W30 2025: Sugar Weekly Update

In W30 in the sugar landscape, some of the most relevant trends included:

- Brazilian sugar producers are advised to lock in forward contracts and manage inventories strategically as domestic output pressures spot prices.

- US buyers should secure imports early amid high wholesale prices and anticipate potential TRQ or WTO-driven shifts in trade policy.

- Pakistan faces rising local sugar prices, making fast-tracked imports and stricter inventory monitoring critical to stabilizing the market.

- Refiners in multiple regions are urged to optimize storage, monitor logistics disruptions, and hedge against Q4 volatility.

- Across all markets, active engagement with customs, logistics, and policy developments is essential for maintaining supply chain resilience.

1. Weekly News

Brazil

Crushing Peaks as Sugar Output Expands Sharply

The Brazilian Sugarcane and Bioenergy Industry Association (UNICA) reports that 201 million metric tons (mmt) of cane were crushed in Centre‑South Brazil through mid‑Jun-25. This is a 13% increase year-on-year (YoY), with sugar output rising by 22% over the same period, signaling solid processing momentum. This elevated throughput continues to support near‑record output estimates for the 2025/26 crop year, confirming sustained volume availability in export channels.

Price Pressure Mounts From Domestic Oversupply

Despite ethanol market considerations, Brazilian sugar is increasingly favored in the production mix, adding to supply-side pressure. Global sugar futures responded accordingly; Intercontinental Exchange (ICE) No. 11 futures slipped by 2% as markets priced in abundant sugar and strong competition from India and Thailand. Export parity is weak, even as the United States (US) dollar strength further depresses price potential.

India

1 MMT Export Permit Greenlit to Manage Growing Surplus

The Indian government reaffirmed permission for mills to export up to 1 mmt of sugar this season, leveraging ample stocks to support mill liquidity and contain domestic price declines. This highlights the heavy surplus structure for the 2024/25 marketing year (MY) as domestic dispatch remains sluggish.

Ethanol Blending Policy Adjusted, Supporting Industry Economics

Regional policy shifts in Maharashtra now permit sugar mills to use maize and other grains in ethanol production, facilitating year-round distillation and offsetting sugar margin vulnerabilities. This adaptation is viewed as a positive structural adjustment to diversify revenue streams and ease sugar glut.

Mexico

Production Rebound Aligns with Weather Recovery, But Export Still Constrained

There have been no significant new developments in Mexico this week, but the United States Department of Agriculture (USDA) forecasts highlight a production recovery to 5.05 mmt in 2025/26 driven by improved weather conditions after drought-impacted years. Mills are gradually regaining planting momentum, though yields and diversion metrics remain under close watch.

Higher Output Not Yet Translating to Export Momentum

Despite improved supply, Mexico continues to face structural export limitations, especially under evolving tariff regimes and quality thresholds. Analysts suggest that while domestic price pressure is easing, international buyers still favor Brazilian origins for cost competitiveness.

Pakistan

Government Orders Massive Imports as Retail Prices Rise

The federal cabinet approved 500,000 metric tons (mt) of duty‑free sugar imports, waiving both customs and sales taxes, to address retail price spikes and supply shortages, as local prices approached USD 0.69 per kilogram (PKR 196/kg). Delivery timelines remain uncertain, delaying immediate relief.

IMF Backlash and Cartel Probes Inject Policy Risk into Market

The International Monetary Fund (IMF) has criticized Pakistan’s tax waiver as violating loan conditions, raising concerns of fiscal mismanagement. At the same time, renewed parliamentary inquiry into alleged pricing collusion among sugar mills has increased regulatory risk, clouding future price pathways.

United States

TRQ Constraints Hold Futures Firm Amid Globally Soft Sentiment

US sugar futures (ICE No. 11) remain anchored near US¢ 16.36 per pound (lb), underpinned by tight tariff-rate quota (TRQ) flows; no significant new quota releases have been announced, limiting supply risk. Despite global oversupply exerting bearish pressure worldwide, US prices remain insulated due to controlled import volumes.

Domestic Supply Balance Provides Stability, Sidestepping Volatility

Domestic beet and cane production are stable, with expected balances maintained through quota management and limited new production shocks. Market participants generally view conditions as balanced, with trading volumes subdued and no imminent policy changes in play to meaningfully disrupt supply dynamics.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W30 2024 to W30 2025)

.png)

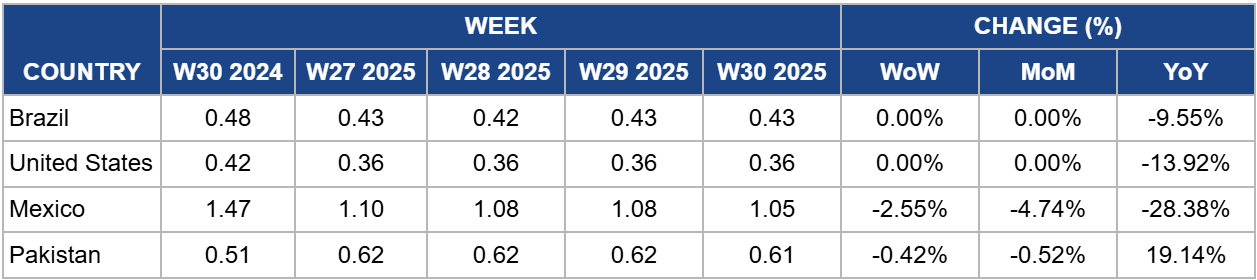

Brazil

In W30, Brazilian wholesale sugar prices remained stable at USD 0.43/kg, similar to W29. YoY prices continue to be subdued, down 8.78% as the market absorbs strong supply from high cane-crushing rates and record sugar output. ICE No.11 futures slipped to US¢ 16.36/lb, down 2.7% on July 21, reflecting oversupply expectations and mounting bearish sentiment.

Wholesale prices in Brazil are likely to stay static or slide slightly unless unexpected export demand emerges or an adverse weather event disrupts harvests. Continued weakness in global futures will keep downward pressure unless supply tightens.

United States

Physical refined wholesale prices remained stable in W30 at USD 0.36/lb, similar to the previous week. YoY prices continue to trend downward by 13.57% owing to steady beet and cane production and quota-based import restrictions. US sugar futures opened around US¢ 16.26-16.36/lb and remained in a narrow trading band, supported by the controlled TRQ system that limits import volumes.

Wholesale refined sugar prices are expected to remain steady owing to stable production. Futures should remain steady around US¢ 16.0-16.5/lb, barring unplanned import announcements or weather disruptions in key regions.

Mexico

In W30, Mexican wholesale sugar prices remained relatively stable at USD 1.05/kg, a slight 2.55% WoW decrease and 4.74% MoM drop, showing stability despite broader global fluctuation. YoY prices continue to exhibit significant downward pressure, down 28.38%. Domestic mills continue recovering output, aligned with improving weather and cane yield, but export activity remains limited and shows no pricing impact yet.

In W31, Mexican sugar prices are expected to remain flat to firm. Unless export tenders or trade shifts emerge, prices are unlikely to show directional change in the near term.

Pakistan

Wholesale sugar prices in Pakistan remained steady at USD 0.61/kg, down 0.42% WoW and 0.52% MoM. Despite this stability, the YoY price remained firm, up 19.14% as supply shortages persist, and government duty-free imports have yet to meaningfully reach the market. As a result, the national average to USD 0.64/kg (PKR 180.9/kg), with some regions reporting spikes as high as USD 0.69-0.71/kg (PKR 195-200/kg) in retail.

With import flows expected to begin clearing customs, wholesale prices may ease modestly in W31. However, unless hoarding and distribution hurdles are resolved, price relief may remain limited and gradual.

3. Actionable Recommendations

Implement Forward Contracting and Inventory Optimization

With international futures prices softening and a strong Brazilian harvest progressing efficiently, millers and exporters should secure forward contracts now to hedge against further downside, especially with bearish signals from the macroeconomic environment. At the same time, exporters should optimize warehouse space and hold back non-committed volumes to exploit better margins if prices rebound in Q4, particularly if India’s output shortfall or global weather events impact the balance. Monitoring ethanol parity and exchange rate fluctuations can further help time export flows for profitability, especially in a volatile forex environment.

Secure Imports and Monitor TRQ Adjustments

The US sugar market continues to operate in a tight supply-demand band, with high wholesale prices sustained by domestic production limits and TRQ caps. Buyers should secure shipments now from Mexico, the Dominican Republic, and other quota-eligible exporters before seasonal shortages intensify. Refiners and major food producers should also stay informed on USDA TRQ announcements and WTO compliance developments, as mid-year policy changes could suddenly shift import dynamics. Additionally, building buffer stocks in Q3 could offer insurance against Hurricane-season supply chain risks, especially in southern US ports.

Accelerate Import Logistics and Expand Monitoring

With domestic sugar prices surging due to tight local inventories and sluggish import clearance, buyers should engage with customs, shipping lines, and transporters to speed up delivery timelines and stabilize downstream prices. Importers and traders should consider joint warehousing and pooled logistics to reduce cost per unit and secure quicker access to high-demand regions such as Punjab and Sindh. Government bodies and industry groups must increase transparency around inventory and mill-level stockholding, helping prevent panic buying or speculative hoarding that could worsen retail inflation.

Sources: Tridge, Barchart, PK Revenue, Pro Pakistani, Pakistan Today, Ground News, Dawn, World Energy News, Agriculture Industry Today, Economic Times, Chini Mandi, USDA