.jpg)

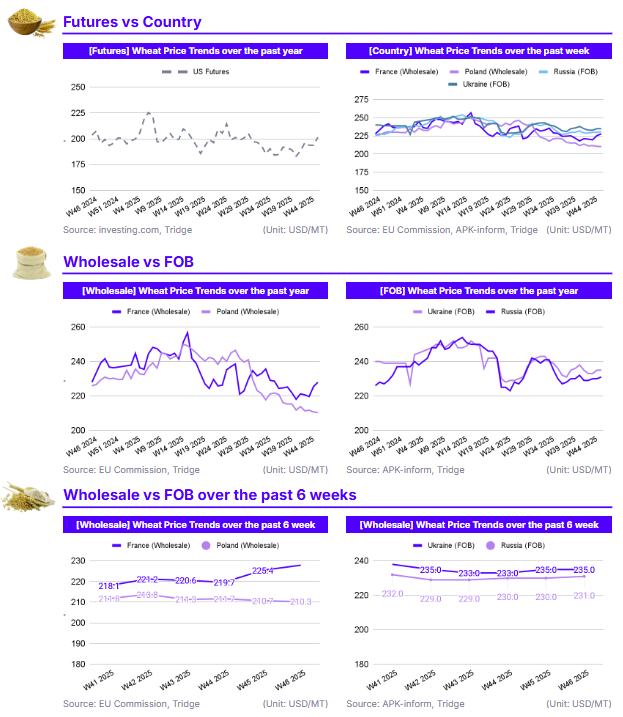

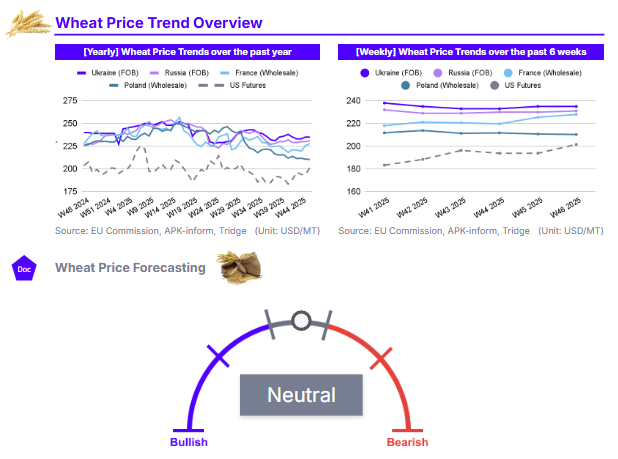

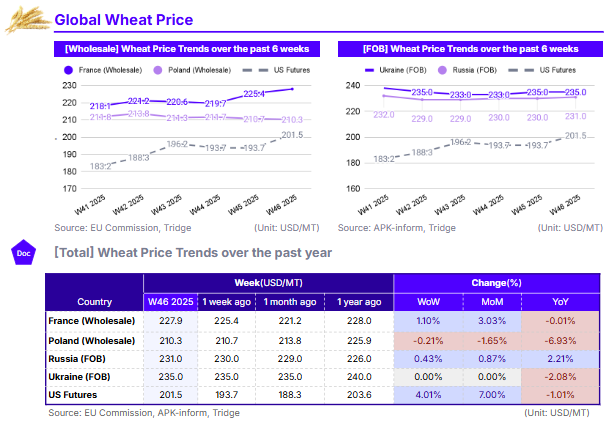

In W46 2025, the US Futures market saw a significant 4.01% WoW surge to USD 201.5/mt, driven by market correction following the release of the Nov-25 WASDE report by the USDA. Black Sea FOB prices also gained slightly WoW. European prices were mixed, with France up 1.10% WoW (USD 227.9/mt) and Poland down 0.21% WoW (USD 210.3/mt). Despite WoW and MoM strength in the US and France, the long-term outlook remains bearish. The Nov-25 WASDE report reinforced this by raising global ending by stocks 7.4 mmt, signaling the first YoY stock build since 2019/20. This global glut has caused widespread YoY price compression, particularly for Poland (-6.93% YoY). Given this trend, EU buyers should prioritize Poland for cost-competitive sourcing, benefiting from a USD 17.6/mt price advantage over France. However, France (USD 227.9/mt) is recommended for large-scale procurement due to superior volume availability and stability.

1. Weekly Price Overview

US Prices Correct Following USDA Report While Other Major Markets Remaining Stable

In W46, US Wheat Futures showed the strongest movement, closing at USD 201.5 per metric ton (mt), a significant 4.01% increase week-on-week (WoW). This surge is likely driven by market corrections following the release of the Nov-25 World Agricultural Supply and Demand Estimates (WASDE) report released by the United States Department of Agriculture (USDA). In the Black Sea, prices showed stability and slight gains. Russia's Free on Board (FOB) price rose 0.43% WoW to USD 231.0/mt, while Ukraine's FOB price was unchanged at USD 235.0/mt. The slight increase in Russian prices can be attributed to a renewed risk premium following Ukrainian drone attacks on key Russian Black Sea ports, which caused temporary disruption and shifted exports to the Baltic sea. The upward pressure is compounded by a downwardly revised production outlook from Russia.

European prices were mixed. France saw its wholesale price rise 1.10% WoW to USD 227.9/mt. This gain is supported by a 2025 harvest relatively on par with the five year average and farmers quickly advancing planting for the next crop, with 89% of soft wheat planted by mid Nov-25, which is ahead of the five-year average. In contrast, Poland’s wholesale price saw the only decline, dropping 0.21% WoW to USD 210.3/mt, due to ample domestic supply (+ 4.84% on the five-year average) and downward pressure from foreign competition.

2. Price Analysis

Higher Global Production and Ending Stocks Result in Long Term Bearish Market Sentiment

The long-term price structure remains fundamentally bearish, driven by high global production and supplies, although recent performance shows regional resilience. In the US, Futures closed at USD 201.5/mt, recording a strong 7% increase month-on-month (MoM), despite a 1.01% decline year-on-year (YoY). France showed a similar MoM recovery, rising 3.03% MoM to USD 227.9/mt, and is trading essentially flat YoY (-0.01%). Poland, however, remains deeply in negative territory, dropping 1.65% MoM to USD 210.3/mt, resulting in a significant 6.93% YoY decline. Black Sea markets are mixed. Ukraine is flat MoM and down 2.08% YoY, while Russia stands as the only market with positive long-term growth, rising 0.87% MoM and 2.21% YoY.

This persistent YoY price compression across most countries is rooted in the overwhelming global production outlook, as reinforced by the November WASDE report. The report revised the 2025/26 global wheat outlook upwards, increasing global supplies by 11.7 million metric tons (mmt) to 1,090.3 mmt. Crucially, the WASDE report lifted global ending stocks by 7.4 mmt to 271.4 mmt, resulting in the first YoY increase in global wheat stocks since 2019/20. This glut of wheat is weighing heavily on prices across various production regions. Russia’s positive YoY performance is supported by high export demand, even as analytical forecasts predict its 2026 crop will decline to 83.8 mmt from 87.8 mmt in 2025, providing some insulation against the broader bearish global trend.

3. Strategic Recommendations

Prioritize Poland For Cost-Effective Sourcing in Europe

For price-sensitive buyers in the European market, Poland is the preferred origin to optimize procurement costs. This recommendation is compelling due to Poland's low price point in an environment where global supply is fundamentally bearish. As of W46, Polish wholesale wheat is priced at USD 210.3/mt. This offers a substantial USD 17.6/mt discount compared to French wholesale prices of USD 227.9/mt. The price advantage is protected by strong supply fundamentals, including Poland’s high production outlook, expected at 13.4 mmt in 2025. Securing volumes from Poland allows buyers to capitalize on the country’s 6.93% YoY price decline and maximize the price spread available among major Western European producers.

Secure Large-Scale Volume and Liquidity via France

Large-scale processors and multinational buyers whose priority is stable, high-volume fulfillment should prioritize sourcing from France, despite the price premium. While French wholesale is currently USD 17.6/mt higher than Polish wheat, this cost reflects a market with significantly greater liquidity and stability. France’s market is defined by its stable 2025 production, with its price now trading at near-parity YoY after rising 3.03% MoM. The combination of its expected 34 mmt production and fast-paced planting for the 2026 season (89% complete) guarantees the volume required for large-scale operations. Buyers prioritizing supply reliability and the ability to execute massive contracts will find the French market better equipped to manage logistics and volume volatility, justifying the price premium.