In W30 in the milk landscape, some of the most relevant trends included:

- The global dairy market is splitting into two distinct paths, with developing nations in Southeast Asia and Africa set for robust production growth. This contrasts sharply with the EU, which faces a decade of stagnation and potential decline due to environmental regulations and shrinking herd sizes.

- Animal diseases are causing significant supply disruptions, with LSD in France and Bluetongue across Western Europe directly impacting production and trade.

- Evolving trade relationships, such as the new UK-EU accord and New Zealand's market access win in Canada, are creating new opportunities and challenges for exporters.

- Animal welfare standards are becoming important among German consumers, with supermarkets like Lidl implementing higher husbandry standards for their products.

1. Weekly News

Global

Global Dairy Supply to Grow, But Europe Faces Stagnation

Global dairy production is projected to be the fastest-growing livestock sector over the next decade, with milk output forecast to increase by 1.8% annually to 1,146 million metric tons (mmt) by 2034. This growth will be driven primarily by significant expansion in developing countries like India and Pakistan in Southeast Asia and Africa, where yields and herd sizes are increasing. This robust global growth stands in stark contrast to the outlook for the European Union (EU), where production is forecast to stagnate and even slightly decline. The EU's output is constrained by a combination of tightening environmental policies, the lasting impact of disease outbreaks, and a structural decline in dairy herd numbers, particularly in Western Europe. This divergence is expected to reshape global dairy trade, with developing nations playing a larger role in volume growth while the EU increasingly focuses on value-added products like cheese.

Europe

EU Milk Production Set for Decline in 2025 Amid Mounting Pressures

EU milk production is forecast to decline by 0.2% in 2025, with total deliveries expected to reach 149.4 mmt, according to a new United States Department of Agriculture (USDA) report. This slight but significant drop is driven by a combination of persistent low farmer margins, tightening environmental restrictions, and the ongoing impact of disease outbreaks across major producing nations. These pressures are accelerating the trend of smaller farmers exiting the industry, leading to a reduction in the total number of dairy cows that cannot be fully offset by productivity gains. The anticipated supply constraint is expected to have a ripple effect through the supply chain, with domestic fluid milk consumption also projected to fall by 0.3% to 23.5 mmt. This will force dairy processors to make strategic decisions on how to best allocate the reduced volume of raw milk for their various products.

Belgium

Belgian Dairy Sector Faces Consolidation as 20% of Farms Plan Exit

A new survey by the Flanders Research Institute for Agriculture, Fisheries and Food (ILVO), Belgium, reveals a significant structural shift is underway in the nation's dairy sector, with 20% of dairy farms indicating they intend to cease operations by 2030. This trend is primarily driven by smaller farms exiting the industry, a reflection of natural attrition and economic pressures. However, this exodus is not expected to cause a major drop in overall milk production. The report notes that a quarter of the remaining, larger dairy farms plan to increase their herd sizes. This consolidation is projected to result in only a 6% net decrease in the total dairy herd. The findings point towards a future Belgian dairy landscape characterized by fewer, but larger and more intensive, farming operations.

France

France Battles Lumpy Skin Disease Outbreak with Culling and Vaccination

France is currently battling a rapidly spreading outbreak of lumpy skin disease (LSD), with 32 infections confirmed since the first case appeared in Jun-25. The French Ministry of Agriculture has declared an emergency, implementing drastic measures to contain the virus, including the mandatory culling of infected herds and a wide-scale vaccination program in the affected Savoie border region. To mitigate the economic blow, the government is providing comprehensive financial support, covering the costs of vaccines, veterinary services, and compensation for culled animals. However, these harsh interventions are meeting resistance from some farmers. While major farming unions support the measures, they are demanding fair market-value compensation, and smaller associations are questioning the necessity of such a severe approach, creating a tense situation for the French livestock sector.

Germany

Lidl Germany Expands High-Welfare Standards to More Dairy Products

Supermarket chain, Lidl, is significantly expanding its commitment to animal welfare in Germany, pledging to convert a wide range of its dairy products to at least Level 3 husbandry standards by the end of 2025. The initiative, which includes items like quark, fresh whipped cream, sour cream, grainy cream cheese, and Skyr Pur, will exclusively use raw milk sourced from German farms, reinforcing the discounter's partnership with domestic agriculture. This move builds on the company's previous conversion to higher welfare standards for all its drinking milk in 2024. By making this switch, Lidl is directly responding to growing consumer demand, where animal welfare has become a key purchasing factor. The company is supporting this transition by paying an animal welfare premium to its farmers, highlighting a strategic shift to align its product range with evolving consumer values.

New Zealand

New Zealand Secures Canadian Dairy Market Access in Trade Dispute Win

New Zealand's dairy sector has secured a significant victory in a long-running trade dispute, with Canada agreeing to open its market to New Zealand dairy products. The resolution comes after Canada restricted imports in a manner that violated the terms of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). As a result of the agreement, Canada will adjust its dairy quotas, a move that is expected to generate an additional USD 157 million in revenue for New Zealand's dairy exporters. This breakthrough provides a substantial boost to the country's export-focused industry, creating valuable new access to the protected Canadian market and reinforcing the importance of international trade agreements for New Zealand's economic prosperity.

Poland

Poland's Dairy Sector Captures South Korean Market with Quality and Value

Poland's dairy industry is rapidly expanding its presence in the South Korean market, with the value of its milk and cream exports nearly doubling from USD 16.82 million in 2022 to USD 33 million in 2024. During the same period, the export volume of these products increased by 84%, from 23,834 metric tons (mt) in 2022 to 43,789 mt in 2024. By May of this year, the export volume also reached 12,788 mt, with an export value of USD 9.58 million. This success is underscored by the fact that Polish products accounted for approximately 90% of all sterilized milk imported by South Korea last year. The sector's competitive edge is attributed to a combination of high quality and affordable pricing, with its sterilized milk being cheaper than German and French alternatives. Polish producers credit their less industrialized, natural grazing-based farming model for producing milk with superior taste and nutritional value. This commitment to quality, backed by strict EU safety standards and farmer education programs, is central to their long-term strategy of building consumer trust and integrating their products into the Korean market.

2. Weekly Pricing

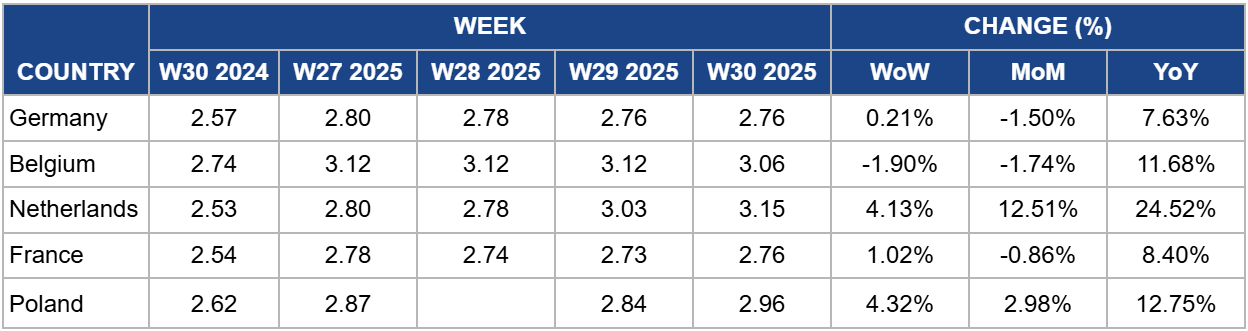

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

Yearly Change in Powdered Milk Pricing Important Exporters (W30 2024 to W30 2025)

Germany

In Germany, the price of SMP was USD 2.76/kg in W30, a slight increase of 0.21% week-on-week (WoW). This price represents a 1.5% decrease month-on-month (MoM) but remains up a significant 7.63% year-on-year (YoY). The German SMP market appears to be stabilizing after recent volatility, with prices firming up slightly this week. The minor WoW increase suggests that the market has absorbed the peak of the seasonal milk flush and is now reacting to the underlying tightness in the EU's raw milk supply.

The slight MoM decrease, however, indicates that prices are still correcting from the higher levels seen before the full impact of the spring production peak was felt. The most significant trend remains the 7.63% YoY price increase. This is a direct consequence of the structural supply constraints facing the EU dairy sector, including reduced cattle herds from disease and drought. These factors have fundamentally tightened the raw milk market compared to last year, keeping the cost of producing storable commodities like SMP at a significantly elevated level.

Belgium

In Belgium, the price of SMP was USD 3.06/kg in W30, a decrease of 1.9% WoW and 1.74% MoM, but still up a significant 11.68% YoY. The Belgian SMP market is experiencing a short-term correction, though prices remain significantly elevated compared to last year. The recent weekly and monthly price declines suggest that the market is currently well-supplied with raw milk following the seasonal production peak. This has eased the immediate upward pressure that was seen in previous weeks, allowing prices to soften from their recent highs.

However, the dominant long-term trend is the 11.68% YoY price increase. This reflects the fundamental supply tightness across the EU, where reduced cattle herds from disease and drought have constrained overall milk production. While the seasonal flush has provided temporary relief, the underlying scarcity of raw milk compared to the previous year continues to support a significantly higher price floor for storable commodities like SMP.

Netherlands

In the Netherlands, the price of SMP was USD 3.15/kg in W30, a sharp increase of 4.13% WoW. This contributes to a substantial 12.51% MoM rise and a significant 24.52% increase YoY. The Dutch SMP market is experiencing a strong bullish trend, with prices surging across all timeframes. The dramatic weekly and monthly price increases are a direct result of the tightening raw milk supply both domestically and across the EU. As the seasonal production peak has passed, the underlying supply constraints—caused by smaller cattle herds due to disease and environmental pressures—are becoming more acute, driving up input costs for processors.

The significant 24.52% YoY increase underscores the long-term impact of these supply shocks. The Dutch dairy herd was particularly affected by the bluetongue virus outbreak, which has constrained milk yields and overall production throughout the past year. This fundamental scarcity of raw milk compared to the same period in 2024 is the primary driver supporting the significantly elevated price for storable commodities like SMP.

France

In France, the price of SMP was USD 2.76/kg in W30, a slight increase of 1.02% WoW. The price is down 0.86% MoM but remains up a significant 8.40% YoY. The slight WoW increase suggests that the market is moving past the peak of the spring/summer milk flush, and the underlying tightness in the EU's raw milk supply is beginning to reassert upward pressure. The marginal MoM decrease, however, indicates that the market is still balanced by the tail end of this seasonal production.

The most critical trend is the 8.40% YoY price increase. This is a direct consequence of the structural supply constraints facing the EU dairy sector, including reduced cattle herds from disease outbreaks (bluetongue and LSD) and environmental pressures. This fundamental scarcity of raw milk compared to the same period last year is the primary driver supporting the elevated price for storable commodities like SMP.

Poland

In Poland, the price of SMP was USD 2.96/kg in W30, a strong increase of 4.32% WoW. This contributes to a 2.98% MoM rise and a significant 12.75% increase YoY. The Polish SMP market is showing significant strength, with prices rising sharply in the short term. This rally is driven by two key factors: the tightening raw milk supply across the EU as the seasonal production peak ends, and robust export demand for Polish dairy products. With Poland successfully capturing significant market share in destinations like South Korea, the strong demand for finished goods is supporting higher prices for commodities like SMP.

The substantial 12.75% YoY price increase highlights the impact of the EU's structural supply constraints. Although Poland's own milk production is growing, bucking the trend seen in Western Europe, it cannot fully offset the continent-wide reduction in cattle herds caused by disease and environmental pressures. This has created a fundamentally tighter European market compared to last year, supporting a significantly higher price floor for storable dairy commodities.

3. Actionable Recommendations

Emulate Poland's Export Success in High-Growth Asian Markets

With EU milk production forecast to stagnate, growth for European processors must come from value-added exports, not increased volume. Companies in Western Europe should adopt the successful strategy demonstrated by Poland in the South Korean market. This involves leveraging the EU's reputation for high quality and safety to introduce premium products, like specialty cheeses and UHT milk, to high-growth Asian markets where dairy consumption is rising. By offering a competitive price point combined with a strong quality narrative, processors can capture new market share and build long-term consumer trust. This strategic pivot allows companies to find profitable new outlets for their products, offsetting the challenges of a constrained domestic raw material supply.

German Producers Must Capitalize on the Animal Welfare Trend

Lidl's major shift to higher animal welfare standards for its dairy products is a clear and powerful market signal driven by consumer demand. German dairy farmers and processors should view this not as a burden, but as a significant commercial opportunity. Farmers should proactively invest in and seek certification for higher husbandry systems (e.g., Level 3) to qualify for the premium payments offered by retailers like Lidl. For processors, this means developing segregated supply chains to market these high-welfare products under premium private labels or their own brands. By embracing this trend, the German dairy sector can secure preferential access to major retail partners and differentiate its products in a competitive market.

Proactively Leverage Trade Agreements to Secure New Markets

New Zealand's recent success in securing an additional USD 157 million in Canadian market access is a powerful demonstration of the tangible value of trade agreements. For dairy exporters in the EU and UK, who are facing stagnant domestic production and the looming threat of US tariffs, this should serve as a critical call to action. Instead of passively waiting for market conditions to improve, industry bodies and individual exporters must proactively lobby their governments to prioritize dairy in all ongoing and future trade negotiations. This includes pushing for the swift implementation of the new UK-EU food safety accord to restore frictionless trade. By actively working to open new markets and enforce existing agreements, exporters can create new revenue streams, diversify their risk away from volatile partners, and secure a more stable and prosperous future in a competitive global landscape.

Sources: Tridge, The Dairy Site, Euromeat News, Dairy Global, ESM, UkrAgroConsult, Chosun Biz