.jpg)

In W30 in the wheat landscape, some of the most relevant trends included:

- The global wheat market is expected to grow steadily in the long term, led by yield gains and moderate expansion in Asia. However, 2025 remains volatile amid weather extremes, geopolitical tensions, and shifting trade dynamics.

- Favorable conditions are boosting wheat yields in the EU, especially in Germany, while France sees a rebound despite export challenges from weak demand and competition.

- Canada faces drought stress and market uncertainty, though durum wheat exports remain robust.

- India’s wheat stocks have hit a four-year high, easing domestic supply concerns, while Indonesia has committed to doubling its annual US wheat imports, indicating rising demand.

- Russia and Ukraine are grappling with weather disruptions, which are reducing yields, harming quality, and driving price volatility.

1. Weekly News

Global

Global Wheat Market to See Decade-Long Growth Despite Current Weather and Geopolitical Volatility

According to the Food and Agriculture Organization (FAO) Agricultural Outlook 2025–2034, global wheat production is forecast to increase by 74 million metric tons (mmt), reaching 874 mmt by 2034. This optimistic forecast is driven largely by yield improvements and moderate area expansion, particularly in Asia. India is expected to contribute nearly 29% of this growth due to government policies aimed at boosting self-sufficiency. Wheat will continue to play a key role in global cereal output, which is projected to reach 3.2 billion metric tons (mt), even as yield growth outpaces expansion in cultivated area. Despite increasing volumes, real wheat prices are expected to decline over the outlook period due to productivity gains, while nominal prices may rise due to inflation. Trade is expected to expand, with wheat exports projected to grow by 21 mmt. The Americas and parts of Europe are expected to reinforce their roles as major exporters, while most African and Asian countries remain net importers.

However, global wheat markets remain volatile in 2025, influenced by weather in key regions, geopolitical tensions, and shifting export strategies. Recent market developments include harvest pressure easing in the Northern Hemisphere, mixed wheat crop forecasts from Russia, Argentina, and Canada, and firm United States (US) export performance, despite soft red spring (SRS) and hard red spring (HRS) wheat prices showing divergent trends. As global wheat consumption is expected to reach 814 mmt by 2025/26 and trade grows, the balance of production, weather conditions, and geopolitics will continue to shape price dynamics and supply chains globally.

European Union

EU Common Wheat Yields Set to Surpass Five-Year Average Due to Favorable Conditions

The European Agricultural Resources Monitoring Agency (MARS) has revised upward its 2025 wheat yield forecasts across the European Union (EU), reflecting favorable growing conditions. The yield for common wheat is now expected to reach 6.09 mt per hectare (ha), slightly above Jun-25 estimates and 6% higher than the five-year average, marking a 9% increase from last season. Durum wheat yield is also raised to 3.78 mt/ha, continuing the positive outlook for wheat production. Complementing this, Germany's National Association of Agricultural Cooperatives projects a 17% year-on-year (YoY) rise in wheat harvest volume, reaching 21.56 mmt, underscoring broader regional optimism. The robust wheat forecasts suggest a strong recovery and production boost for the EU wheat sector in the 2025 season.

Canada

Canadian Wheat Market Faces Drought and Trade Uncertainty Amid Strong Durum Sales

Canada’s wheat production for the 2025/26 season is under pressure due to persistent drought and poor growing conditions across key Prairie provinces, particularly affecting spring and winter wheat. While total wheat output is forecast at 35.15 mmt, production remains uncertain amid moisture stress and tightening ending stocks from 2024/25. Durum wheat exports are notably strong, with 5 mmt shipped from Jan-25 to May-25, reflecting sustained global demand. However, feed wheat markets are weighed down by competition from other grains. Ongoing trade negotiations and potential tariff changes are adding to the volatility and supply risks in Canada’s wheat market.

France

France’s Wheat Recovery in 2025 Faces Export Headwinds Despite Strong Yields

France’s 2025 soft wheat harvest is projected to rise significantly to 33.4 mmt, up 30% from last year’s rain-affected crop, driven by improved yields averaging 7.44 mt/ha. However, a reduced sown area and limited grain filling due to Jun-25 heat are keeping production below the 2017–2023 average. The crop is largely of export quality, yet France faces mounting challenges in finding buyers. Weakened demand from key importers like Algeria and China, along with strong competition from cheaper Black Sea grain and a strengthening euro, are narrowing export opportunities.

Durum wheat production is also recovering, with 2025 output forecast at 1.5 mmt, up from last year’s drought-hit harvest. However, demand for French durum remains weak, particularly in North African markets where local production has improved and imports have shifted to other suppliers.

As a result, France risks stockpiling wheat or diverting it to feed markets, potentially pushing prices below production costs. These export constraints mirror broader struggles in Western Europe, as countries like Germany and Poland face similar market pressures amid a more competitive landscape shaped by Romania, Bulgaria, and Ukraine.

India

India’s Wheat Stocks Reach Four-Year High, Easing Import Concerns

India’s wheat market has stabilized, supported by strong government procurement that lifted wheat stocks to 35.9 mmt as of July 1, the highest in four years and well above official targets. This buffer is expected to help the government manage potential price spikes later in the year through open market sales. Despite concerns about previously poor harvests and speculation around potential wheat imports, the current inventory levels reduce the immediate need for such measures. Additionally, the government has not granted any duty concessions on agricultural commodities, including wheat, under the new free trade agreement with the United Kingdom (UK), ensuring domestic farmers are protected from cheaper imports.

Indonesia

Indonesia to Double US Wheat Imports in Landmark Five-Year Deal

Indonesia’s flour milling association (APTINDO) has signed a memorandum of understanding to double its annual US wheat imports to 1 mmt over the next five years. This reflects Indonesia's rising demand for food-use wheat, which has grown by 22% over the past decade. Kansas hard red winter (HRW) wheat, a key component of past US exports to Indonesia, is expected to meet much of this increased demand, providing a potential boost to Kansas farmgate prices. Already one of the world’s top wheat importers, Indonesia previously imported an average of 500 thousand mt annually from the US, with 2024/25 volumes already nearing 792 thousand mt, underscoring strong market momentum amid global competition.

Russia

Weather Extremes Deepen Strain on Russia’s Wheat Sector in 2025

Russia’s wheat sector is facing intense pressure for the second year in a row as extreme and unpredictable weather, marked by heatwaves in the south and heavy rains in central regions, continues to disrupt production. These adverse conditions have reduced yields and degraded grain quality, with average yields dropping to 3.5 mt/ha by mid-Jul-25, down from 3.7 mt/ha the previous year. Harvesting progress remained slow, particularly in the southern regions, though it accelerated in the second half of the month. However, persistent rainfall in central areas continues to affect both progress and quality. This has fueled price volatility, with wheat prices initially spiking due to early supply tightness before softening as more crops entered the market. Experts caution that declining quality and regional supply gaps could deepen food security concerns and drive up prices for staple goods like bread and cereals, amplifying inflationary pressures and broader economic risks.

Ukraine

Ukraine Faces Lowest Wheat Harvest in a Decade Amid Weather and War Pressures

Ukraine’s wheat harvest in 2025 is projected to be the lowest in a decade due to severe spring frosts, hail, and ongoing war-related challenges. These issues have significantly reduced yields and damaged crop quality, particularly in southern regions. As of late Jul-25, only 7.1 mmt of wheat had been harvested from 2.18 million ha, reflecting a sharp lag compared to last year. These setbacks have pushed domestic wheat prices upward, with early Jul-25 levels rising from under USD 191.19/mt (UAH 8,000/mt) to USD 215.09/mt (UAH 9,000/mt), and bread prices increasing by 22% YoY. Although some experts remain cautiously optimistic, forecasting a 7% higher total grain harvest than in 2024, others warn of a possible 15-mmt drop in wheat export potential. Market pressures have also mounted due to falling export prices and shrinking margins for traders, with prices at Ukrainian ports becoming uncompetitive on free-on board (FOB) terms. Overall, the wheat market faces uncertainty, with rising domestic prices, declining export margins, and concerns over future food security and inflation.

2. Weekly Pricing

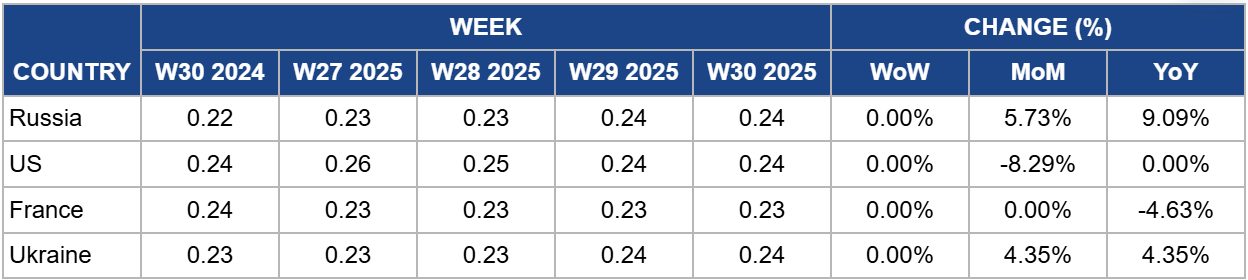

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W30 2024 to W30 2025)

Russia

In W30, Russia’s wheat prices remained stable week-on-week (WoW) at USD 0.24 per kilogram (kg) but rose by 4.35% month-on-month (MoM) and 9.09% YoY. During the first half of Jul-25, prices increased due to slow harvesting progress and lower yields, particularly in the southern regions. By July 4, only 2.5 million ha had been harvested, compared to 15.3 million ha during the same period last year, with average yields down to 3.2 mt/ha from 4.4 mt/ha. However, prices are expected to ease following this temporary rise as the new crop enters the market. By July 18, harvesting had gained momentum, with 23.9 mmt of wheat threshed, most of it from the South at 20.9 mmt, while operations gradually moved toward the central regions. Also, 6.9 million ha had been harvested compared to 9.8 million ha a year earlier, with the average yield improving to 3.5 mt/ha, narrowing the gap with last year’s 3.7 mt/ha.

United States

In W30, US wheat prices held steady WoW and YoY at USD 0.24/kg but were down 7.69% MoM. The weekly stability indicates that US wheat remains globally competitive, and potential reductions in Russian exports could create new demand opportunities for US suppliers. Protein spreads between HRS and HRW are expected to narrow as both wheat classes are showing adequate protein content. Meanwhile, Soft White (SW) prices remain steady, and Soft Red Winter (SRW) basis is largely unchanged.

On the trade front, net sales for the week ending July 17 totaled 712.18 thousand mt for delivery in the 2025/26 season. Combined outstanding sales and accumulated exports across all wheat classes have reached 8.9 mmt, 12% ahead of last year’s pace. The United States Department of Agriculture (USDA) projects total US wheat exports for 2025/26 at 23.1 mmt, with current commitments covering 39% of that target.

France

In W30, France's wheat prices held steady WoW and MoM at USD 0.23/kg, but remained 4.17% lower YoY, reflecting a stable yet subdued market environment. The French Ministry of Agriculture anticipates a strong rebound in soft wheat production in 2025, projecting output at 32.6 mmt, a 27% increase from 2024, when excessive rainfall severely affected yields. However, marketing this larger crop could be challenging. Demand from major export markets such as Algeria and China has declined, driven by diplomatic tensions and sufficient domestic supply, respectively. In addition, fierce price competition from Black Sea grain is expected to limit France’s export reach beyond the EU, with 2025/26 non-EU soft wheat exports forecasted at just 7.5 mmt. This could result in the highest end-of-season wheat stocks in 21 years. Although countries like Morocco, West Africa, Egypt, and Thailand absorbed much of France’s smaller 2024 crop, their demand may not be enough to offset the anticipated surplus, potentially putting downward pressure on export prices.

Ukraine

In W30, Ukraine’s wheat prices remained steady WoW at USD 0.24/kg but were down 4.35% both MoM and YoY, reflecting broader market softness despite short-term stability. However, underlying pressures persist. Delayed harvests and sales restrictions imposed by farmers in both Ukraine and Russia have fueled speculative price increases across the Black Sea region. Forecasts of additional rainfall in the coming week are further heightening concerns among traders, especially as Jul-25–Aug-25 shipping deadlines approach. Persistent rains in central and western Ukraine are slowing harvest progress and could raise the proportion of lower-quality feed wheat, likely widening the price gap between feed and milling wheat. At the same time, poor yields in southern Ukraine are tightening supply and driving up export prices, prompting increased buying activity at Black Sea ports.

3. Actionable Recommendations

Leverage High EU Yields for Strategic Market Repositioning

With EU wheat yields projected to exceed the five-year average, European producers should focus on optimizing storage capacity and targeting intra-EU and premium export markets to counter rising competition from Black Sea exporters. In particular, France and Germany can benefit from shifting more volumes toward higher-quality milling markets or into specialized wheat products to retain value. Additionally, regional coordination on export pricing and logistics can help avoid internal competition that could drive prices below production costs.

Diversify Canada’s Export Destinations and Strengthen Feed Integration

Faced with drought stress and trade uncertainty, Canada should prioritize diversifying its wheat export markets beyond traditional buyers to mitigate geopolitical and tariff risks. Capitalizing on strong durum wheat demand, Canada can also explore expanded trade agreements or private-sector deals in the Middle East and North Africa (MENA) and Southeast Asia. Simultaneously, policies encouraging the integration of lower-grade wheat into domestic livestock feed or biofuel markets can reduce surplus pressures, support prices, and improve value chain resilience.

Use Strategic Reserves to Stabilize Prices in India

India’s strong wheat reserves offer an opportunity to stabilize domestic prices through well-timed open market sales and buffer stock releases. The government should proactively monitor local supply-demand dynamics and deploy reserves to prevent market spikes, especially during lean months. Furthermore, maintaining import restrictions and safeguarding against cheap imports under new trade agreements will help protect farmer incomes and ensure self-sufficiency goals remain intact.

Capitalize on Indonesia’s Rising Wheat Demand with Long-Term Partnerships

To meet its commitment to double wheat imports from the US, Indonesia should invest in strengthening grain logistics, port infrastructure, and domestic milling capacity. In turn, the US can deepen ties through technical assistance, quality assurance programs, and tailored wheat varieties like HRW that match Indonesia’s end-use needs. Long-term contracts or futures-based agreements could also stabilize supply and prices for both parties amid global market competition.

Sources: Tridge, Agropolit, Economic times, Graintrade, Hellenic Shipping News, Oilworld, UkrAgroConsult