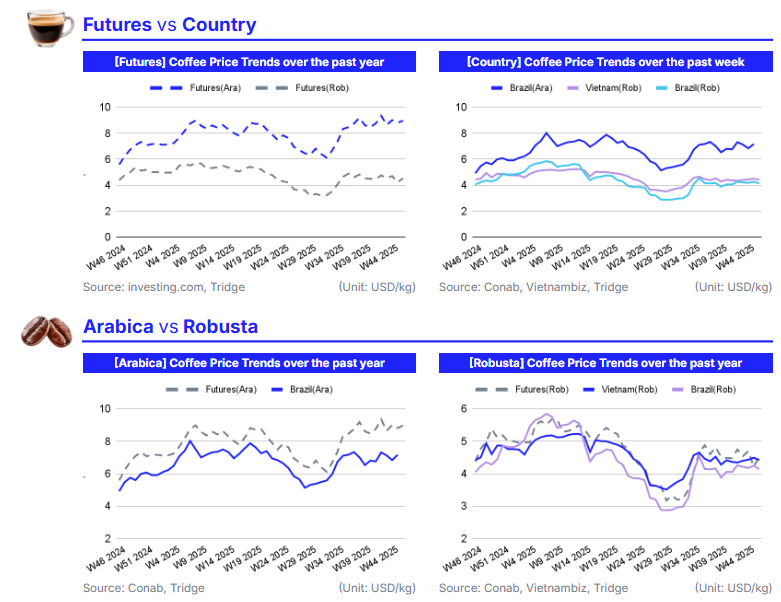

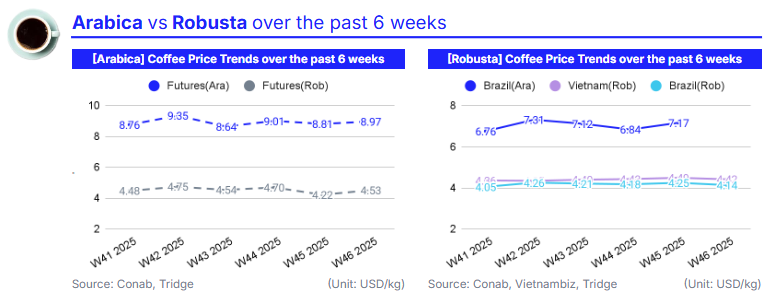

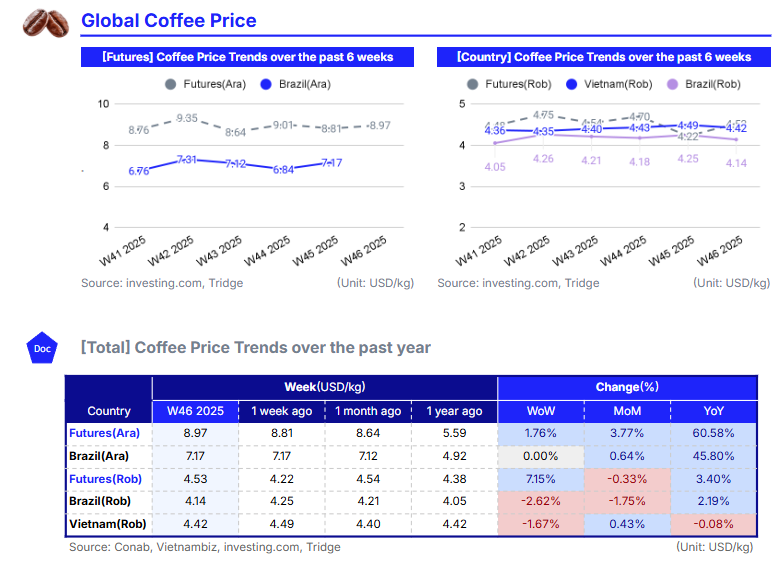

In W46 2025, global coffee prices continued to rise as tightening inventories and persistent logistics constraints supported benchmark futures. Arabica (US Coffee C Futures) increased to 8.97 USD/kg (+1.76% WoW), while Robusta (London Coffee Futures) climbed to 4.53 USD/kg (+7.15% WoW). The gains reflect falling ICE-certified Arabica stocks, ongoing congestion in Brazil, where Sep-25 port delays left nearly 1 million bags unshipped, and renewed uncertainty over US tariff policy, which continues to keep US roaster costs elevated. In origin markets, Brazil’s Arabica held steady at 7.17 USD/kg, while Robusta fell to 4.14 USD/kg (-2.62% WoW) amid a weaker dollar and thin trading. Vietnam’s Robusta softened slightly to 4.42 USD/kg (-1.67% WoW) as strong exports and expectations of a 10% production increase for 2025/26 put mild pressure on prices. For a global food manufacturer sourcing Brazilian Robusta, the core strategy is to secure Vietnamese volumes early, given strong exports, softer prices, and a larger 2025/26 crop, while maintaining flexibility to shift toward Brazilian supply once Santos congestion eases. Brazil’s logistical delays continue to add upside risk to Robusta premiums, making Vietnam the more reliable near-term anchor. To manage price volatility, a light long hedge using call-skewed Robusta structures provides protection against weather-driven firmness without heavy premium costs, ensuring stable supply and preserving optionality as Brazil’s logistics and Vietnam’s harvest progress into early 2026.

1. Weekly Price Overview

Arabica and Robusta Rebound as Brazil Faces Logistics Delays and Vietnam Expands Exports

In W46 2025, global coffee prices continued their upward momentum, with the international Arabica benchmark, represented by US Coffee C Futures, rising 1.76% week-on-week (WoW) to USD 8.97 per kilogram (kg), and the international Robusta price, represented by London Coffee Futures, gaining 7.15% WoW to USD 4.53/kg. The rebound reflects tightening inventories, persistent logistics bottlenecks in Brazil, and renewed uncertainty surrounding the United States (US) tariff policy. Despite public comments from the US President indicating potential tariff reductions on imported coffee, no formal changes have been enacted, and US roasters continue to face elevated import costs. Retail-roasted coffee prices in the US rose to USD 9.14 per pound (lb) in Sep-25, up 41% year-on-year (YoY), according to Bureau of Labour Statistics data.

In Brazil, Arabica remained stable at USD 7.17/kg, while Robusta declined 2.62% WoW from USD 4.25/kg to USD 4.14/kg amid a weaker dollar, thin trading volumes, and producer hesitation amid shifting international benchmarks. Domestic logistics constraints continue to restrict export flows. Port delays in Santos reached 75% of vessels in Sep-25, with unshipped volumes exceeding 939,000 bags, according to the Brazilian Coffee Exporters Council (Cecafé). The disruptions prevented an estimated USD 348 million in exports and continue to support international prices by slowing the release of Brazilian supply into the global market. Brazil exported 1.26 million bags during the first five working days of November, reflecting solid demand but ongoing logistical strain.

Vietnam’s Robusta market softened slightly, down 1.67% WoW to USD 4.42/kg, as record export momentum and expectations of a 10% production increase for the 2025/26 crop exerted downward pressure. Exports for the first ten months reached 1.31 million metric tons (mmt), up 13.4% YoY, reinforcing Vietnam’s role as the primary anchor supplier to the global Robusta market.

2. Price Analysis

Arabica Extends Bullish Run as ICE Stocks Hit 18-Month Low and Vietnam’s Weather Disruptions Add Support to Robusta Coffee

Global coffee prices strengthened as of W46 2025, Arabica rose 3.77% MoM and 60.58% YoY to USD 8.97/kg, while Robusta increased 3.40% YoY to USD 4.53/kg. The primary driver of Arabica’s surge is the sharp decline in ICE-certified stocks, which have fallen more than 40% since late Jul-25 and sit at their lowest level in 18 months. This contraction reflects both growers’ reluctance to certify beans, given stronger domestic pricing and capitalized farm balance sheets, and the accelerated drawdown by roasters, especially in the US, where tariffs have raised import costs and encouraged stock consumption. Supply-side uncertainty remains elevated. Brazil’s 2026/27 Arabica development improved following late-Oct-25 rains, but the earlier drought and premature flowering leave yield risk unresolved. Robusta markets are supported by weather disruptions in Vietnam, where heavy rains linked to Typhoon Kalmaegi have delayed harvests and increased quality concerns, while Brazil’s Conilon faces a likely cyclical production dip after its record 25/26 output.

Given tightening certified stocks, weather-sensitive supply outlooks, and mounting logistical pressure, highlighted by Brazil’s Sep-25 export bottlenecks that left nearly 1 million bags stranded, Arabica is likely to remain bullish in the short term. Prices should stay elevated until ICE stocks rebuild materially, which is unlikely before early 2026. Robusta trends more neutral-to-bullish. While Vietnamese domestic prices remain stable MoM, harvest delays and ongoing rainfall issues suggest firmness ahead, especially if demand shifts from expensive Arabica into lower-grade blends. In the broader market, rising logistics costs, port congestion in Brazil, and delayed export flows add upside risk across both varieties, reinforcing a supportive price environment into Q1-2026.

3. Strategic Recommendations

Arabica Rally Extends on Tight Stocks as Vietnamese Weather Risks Support Robusta Trade Strategies into Early 2026

Given the continued rise in global coffee prices and the stronger momentum in Arabica versus Robusta, market participants should adopt differentiated origin and instrument strategies. Arabica remains structurally bullish due to a sharp contraction in ICE-certified stocks, persistent logistics congestion in Brazil, and unresolved weather risks that keep the 2026/27 crop outlook fragile. These conditions reinforce a supportive price environment into early 2026, creating opportunities for traders to lean long on Arabica through controlled exposure. Robusta offers a neutral-to-bullish setup: Vietnam’s record export pace and expectations of a sizeable production increase apply downward pressure, but ongoing weather disruptions, delayed harvests linked to Kalmaegi, and Brazil’s likely Conilon production dip prevent sustained price softness. Logistics constraints in Brazil continue to slow the release of supply, providing an additional cushion for both markets.

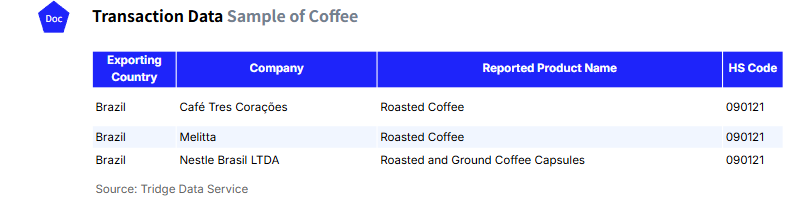

Based on this price environment, Arabica traders should consider accumulating long exposure through a combination of futures and call spreads targeting Q1–Q2 2026, taking advantage of the current divergence between certified stock drawdowns and physical export delays. These structures limit premium outlay while capturing the upside associated with tight inventories and delayed Brazilian flows. For Robusta, a more balanced stance is appropriate. Traders can maintain a mild long bias using call-skewed structures that benefit from weather-driven firmness while acknowledging the coming wave of Vietnamese supply. Importers and roasters that rely heavily on Robusta blends should prioritise Vietnamese volumes in the near term while maintaining flexibility to reweight toward Brazil once logistics normalise. According to data from Tridge Eye, diversifying supply through Brazilian roasted and capsule products from Café Três Corações, Melitta, and Nestlé Brasil LTDA can help mitigate domestic basis volatility and protect downstream margins.

In the next 30 to 60 days, buyers should deepen engagement with Vietnamese exporters as the 2025/26 harvest progresses, securing early-cycle shipments before export competition intensifies. US and European Union (EU) roasters facing elevated logistics costs should advance freight bookings to avoid Santos-related congestion risk extending into early 2026. For Arabica, a gradual buildup of long positions is warranted while ICE stocks remain at multi-year lows, with periodic reassessment as Brazilian weather updates become available in early 2026. For Robusta, maintaining optionality is essential: securing physical volumes from Vietnam while holding upside calls allows roasters to manage potential price firmness stemming from slow harvest progress and weather uncertainty. As both markets remain highly sensitive to logistics and weather outcomes, a rolling review of hedge ratios is necessary, ensuring exposure levels adapt to shifts in Brazilian export flows and Vietnam’s harvest performance.