.jpg)

In W17 in the wheat landscape, some of the most relevant trends included:

- The USDA forecasts a 9% YoY decrease in global wheat trade for the 2024/25 season. This is primarily due to reduced imports from major wheat buyers like China and Pakistan, which are increasing domestic production.

- Russian wheat exports significantly dropped in Apr-25, with only 1.3 mmt shipped during the first 20 days. Key export markets like Egypt and Saudi Arabia reduced their purchases, prompting alternative suppliers like Romania and Ukraine to take over tenders.

- Ukraine’s wheat harvest for the 2025/26 season will be 23% lower than the previous year, due to dry soils and reduced crop areas. Despite this, exports will exceed half of last year’s record volume.

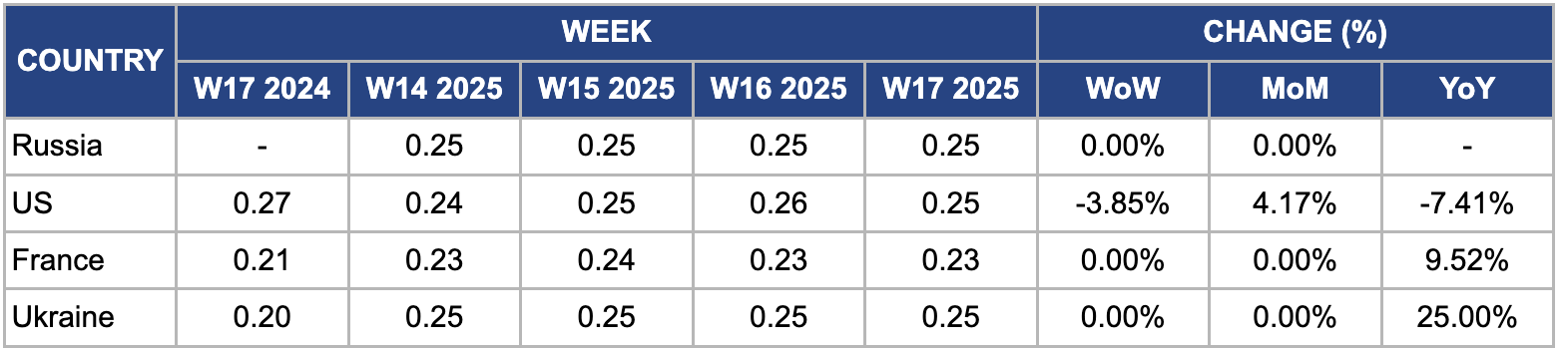

- US FOB wheat prices declined WoW due to challenging weather conditions. Meanwhile, Russian wheat prices remained stable for the fourth consecutive week due to government interventions, including a price floor and increased export duties designed to stabilize the market. In contrast, Ukrainian wheat prices surged YoY, reflecting market adjustments to lower production expectations.

1. Weekly News

Global

USDA Predicts 9% Drop in Global Wheat Trade Due to Falling Imports from China and Pakistan

The United States Department of Agriculture (USDA) forecasts a significant decline in world wheat trade, predicting a 9% year-on-year (YoY) drop in the 2024/25 season compared to the previous one. This marks the sharpest one-year decline in decades. The main factor driving this decrease is the reduced import demand from major wheat-importing countries, such as China and Pakistan.

As these countries increase their domestic wheat production, they rely less on imports. China's wheat imports are plummeting. The USDA revised its forecast for Chinese wheat imports in Mar-25 to 6.5 million metric tons (mmt), and in its Apr-25 forecast, it dropped further to 3.5 mmt. This represents a 10.1 mmt decrease from the 2023/24 season, when China imported 13.6 mmt. Countries that export wheat to China, particularly Australia, which depends heavily on China as an export destination, are impacted.

Indonesia

Indonesia and Jordan Begin Agricultural Cooperation on Wheat Production

Indonesia announced plans to collaborate with Jordan on wheat planting trials to reduce its reliance on wheat imports. During their visit to Jordan in W16, the Indonesian Agriculture Minister and the President signed a bilateral agricultural cooperation agreement with the Jordanian Agriculture Minister, initiating the partnership. The agreement includes agricultural exchange, plantation technologies, and water management strategies. Jordan's efficient irrigation system and successful wheat production could be key assets to Indonesia. Indonesia has assessed agroclimatic conditions suitable for wheat and is now seeking high-yield seed varieties. Jordan will also send experts to support the trial phase in Indonesia. If successful, this project could be a step toward Indonesia's long-term goal of reducing wheat import volumes.

Russia

Russian Wheat Exports Declined Sharply in Early Apr-25 Due to Reduced Demand

Russian wheat exports dropped sharply in Apr-25, with only 1.3 mmt shipped during the first 20 days, 2.8 times less than in Apr-24. Full-month exports are projected at just 2 mmt, well below the five-year average of 3.5 mmt, marking the fourth consecutive month of below-normal volumes. This decline is due to low export margins, loss of price competitiveness, and reduced interest from key buyers. The number of importing countries also fell drastically from 35 to 15, with Iran, Türkiye, and Libya remaining as top buyers, although their purchase volumes also decreased. Egypt, traditionally a major customer, slashed its imports by 8.2 times, while Israel, Saudi Arabia, and Yemen also significantly reduced purchases.

Conversely, Lebanon, Tanzania, and Oman showed moderate growth, albeit with small volumes. Amid reduced Russian shipments, more countries are turning to alternative suppliers. For instance, Algeria recently secured 570 thousand metric tons (mt) to 600 thousand mt of wheat of any origin at USD 267.5/mt. This is USD 2 to 3 cheaper than Russian offers, suggesting countries like Romania, Bulgaria, and Ukraine likely won the tender due to more favorable pricing.

Ukraine

Ukraine's Wheat Harvest to Drop 23% YoY in 2025/26, Reaching 13-Year Low

According to the USDA, Ukraine’s wheat harvest for the 2025/26 marketing year (MY) will reach 17.9 mmt, the lowest in 13 years and 23% lower than in 2024/25. This decline is attributed to dry soils during the sowing season and reduced crop areas due to low profitability. In contrast, Russia forecasts its wheat harvest to range from 79.7 mmt to 82.5 mmt for the same period, nearly matching the production levels of 2024/25. While favorable weather conditions could improve crop conditions in both countries, the initial forecasts raise concerns, particularly as the USDA expects Ukrainian wheat exports to exceed half of the record volume from the previous year.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W17 2024 to W17 2025)

Russia

In W17, Russian FOB wheat prices remained stable at USD 0.25 per kilogram (kg) for the fourth consecutive week. This stability is mainly due to government measures, including a price floor set by the Russian Ministry of Agriculture at USD 250/mt for wheat exports to curb excessive export volumes and manage domestic inflation. Furthermore, the Russian government raised export duties by 12.2% in Mar-25, which has helped control the flow of wheat out of the country, ensuring price stability. Russian wheat production for the 2024/25 harvest season will be strong, supported by favorable weather conditions and improved yields in key growing regions such as Krasnodar and Rostov. Despite global price fluctuations, Russian wheat prices have remained resilient, supported by consistent domestic production, strategic export quotas, and ongoing government measures that helped stabilize the wheat export market.

United States

In W17, United States (US) FOB wheat prices declined 3.85% week-on-week (WoW), reaching USD 0.25/kg. Weekend rains on April 19 to 20 offered some relief to dry hard red winter wheat fields in Kansas and Oklahoma, but the latest crop conditions report indicated no immediate improvement. Winter wheat conditions declined in central and southern production areas, except Texas, while conditions improved in South Dakota and Montana. As of April 20, the USDA reported mixed wheat conditions, with Kansas at 41% good-to-excellent (down from 43%), Oklahoma at 39% (down from 43%), and Texas at 27% (up from 23%). Despite Nov-24 rain providing benefits to the crop, many areas, especially southwest Kansas and northern Oklahoma, still lack substantial rain.

France

In W17, wholesale wheat prices in France remained steady at USD 0.23/kg, with no change WoW or month-on-month (MoM). However, prices saw a 9.52% YoY increase due to tightening supply expectations and weather-related risks to the 2025 wheat crop. Persistent wet conditions in key wheat-growing regions like Hauts-de-France and Grand Est have delayed spring fieldwork, with only 80% of the planned soft wheat area planted by early Apr-25, compared to 95% last year. Concerns over fungal diseases caused by excess moisture have raised doubts about the potential yield and quality of the crop. Despite these challenges, steady demand from North African countries, such as Algeria and Morocco, has helped sustain export activity.

Ukraine

Ukrainian wheat prices remained unchanged WoW and MoM in W17. However, prices surged by 25% YoY, rising to USD 0.25/kg from USD 0.20/kg in W17 2024 due to tight supply. According to the USDA, the wheat harvest for MY 2025/26 will be 17.9 mmt, the lowest in 13 years and 23% lower than the previous year's harvest. This decline is due to dry soils during the sowing season and reduced crop areas due to low profitability.

3. Actionable Recommendations

Diversify Export Markets for Wheat Producers

As the USDA forecasts a decline in global wheat trade, especially with major importers like China and Pakistan reducing their reliance on imports, wheat-producing countries should actively seek to diversify their export markets. For instance, countries like Australia and Russia, which have historically relied on China, could look to expand their wheat exports to regions like Southeast Asia, Africa, and Latin America, where growing populations and rising demand for wheat products present new opportunities. Developing relationships with emerging wheat-importing countries and tapping into non-traditional markets can help reduce dependency on a few large buyers and mitigate the risk of sharp price fluctuations caused by shifting demand from major importers.

Invest in Domestic Wheat Production Efficiency

Indonesia should invest in domestic wheat production to reduce its reliance on imports. As Indonesia collaborates with Jordan to improve wheat yields through advanced irrigation systems and high-yield seed varieties, other wheat-importing countries should prioritize boosting local agricultural productivity. Governments and private stakeholders should allocate resources to agricultural research and development, focusing on climate-resilient seed varieties, water-saving technologies, and precision farming practices. This approach would reduce dependence on volatile international wheat markets, stabilize local prices, and enhance food security.

Monitor Global Supply Chains and Price Fluctuations

In light of the ongoing volatility in global wheat prices, Russian and Ukrainian exporters and importers must closely monitor price trends and disruptions in global supply chains. Importers should build strategic wheat reserves during periods of price stability or low supply, particularly when geopolitical risks or weather events threaten production. Exporters should explore fixed-price contracts or long-term agreements with buyers to mitigate the impact of short-term price fluctuations. Both producers and buyers must leverage hedging strategies and forward contracts to manage risks from market uncertainties and ensure supply chain stability.

Sources: Tridge, Oilworld, UkrAgroConsult