In W17 in the peanut landscape, some of the most relevant trends included:

- Argentina’s 2023/24 peanut production is expected to rebound by 64% to 1.20 mmt, driven by improved yields and later planting, despite a smaller planted area. Córdoba remains the dominant producing region, contributing 87% of national output.

- Recovering from historic lows in Oct-23, global peanut prices rose 16% in Mar-25 to USD 1,272/mt due to tight supply and growing demand, especially from European buyers of Argentine peanuts.

- In Goa, India, peanut farmers reported severe crop failure in the 2024/25 Rabi season due to the non-germinating seeds distributed by government agencies, prompting demands for compensation and stricter seed quality oversight.

- The Southern Peanut Farmers Federation expanded in 2024 to include South Carolina, unifying representation for Southeastern US growers responsible for 73% of national output and promoting stronger industry collaboration.

1. Weekly News

Argentina

Córdoba Peanut Sector Shows Production and Price Recovery

Córdoba, Argentina's key peanut-producing region, is forecast to see a 64% increase in production for the 2023/24 season, with an estimated 1.20 million metric tons (mmt) expected, following a drought-impacted previous year. This recovery is attributed to improved yields and later planting, though the planted area was 6% lower than the five-year average. Córdoba accounts for 87% of Argentina's peanut production, with significant contributions from departments like Río Cuarto and Juárez Celman.

International peanut prices, which hit a historic low in Oct-23, have started to recover, reaching USD 1,272 per metric ton (mt) in Mar-25, a 16% increase from Feb-25. This rise is fueled by limited supply from major exporters and increased global demand, particularly from Europe, which remains the largest buyer of Argentine peanuts. While expected yields are strong, concerns remain over the impact of Mar-25 rains on grain quality. Despite this, the improved production and rising prices provide a positive outlook for the sector, offering potential foreign currency inflows for Argentina’s agro-industrial economy.

India

Peanut Farmers in Goa Report Major Losses Due to Faulty Seed Distribution

Peanut farmers in Goa, particularly in Sangolda, have reported severe crop losses during the 2024/25 Rabi season due to non-germinating high-yielding seeds provided by the Agriculture Department's Zonal Agricultural Office in Mapusa. Despite paying USD 70.45 per kilogram (INR 6,000/100 kg) and investing heavily in land preparation and inputs, affected farmers saw no returns. In contrast, seeds sourced from the open market performed well, raising concerns about the quality and suitability of government-distributed varieties.

Farmers have lodged complaints seeking compensation and called for a formal inquiry. They stress the urgent need for the Department to conduct local field trials and demonstrations before distributing new seed varieties, especially in regions with limited irrigation infrastructure. With Rabi being the primary earning season, farmers argue that such oversight has led to avoidable financial distress.

United States

Southern Peanut Farmers Federation Expands to Include South Carolina

The Southern Peanut Farmers Federation (SPFF) has officially welcomed the South Carolina Peanut Board as its newest member, joining Alabama, Florida, Georgia, and Mississippi. This expansion strengthens the Federation’s representation of peanut growers across five Southeastern states, which collectively produce 73% of the United States (US) peanut crop. In 2024, growers in these states achieved an average yield of 3,560 pounds (lbs) per acre. Leaders from South Carolina and Georgia emphasized the move as a significant step toward greater industry unity, advocacy, and collaboration.

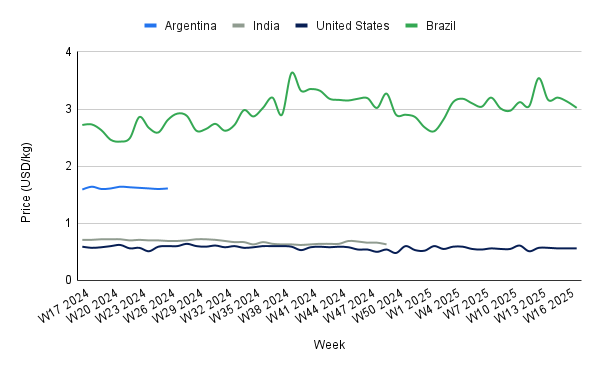

2. Weekly Pricing

Weekly Peanut Pricing Important Exporters (USD/kg)

Yearly Change in Peanut Pricing Important Exporters (W17 2024 to W17 2025)

United States

US peanut prices held steady at USD 0.56 per kilogram (kg) in W17, reflecting a modest decline of 1.75% month-on-month (MoM) and 5.08% year-on-year (YoY) from USD 0.59/kg. The downturn is largely due to strong production expectations, with early planting underway in South Georgia, one of the nation's top peanut-producing regions, spurred by favorable weather and reduced competitiveness of corn and cotton. The projected acreage increase to 950,000 acres suggests a potential surge in supply, which may apply additional downward pressure on prices as the season progresses. Nonetheless, the market direction will remain sensitive to mid-season weather conditions and final yield performance, which could either reinforce or offset current bearish trends.

Brazil

In W17, Brazil's peanut prices fell to USD 3.02/kg, a 3.51% WoW decline, though still 11.03% higher YoY from USD 2.72/kg. This decrease reflects strategic export pricing amid the mid-harvest phase, which is delivering strong volumes and quality as of W17. However, persistent rainfall threatens to delay harvest progress and may reduce final output. The current price dip is largely tied to Brazil's efforts to regain international market share, particularly outside Europe, following a weak 2024 crop. This has led exporters to adopt aggressive pricing, increasing competitive pressure on suppliers like the US and Nicaragua. If adverse weather persists and disrupts harvest completion, reduced supply could drive prices higher in the medium term, counteracting short-term declines and reshaping global peanut trade dynamics.

3. Actionable Recommendations

Implement Strategic Quality Control for Seed Distribution Programs

In response to seed germination failures reported in Goa, Indian agricultural authorities should mandate localized field trials and validation of peanut seed varieties before mass distribution. Implementing stricter quality assurance protocols, such as third-party seed certification and performance benchmarks in regional conditions, can reduce the risk of widespread crop failure and protect farmer livelihoods during key seasons like Rabi.

Leverage Argentina's Production Recovery to Expand European Market Share

With Córdoba's production increase and strong European demand, Argentine exporters should secure long-term contracts with European buyers and promote traceable, high-quality peanuts. Investments in post-harvest processing to preserve grain quality amid weather risks, coupled with targeted marketing campaigns, can enhance competitiveness and foreign currency inflows.

Bolster Supply Chain Resilience Amid Global Weather Uncertainty

As unpredictable rainfall affects harvest timing and quality in Brazil and Argentina, peanut buyers and processors, particularly in Europe and Asia, should diversify sourcing portfolios to include suppliers from both hemispheres. Long-term agreements with producers in the US, Africa, and South America can mitigate risks and ensure a steady supply in the face of weather-driven market disruptions.

Sources: Tridge, AG Info, Herald Goa, Punto a Punto