.jpg)

In W36 in the soybean landscape, some of the most relevant trends included:

- China continues to favor Brazilian soybeans, reinforcing Brazil's role as its preferred supplier. The significant 34% tariff on US soybeans effectively nullifies any price advantage, cementing China's reliance on South American imports for the near future.

- The global soybean market is facing increased scrutiny from both a trade and sustainability perspective. The ASA is formally accusing Brazil of using unfair subsidies, while major European retailers are pressuring Brazil to uphold the Amazon Soy Moratorium.

- Brazil is solidifying its market dominance with forecasts of a record harvest and continued strong exports, while the US market is weakening under harvest pressure and a lack of Chinese demand. This divergence caused US prices to fall 2.17% WoW while Brazilian prices remained stable.

- The US is attempting to mitigate its over-reliance on China by securing other key export destinations. The formal implementation of the US-Japan trade agreement is a positive step, but it is not yet sufficient to offset the significant market pressure from the ongoing Chinese trade dispute.

1. Weekly News

Global

Global Soybean Market Awaits Chinese Buying Decisions Amid US Harvest Uncertainty

The global soybean market is in a cautious phase as industry players await key United States (US) harvest data expected between September 15 to 20 and clarity on Chinese purchasing intentions for the new crop. While US crops are expected to yield well, initial stockpile projections are tight, making the upcoming harvest results a critical factor for price direction. The market is currently defined by China's absence from the US market since May-25, with South American suppliers, particularly Brazil and Argentina, fulfilling the majority of its recent demand. A potential resumption of US purchases faces significant economic hurdles. Although US soybeans are offered at a lower price point, approximately USD 420 per metric ton (mt) free on board (FOB) Gulf versus Brazil's USD 445/mt FOB for Nov-25 delivery, this advantage could be entirely nullified by steep retaliatory tariffs. China’s effective tariff on US soybeans is approximately 34% after including various taxes, creating a substantial barrier to trade. The industry anticipates China may resume some level of purchasing from the US in late Sep-25, but this high tariff cost casts considerable doubt on the potential volume, leaving the market uncertain whether significant demand will shift back to the US or remain focused on Brazil. Although a new trade agreement may lead to a resumption of some US purchases for the sake of supply diversification, the notion of the US regaining its former dominance is highly unlikely. The fundamental geopolitical and economic alignment ensures Brazil will remain the cornerstone of China's soybean import strategy for the foreseeable future.

Brazil

Safras & Mercado Raises Brazil's 2025/26 Soybean Production Forecast

Leading agribusiness consultancy Safras & Mercado has upwardly revised its forecast for Brazil's 2025/26 soybean harvest, signaling the potential for another record-breaking season. The new production estimate is pegged at 173.327 million metric tons (mmt), an increase from the firm's Jul-25 projection of 171.51 mmt. This updated figure represents a 2.3% increase over the 169.366 mmt produced in the 2024/25 cycle. The optimistic outlook is supported by an anticipated 2% expansion in the planted area, which is expected to reach 48.745 million hectares (ha), up from 47.78 million ha in the previous season. Furthermore, a modest improvement in productivity is also factored in, with the average yield projected to rise by 0.3% to 3,556 kilograms (kg) per ha. The primary driver for this positive revision is the favorable weather outlook associated with the expected return of the La Niña phenomenon, which typically brings beneficial rainfall to Brazil's key agricultural regions. This forecast reinforces Brazil's position as the dominant global supplier, with potential implications for global supply and pricing.

Brazil's Soybean Exports Surge on Strong Chinese Demand

Brazil's soybean export market is demonstrating remarkable strength, with Sep-25 shipments projected to reach 6.75 mmt, a substantial year-on-year (YoY) increase from 5.16 mmt in Sep-24. This robust performance is underpinned by a record-breaking harvest and sustained, strong demand from China. In Aug-25, China accounted for 84% of Brazil's soybean exports, significantly higher than the four-year average of 75%, a trend reinforced by ongoing Chinese trade tariffs on US soybeans. Despite a slight miss on August's export projections, the National Association of Cereal Exporters (ANEC) maintains its forecast for a record-setting year, anticipating total 2024/25 exports to reach 110 mmt, up from 97.3 mmt in 2023/24. With an additional 16 mmt expected to be shipped between October and December 2025, Brazil is solidifying its dominant position in the global soybean market.

European Retail Giants Rally to Defend Brazil's Amazon Soy Moratorium

Major European food retailers, including Tesco, Sainsbury's, Lidl, and Aldi, are exerting significant pressure on the world's largest grain traders to uphold Brazil's Amazon Soy Moratorium. In a formal letter, the retailers urged the CEOs of ADM, Bunge, Cargill, Louis Dreyfus Company, and China Oil and Foodstuffs Corporation (COFCO) to publicly reaffirm their commitment to the moratorium, a voluntary pact established in 2006 that bans the purchase of soybeans from Amazon land deforested after 2008. This initiative is credited with drastically reducing soy-driven deforestation in the region. The retailers' intervention comes at a critical time, following a decision by Brazil's antitrust authority, the Administrative Council for Economic Defense (CADE), to suspend the agreement in August after intense lobbying from Brazilian farm groups who claim it restricts competition. Although a temporary injunction has kept the moratorium in place, the market faces significant uncertainty. The European grocers have warned that if the agreement is dismantled, they will hold individual trading houses accountable to their own deforestation-free sourcing policies and that consumer pressure will intensify. This move underscores the growing importance of sustainability in the global soy supply chain and the pivotal role of market-driven initiatives in protecting vital ecosystems.

Brazil Gains Soybean Market Access to Togo, Expanding West African Footprint

Brazil has expanded its global soybean footprint by securing market access for soybean seeds in Togo, marking a strategic entry into the West African nation. The agreement, finalized by Brazil's Ministry of Agriculture and Livestock (MAPA), is part of a broader government initiative to diversify export destinations, representing the 13th new agricultural market opened in 2025. While Togo is a smaller player in the global soybean trade, importing 144,536 mt in 2023 and 89,193 mt in 2024, the development is strategically significant. It allows Brazil to compete in a market that has been traditionally dominated by regional suppliers such as Burkina Faso. This new access provides Brazilian exporters with an alternative outlet and establishes a commercial foothold in West Africa. The move contributes to Brazil's long-term goal of reducing reliance on a concentrated number of large buyers and fostering incremental growth in emerging markets around the world.

United States

US Soybean Producers Escalate Trade Dispute, Accusing Brazil of Unfair Trade Practices

Tensions between the world's leading soybean exporters have intensified as the American Soybean Association (ASA) formally petitions the US government to investigate Brazil for unfair trade practices. The ASA alleges that Brazil leverages a range of government subsidies—including preferential credit lines, public infrastructure investments, and regional tax incentives—to offer soybeans at unbeatable prices on the global market. US producers claim this strategy distorts competition and allows Brazil to capture market share at their expense, particularly in key destinations like China. In response to this pressure, the US Trade Representative (USTR) has initiated public consultations to examine Brazil's agricultural policies, with the ASA advocating for retaliatory tariffs. Brazil has countered these accusations, asserting that its support programs are fully compliant with World Trade Organization (WTO) rules and that its competitive edge is built on structural advantages in productivity and logistics, not illegal subsidies. The escalating dispute highlights the strategic importance of the soybean trade and could reshape global supply chains if the US proceeds with punitive measures against its South American rival.

US Soybean Farmers Welcome Implementation of US-Japan Trade Agreement

The US soybean industry has welcomed the formal implementation of the US–Japan Trade Agreement, which was enacted via a presidential Executive Order. The agreement includes provisions for Japan to make USD 8 billion in annual purchases of US goods, including food and agricultural products. This development is seen by industry stakeholders as a crucial step in formally securing a top-ten export market for American soybeans. Japan is already a vital trading partner, having imported USD 1.31 billion worth of US soy products in the 2023/24 marketing year, making it the sixth-largest market by volume. The ASA praised the timing of the agreement, noting that it provides valuable market certainty for farmers as the annual harvest commences. The ASA views the deal as a significant measure that strengthens market stability, prioritizes agricultural interests in trade negotiations, and helps maintain the global competitiveness of US soy producers.

China Trade Dispute Creates Anxiety for US Soybean Farmers as Harvest Commences

South Dakota soybean farmers are facing significant market uncertainty and financial pressure as they commence the 2025 harvest amidst the ongoing trade dispute with China. With China boycotting US soybeans in retaliation for tariffs, a crucial export channel has been severed. This has had a direct impact on profitability, with local prices already falling by USD 1.00 to USD 1.50 per bushel compared to the previous year. The absence of Chinese buyers, who typically purchase around 30% of the state's exported soybeans, is forcing producers to make difficult decisions. Many farmers are planning to store their newly harvested crop in the hope that a trade resolution will lead to a price recovery, raising concerns about potential storage capacity shortages. While industry leaders stress the urgent need for a trade deal, the situation has also intensified calls for long-term strategic adjustments. There is a growing consensus on the need to diversify export markets and develop new domestic demand streams, such as for sustainable aviation fuel, to reduce the industry's heavy reliance on a single major buyer.

2. Weekly Pricing

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W36 2024 to W36 2025)

Brazil

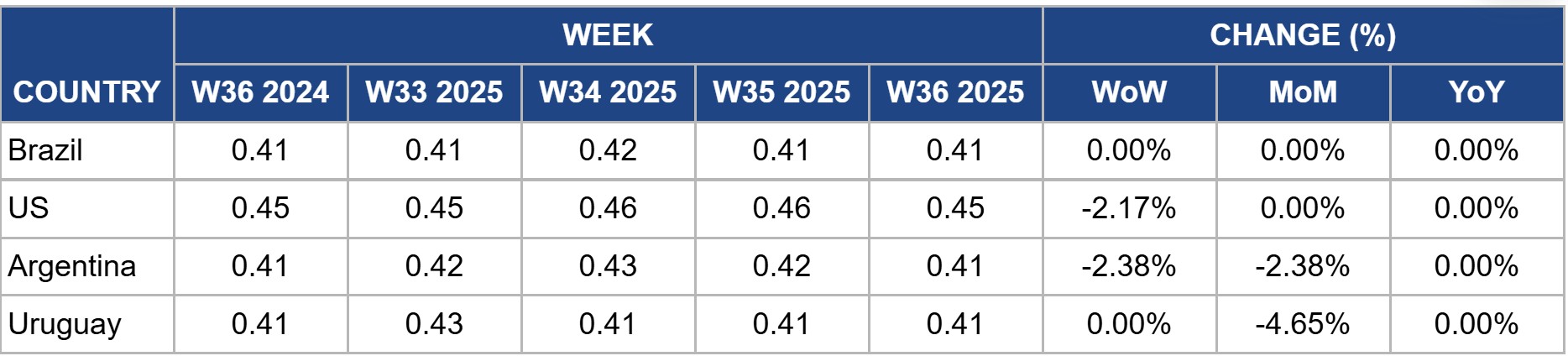

In Brazil, the price of soybeans was USD 0.41/kg in W36, showing no change week-on-week (WoW), month-on-month (MoM), or YoY. This price stability reflects a market carefully balancing exceptionally strong current demand against the prospect of a massive future supply. On one hand, robust export demand, particularly from China, is providing a solid price floor. Projections for a strong Sep-25 shipping pace, building on a record year for exports, are preventing prices from falling. On the other hand, a significant forecast upgrade for the upcoming 2025/26 harvest is capping any potential price increases. The consultancy Safras & Mercado raised its production estimate to a record 173.3 mmt based on a favorable La Niña weather outlook. Traders are weighing the immediate strong sales against this very large future crop, resulting in a market equilibrium for the time being.

United States

In the US, the price of soybeans was USD 0.45/kg in W36, down 2.17% WoW, but flat MoM and YoY. The WoW price decline reflects mounting pressure as the US harvest begins without any significant new crop export sales to the key Chinese market. Reports from states like South Dakota highlight growing farmer anxiety and the direct impact of China's boycott on local prices. While the formal implementation of the US–Japan trade deal provides some positive long-term news by securing a reliable market, it is not substantial enough to offset the immediate bearish sentiment. The MoM and YoY stability suggests that prices are finding some support at these lower levels, likely buoyed by strong domestic demand. However, the primary headwind remains the 34% Chinese tariff, which effectively negates the US price advantage over Brazil and will continue to limit price potential until a trade resolution is achieved.

Argentina

In Argentina, the price of soybeans was USD 0.41/kg in W36, down 2.38% WoW and MoM, but unchanged YoY. The price decline over the past month is primarily influenced by broader regional supply dynamics. The upward revision of Brazil's harvest forecast to a record high creates significant competitive pressure on Argentine exports, weighing on prices across South America. Furthermore, with the US harvest now commencing, the global market is anticipating an influx of new supply from the Northern Hemisphere, adding to the downward pressure on prices. The ongoing domestic issue of high export taxes, which makes soybeans less attractive for farmers compared to other crops, continues to disincentivize farmers from selling. This subdued market activity makes local prices more susceptible to negative external factors. The flat YoY price indicates that, despite current pressures, values remain within the same general range as the previous year.

Uruguay

In Uruguay, the price of soybeans was USD 0.41/kg in W36, stable WoW, but down 4.65% MoM and flat YoY. The WoW stability indicates that the market has maintained the equilibrium it found in the previous week. After earlier declines, which were largely attributed to localized factors such as the conclusion of major export programs for the season, prices have now leveled off. The market appears to be in a waiting period, balancing the lack of immediate, large-scale port demand with the broader price floor provided by the strong regional export environment led by neighboring Brazil. The notable MoM decline reflects the sharp price correction that occurred in previous weeks as logistical demand eased.

3. Actionable Recommendations

Navigate Chinese Absence by Focusing on Domestic and Alternative Export Markets

For US producers and exporters, the ongoing Chinese boycott and high tariffs create a significant headwind, as evidenced by the 2.17% WoW price drop. Producers should prioritize selling into the strong domestic market, where crush demand remains robust, to secure cash flow during the critical harvest period. Exporters must intensify efforts to leverage recent trade wins, such as the US-Japan agreement, by strengthening relationships and securing long-term contracts in these reliable markets. Furthermore, exploring and developing smaller, emerging markets, similar to Brazil's recent entry into Togo, can build a more resilient and diversified export portfolio for the future. This strategy of focusing on stable domestic and alternative international demand is critical to weathering the current geopolitical storm and reducing long-term dependence on the Chinese market.

Leverage Brazil's Favorable Supply Outlook for Forward Contracting

For global buyers and importers, Brazil's position as the dominant global supplier has been reinforced by an upgraded 2025/26 harvest forecast projecting a record 173.3 mmt. While current prices are stable due to strong immediate demand, this massive future supply suggests a bearish long-term outlook that could soften prices in the coming months. Importers, particularly those outside of China, should capitalize on this forecast by initiating negotiations for forward contracts for the new crop. Locking in supplies now could provide a hedge against potential logistical bottlenecks and secure favorable pricing before a potential surge in demand as the harvest approaches. Given China's strategic preference for Brazil, securing supply commitments early is a prudent risk management strategy to ensure consistent access to the world's largest soybean source.

Sources: Tridge, Safras & Mercado, Canal Rural, Datamar News, Reuters, Brazilian Ministry of Agriculture and Livestock, CPG, American Soybean Association, South Dekota, Searchlight