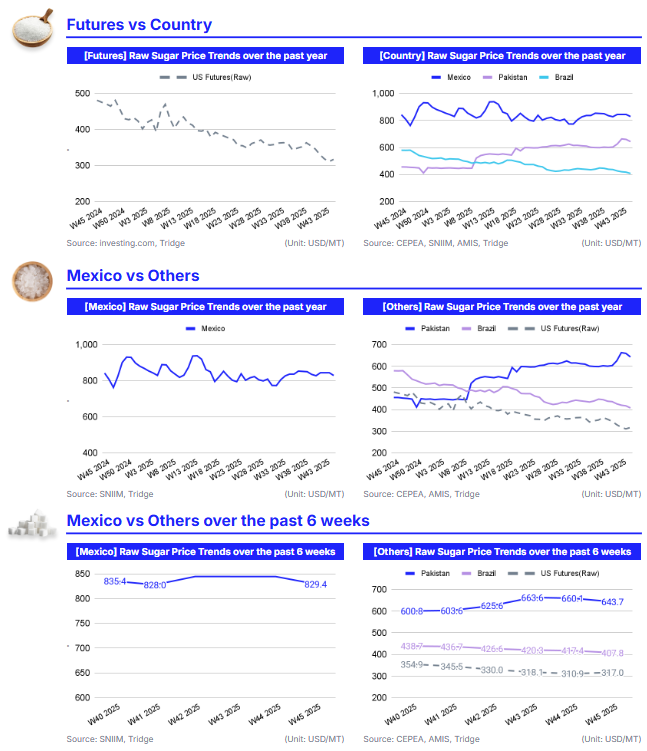

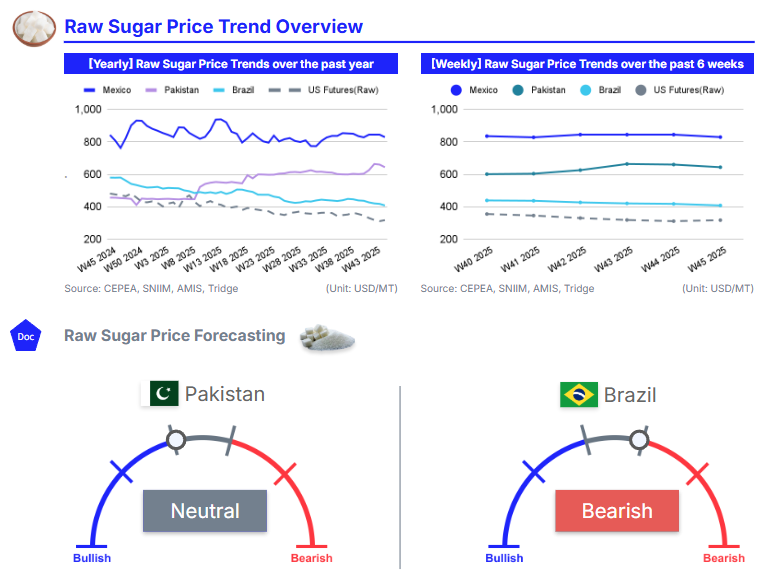

In W45 2025, global sugar prices continued to decline, led by Brazil, where expanding output, weak exports, and rising inventories pushed values toward multi-year lows despite weather-related yield losses. With Brazil’s 2025/26 production projected at 45 mmt and TRS levels deteriorating, the market remains firmly oversupplied, reinforcing a bearish-to-neutral short-term outlook. Mexico’s tariff-protected market remains stable, while Pakistan’s price firming reflects local regulatory shifts rather than global fundamentals.

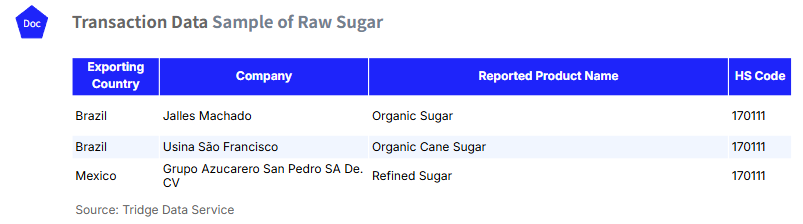

Global food and beverage manufacturers sourcing bulk raw and organic sugar should capitalize on Brazil’s discounted pricing by securing medium-term supply from producers such as Jalles Machado and Usina São Francisco. The core strategy is to prioritize Brazilian volumes through a mix of spot buying and staggered forward contracts through Q2-2026, ensuring cost efficiency while maintaining optionality should export flows tighten later in the season. Mexico’s refined sugar, led by Grupo Azucarero San Pedro, offers supplemental stability for buyers needing consistent specifications without immediate price upside. Traders and risk managers should maintain a bearish-to-neutral positioning, using short futures or bear put spreads while gradually adding upside protection as Brazil’s logistics improve and global demand normalizes.

1. Weekly Price Overview

Brazil’s Rising Output Drives Global Sugar Prices to Multi-Year Lows While Mexico Stabilizes and Pakistan Firms

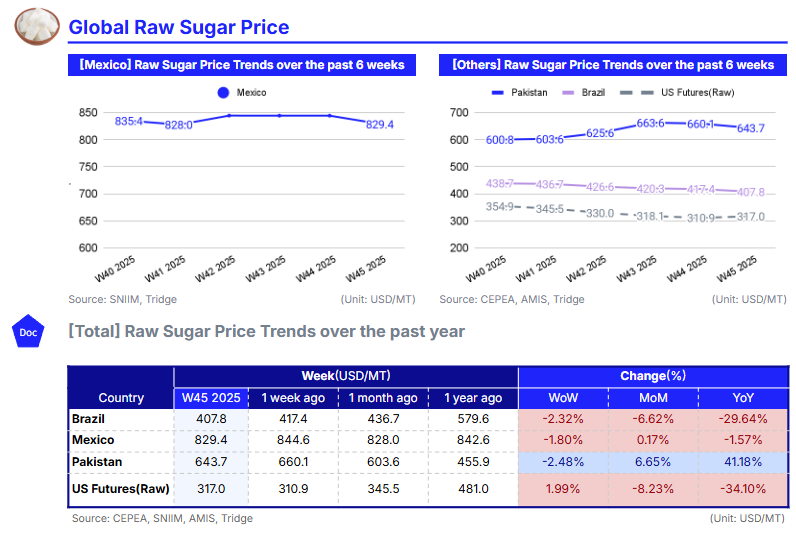

In W45 2025, sugar prices continued to weaken across major markets, led by Brazil, where values fell 2.32% WoW to USD 407.8/mt, extending a broader annual decline of nearly 30%. The recent downturn is primarily driven by Brazil’s National Supply Company (CONAB) updated projections, which show the country's 2025/26 sugar production rising to 45 million metric tons (mmt), a 2% increase and the second-largest output on record. Despite earlier weather challenges in the Center-South, strong sugarcane availability has supported high crushing volumes, reinforcing global oversupply and pushing international prices toward multi-year lows. Lower Brazilian exports between Apr-25 and Sep-25, down 9% YoY to 17.7 mmt, combined with reduced total recoverable sugars (TRS) levels, have further pressured futures markets.

Mexico also experienced price declines, with sugar down 1.80% WoW to USD 829.4/mt, as domestic oversupply continues to weigh on the sector. In response, the government implemented a 156% tariff on sugar imports to stabilize the market and protect growers, alongside a modernization plan aimed at boosting productivity and diversifying sugarcane use into renewable energy. Pakistan moved in the opposite direction, with sugar prices rising 2.48% WoW to USD 643.7/mt amid regulatory measures mandating a uniform crushing start date to secure farmer payments and improve mill-grower coordination. Meanwhile, US raw sugar futures fell 1.99% WoW to USD 317/mt, reflecting global surplus conditions and weak demand, with prices now at the lowest point in five years.

2. Price Analysis

Brazilian Sugar Prices Fall Further as Oversupply and Weak Exports Override Weather-Driven Yield Losses

Brazil’s sugar market extended its downward trajectory in W45, with prices falling 6.62% MoM to USD 436.7/mt and nearly 30% lower YoY. The decline is driven by a combination of weaker raw material quality, slower export flows, and rising inventory burdens, which together outweighed weather-related productivity losses that might have otherwise provided upward price support. Despite drought, excessive heat, and reduced TRS eroding yields across key producing states, particularly São Paulo, the market remains oversupplied because stocks accumulated earlier in the season expanded the stock-to-export ratio. This imbalance has amplified downward pressure on futures markets, reinforcing a bearish short-term trend even as field conditions deteriorate.

Brazil’s harvest outlook presents a mixed structure but still leans toward sustained price softness. Conab’s projection of 666.4 mmt of sugarcane, a 1.6% YoY decline, signals tighter crop performance, yet the 2% increase in sugar output to 45 mmt keeps supply historically high. The combination of low TRS, a smaller cane supply, and a more sugar-heavy production mix suggests that while production efficiency will remain constrained, total availability will remain sufficient to prevent significant price recovery. Export volumes, down 9% between Apr-25 and Sep-25, indicate that logistical and quality issues are limiting the sector’s ability to clear supply quickly, which should continue to weigh on New York futures until stocks normalize. Ethanol dynamics offer only partial support, with strong domestic anhydrous sales helping absorb some cane, but declining overall ethanol output keeps more of the remaining cane directed toward sugar, maintaining global surplus conditions.

In Mexico, prices recorded a mild 0.17% MoM decline, reflecting ongoing oversupply despite new protectionist measures. The newly imposed 156% tariff effectively shuts the door to sugar imports, stabilizing domestic pricing but not creating immediate upward momentum. The broader policy push toward modernization and renewable-energy integration may tighten the market in future seasons, yet the current cycle remains defined by comfortable domestic availability and weak pricing power.

The short-term forecast for sugar prices remains bearish to neutral, dominated by Brazil’s heavy supply base, slowed export pace, and stock overhang. Any price stabilization in Q4-2025 would likely stem from seasonal tightening and marginally improved domestic demand, but a material rebound will require either a sharper weather-driven production cut or a significant acceleration in export flows.

3. Strategic Recommendations

Leverage Brazil’s Low-Price Window While Positioning for Gradual Tightening in 2026

Given the current oversupply and multi-year low prices driven by Brazil’s rising output and slow export pace, global buyers should prioritize securing Brazilian sugar, both conventional and organic, while maintaining flexibility for a potential shift in fundamentals later in the season. Brazil’s projected 45 mmt output, weaker TRS, and rising inventories indicate that discounted values will persist in the short term, offering a cost-effective entry point for food manufacturers and importers. According to Tridge Eye data, Companies such as Jalles Machado and Usina São Francisco can provide competitively priced organic sugar during this window, before export demand strengthens and premiums begin to widen.

Mexico’s market, protected by a 156% import tariff, remains stable but lacks meaningful upward momentum, making it a secondary sourcing option best suited for buyers needing a refined product with consistent domestic availability. Grupo Azucarero San Pedro’s refined sugar offers a predictable supply, but price upside appears limited under current oversupply conditions. Pakistan’s firmer trend reflects local regulatory tightening rather than a broader structural shift, positioning it more as a hedging consideration than a core procurement origin.

Importers and processors should secure Brazilian volumes through a mix of spot purchases and forward contracts covering Q4-2025 to Q2-2026, capturing current discounts while smoothing risk. Traders should maintain a bearish-to-neutral bias via short futures or bear put spreads, shifting gradually into call-skewed structures as export flows improve. North American buyers can supplement Brazilian raws with tariff-shielded Mexican refined sugar to balance cost efficiency and specification needs. Risk managers should implement layered hedging tied to Brazil’s crushing progress and export lineups, combining short futures with upside calls to protect against potential early-2026 tightening.