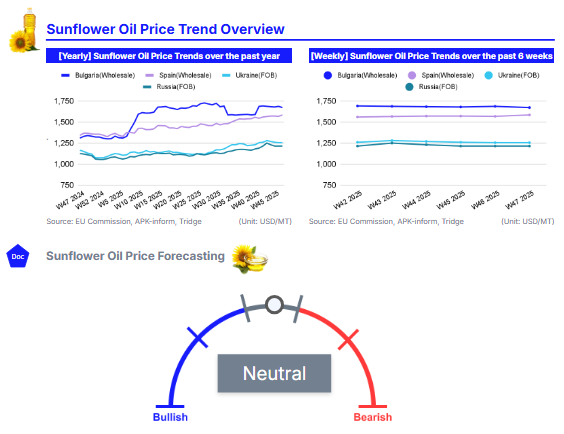

W47 2025: Sunflower Oil

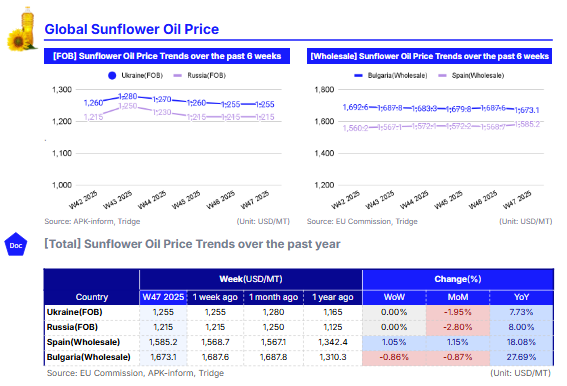

In W47 of 2025, global sunflower oil prices remained stable in the Black Sea region while showing mixed movement in the EU. Ukraine’s FOB price held at USD 1,255/mt, and Russia’s FOB price remained at USD 1,215/mt. EU wholesale markets diverged, with Spain rising 1.05% WoW to USD 1,585.2/mt and Bulgaria dipping 0.86% WoW to USD 1,673.1/mt. Despite weekly stability, the market remains structurally tight, with prices up significantly YoY: Bulgaria (+27.69%), Spain (+18.08%), Ukraine (+7.73%), and Russia (+8.00%). This bullish trend is underpinned by a decade-low harvest in Ukraine and the smallest EU crop in nine years. Russia remains the most cost-effective sourcing origin, though geopolitical and logistical risks persist. Tridge Eye’s transaction level data highlights Divo Altaya, Maslenitsa, and Yug Rusi as viable export partners in Russia.

1. Weekly Price Overview

Black Sea Prices Hold Firm While EU Wholesale Markets Show Divergence

In W47 of 2025, sunflower oil export prices in the Black Sea remained stable, extending the stable period experienced in recent weeks. Ukraine's Free on Board (FOB) price held steady at USD 1,255 per metric ton (mt), unchanged week-on-week (WoW). Similarly, Russia's FOB price remained flat at USD 1,215/mt. In the European Union (EU) wholesale market, price movements diverged slightly. Spain recorded a 1.05% WoW increase to USD 1,585.2/mt, while Bulgaria saw a minor decline of 0.86% WoW to USD 1,673.1/mt.

The stability in Black Sea export prices in recent weeks reflects a market finding equilibrium. While global vegetable oil markets have seen downward pressure, sunflower oil prices in Ukraine and Russia are supported by tight regional supply fundamentals. The Ukrainian harvest is nearing completion with yields projected to be the lowest in a decade due to a dry, hot summer, effectively capping any significant price drops. In the EU, Spain's price rise is underpinned by the broader European production deficit, with the total EU sunflower seed harvest expected to be significantly below the five-year average. Conversely, Bulgaria's slight dip suggests a localized adjustment, though prices remain historically high due to its own disappointing crop season marked by drought and late rains.

2. Price Analysis

Structural Deficits Keep Annual Prices High Despite Seasonal Cooling

In Russia, the price of sunflower oil decreased 2.80% month-on-month (MoM) to USD 1,215/mt, while maintaining an 8% year-on-year (YoY) increase. Ukraine followed a similar trend, falling 1.95% MoM to USD 1,255/mt, yet remaining 7.73% higher YoY. In the EU, movements were mixed. Spain saw a 1.15% MoM rise to USD 1,585.2/mt, contributing to an 18.08% YoY gain, whereas Bulgaria dipped 0.87% MoM to USD 1,673.1/mt but sustained a massive 27.69% YoY surge.

The monthly easing in Black Sea export prices reflects a market stabilizing following a momentary price rise during mid October 2025, influenced by harvest pressure in the form of delayed harvests. However, the robust annual price increases highlight the severe structural supply deficit underpinning the market. The USDA recently lowered its global sunflower seed production forecast by 1 million metric tons (mmt), citing reductions for Ukraine, Russia, and the EU.

Specifically, Oil World estimates the EU harvest to be the smallest in nine years, a shortfall that is driving the substantial premiums seen in Spain and Bulgaria. Similarly, Ukraine’s 7.73% YoY gain is driven by a decade-low harvest resulting from a hot, dry summer. While Russia’s production estimate was also cut by 0.5 mmt, its harvest remains substantial enough to keep its prices the most competitive in the group, although they are still supported by the broader regional tightness.

3. Strategic Recommendations

Russia's Price-Competitive Sunflower Oil Remains a Good Opportunity but Requires Careful Risk Management

For global buyers seeking to mitigate the high prices seen in the EU, Russia remains a key sourcing opportunity. In W47, Russia's FOB price held steady at USD 1,215/mt, reinforcing its position as the most competitive major exporter. This price stands significantly below Ukraine's (USD 1,255/mt) and especially EU wholesale levels in Bulgaria (USD 1,673.1/mt) and Spain (USD 1,585.2/mt). This price advantage is supported by strong supply fundamentals. While Ukraine faces its lowest harvest in a decade and the EU suffers a nine-year low in production, Russia's 2025 harvest remains substantial despite minor downward revisions. This combination of the lowest price and ample volume availability makes it an attractive option for importers.

However, buyers must balance this opportunity with the significant geopolitical and logistical risks involved. Sourcing from a nation engaged in an active war carries inherent uncertainties, including potential disruptions to Black Sea port operations, high insurance premiums, and complex payment channels. Therefore, importers considering Russia should conduct thorough due diligence on their logistics partners and secure comprehensive cargo insurance. Tridge Eye’s transaction level data highlights Divo Altaya, Maslenitsa, and Yug Rusi as viable export partners in Russia.