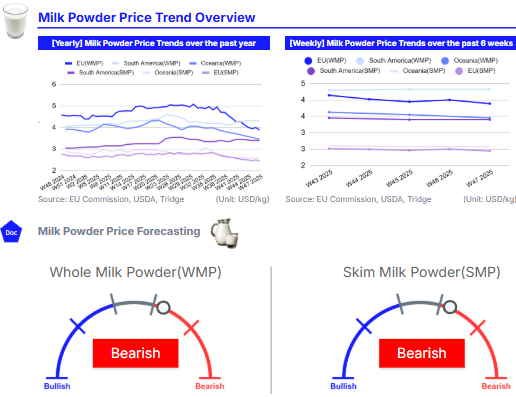

In W47, global milk powder markets showed mixed trends, with EU and Oceania WMP and SMP prices declining due to steady production, cautious short-term demand, and competitive pricing. On the other end, South American WMP rose slightly, supported by exports from Argentina and Uruguay. The November 18 GDT auction confirmed the softening trend, with WMP and SMP down 1.9% and 0.6%, respectively, from the previous auction. However, North Asia led purchases for both WMP and SMP commodities. In the US, milk powder production was modest and exports subdued. Key strategies include shifting EU and Oceania output toward higher-value or specialty powders and securing forward contracts and storage to manage inventory. Additionally, South American producers should prioritize WMP production for exports, while US producers can mitigate price volatility through hedging and aligning production schedules with demand.

1. Weekly Price Overview

Rising Milk Output and Cautious Demand Push WMP and SMP Prices Lower

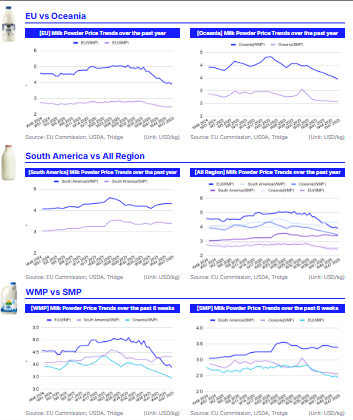

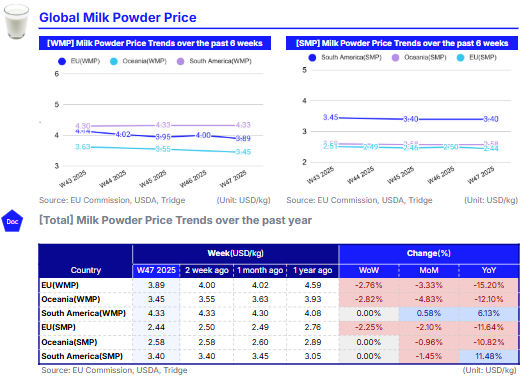

In W47, European Union (EU) whole milk powder (WMP) prices averaged USD 3.89 per kilogram (kg), reflecting a 2.76% week-on-week (WoW) drop, a 3.33% month-on-month (MoM) decline, and a 15.20% year-on-year (YoY) fall. The decrease was driven by sellers trimming offers to remain competitive amid steady production, limited export interest, and demand focused on near-term needs. Similarly, EU skimmed milk powder (SMP) averaged USD 2.44/kg, down 2.25% WoW, 2.10% MoM, and 11.64% YoY. This could be attributed to buyers remaining cautious, prioritizing immediate coverage and avoiding longer-term positions. Production continues steadily, supported by consistent milk intakes, while spot availability sufficiently meets current requirements.

In Oceania, WMP prices fell to USD 3.45/kg, a 2.82% WoW decline, 4.83% MoM drop, and 12.10% YoY fall, reflecting lower domestic pricing amid the peak of milk output and active WMP production. SMP prices averaged USD 2.58/kg, largely unchanged from the previous price, though still 0.96% lower MoM and 10.82% below last year. Production remains strong due to abundant milk supplies during the spring flush, while demand stays short-term focused. However, producers are beginning to secure forward contracts for Q1-2026 and Q2-2026, supporting longer-term sales.

In South America, WMP prices averaged USD 4.33/kg, remaining stable from the previous week but rising 0.58% MoM and 6.13% YoY. This was largely supported by export demand from Argentina and Uruguay, despite Brazil’s exports declining for 2025. SMP averaged USD 3.40/kg, stable from the previous week, down 1.45% MoM but 11.48% higher YoY. Manufacturers are prioritizing WMP production by utilizing more cream from milk loads, resulting in tight spot inventories, though some supply remains available in the market.

2. Price Analysis

Steady Production and Focused Demand Influence Global Milk Powder Trends

The fortnightly Global Dairy Trade (GDT) auction on November 18 recorded a softer outcome, with the average winning price falling 3% from the previous event to USD 3,678 per metric ton (mt). Most major commodities registered declines, including WMP, which dropped 1.9% to USD 3,452/mt, and SMP, down 0.6% to USD 2,542/mt. Despite the overall softening, WMP demand remained relatively strong, led by North Asia, which purchased 52% of available products, followed by the Middle East at 24%. For SMP, North Asia accounted for 63% of total purchases, increasing its share of demand compared to previous auctions.

In South America, demand in Brazil for WMP is moderate, with most Nov-25 requirements already met. Elsewhere in the region, demand ranges from steady to stronger. SMP producers are increasingly directing milk solids toward WMP production by utilizing more cream in milk loads, reflecting a strategic focus on higher-value output.

In the EU, WMP demand remains near-term focused, with production steady and export interest limited. SMP demand continues to be cautious, as buyers prioritize immediate coverage and avoid longer-term commitments. Production is supported by consistent milk intakes, and spot availability sufficiently meets current requirements.

In the United States (US), milk powder production remains relatively subdued, though volumes increased slightly in Aug-25. Combined output of nonfat dry milk (NDM) and SMP totaled 165.1 million pounds (lbs), up 0.9% YoY. However, milk powder exports weakened, falling 17.6% YoY to 124.4 million lbs, indicating continued pressure on US producers from both domestic and international markets.

3. Strategic Recommendations

Strategic Shifts Key as WMP and SMP Prices Show Divergent Regional Trends

In the EU and Oceania, where WMP and SMP prices are declining due to steady production and near-term-focused demand, processors should shift output toward higher-value products such as specialty powders, fortified milk powders, or niche dairy ingredients. Implementing forward contracts for Q1-2026 and Q2-2026 can secure sales at predictable prices and help manage inventory exposure, while using short-term storage strategies can smooth supply until demand recovers.

In South America, manufacturers should continue prioritizing WMP production to capture stronger export demand in Argentina and Uruguay, while carefully monitoring Brazilian market needs to avoid oversupply and maintain premium pricing.

For US producers facing weak exports and subdued milk powder production, hedging strategies using futures or options contracts should be considered to protect against price volatility, particularly for NDM and SMP. Production schedules should be aligned with domestic and export demand cycles, ensuring that block and bulk SMP/WMP availability matches peak retail and food-service needs.