to 22 to 24°C, improving growing conditions for better harvesting. However, market stabilization remained uncertain due to prior disruptions.

Türkiye

In W10, Türkiye's tomato prices remained unchanged WoW but increased 6.80% MoM to USD 1.10/kg. This price rise is primarily driven by strong export demand, as Türkiye's tomato exports reached USD 536 million in 2023 and continue to grow. The tightened domestic supply due to heightened international demand has exerted upward pressure on prices. Moreover, the Turkish tomato market expanded modestly to USD 8.7 billion in 2024, reflecting a 3.5% YoY increase, signaling robust domestic consumption alongside export growth.

France

In W10, France's tomato prices increased 9.84% WoW and 17.54% MoM to USD 2.01/kg from USD 1.83/kg. This marks a turning point for the market after a month of weak prices in Feb-25 due to sluggish demand. However, market conditions reversed sharply in W8, driven by revived demand. Factors such as the start of the month, schools reopening, improving weather, and a shift toward spring produce have all contributed to higher tomato consumption. Some retail chains are already transitioning to French-grown tomatoes, further boosting demand. With supply struggling to keep up, producers are looking to raise prices in response to the market rebound.

3. Actionable Recommendations

Implement Targeted Supply Management Strategies

Oversupply in markets like Mexico and the Philippines has led to sharp price declines, while Spain and France are struggling with supply shortages. To address this imbalance, producers in Mexico and the Philippines should adopt staggered planting schedules and coordinated harvest timelines to prevent seasonal gluts that crash prices. Meanwhile, in Spain and France, greenhouse expansion and adopting climate-resilient tomato varieties can help stabilize production during colder months, reducing reliance on imports. Moreover, exporters from high-production regions should diversify target markets and explore alternative destinations to avoid excess supply accumulating in domestic markets, ensuring more stable pricing.

Enhance Post-Harvest Infrastructure and Processing Capacity

Moroccan exporters should work on negotiating flexible export schedules with EU buyers, allowing shipments to align with demand fluctuations and avoiding domestic oversupply. Mexican tomato producers should diversify export markets by targeting regions such as Canada, Japan, and the Middle East to reduce reliance on the US market. In Europe, French and Spanish retailers should consider expanding forward contracts with local producers to secure supply at stable prices, reducing exposure to price volatility and import reliance.

Adjust Trade and Pricing Strategies to Market Conditions

High post-harvest losses in Nigeria and the Philippines significantly reduce farmer earnings and create inefficiencies in the supply chain. To mitigate this issue, investments in cold storage networks and processing facilities are essential to extend the shelf life of fresh tomatoes and reduce wastage. Governments and private investors can establish public-private partnerships (PPPs) to develop affordable logistics solutions, such as solar-powered storage units and mobile processing plants that can reach rural farming communities. Furthermore, encouraging contract farming with processors will help ensure steady demand, allowing farmers to sell their produce at predictable prices rather than relying on volatile fresh markets.

Sources: Tridge, East Fruit, Tomato News